Abbott Laboratories Bull Put Spread

A bull put spread is a defined risk option strategy that profits if the stock closes above the short strike at expiry.

To execute a bull put spread an investor would sell an out-of-the-money put and then but a further out-of-the-money put.

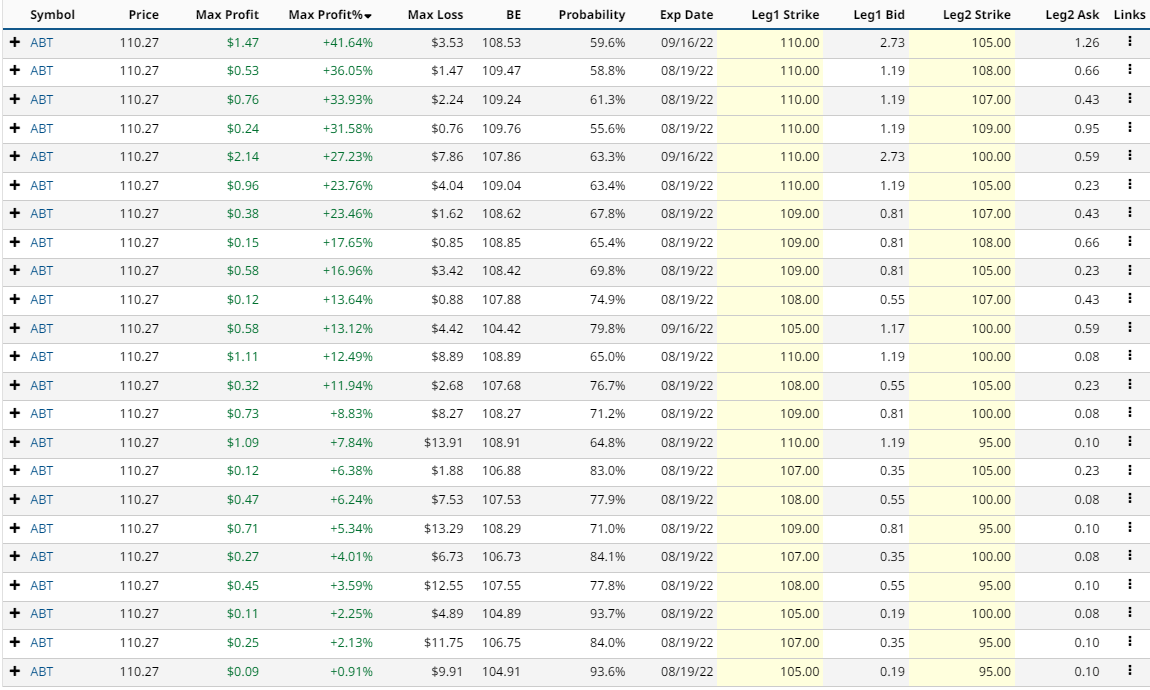

Running the Barchart Bull Put Spread Screener shows these results for ABT:

Let’s use the first line item as an example. This bull put spread trade involves selling the September expiry 110 strike put and buying the 105 strike put.

Selling this spread results in a credit of around $1.47 or $147 per contract. That is also the maximum possible gain on the trade. The maximum potential loss can be calculated by taking the spread width, less the premium received and multiplying by 100. That give us:

(5 – 1.47) x 100 = $353.

If we take the maximum gain divided by the maximum loss, we see the trade has a return potential of 41.64%.

The probability of the trade being successful is 59.6%, although this is just an estimate.

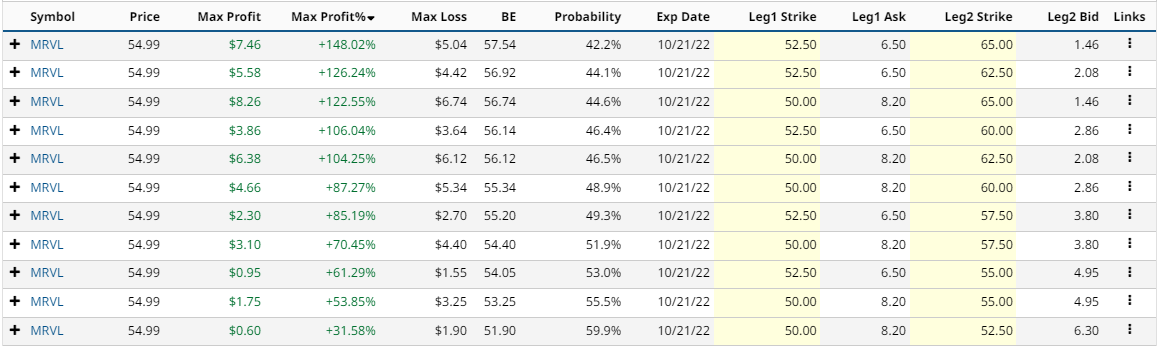

For MRVL, let’s look at the bull call spread screener.

Marvell Technology Bull Call Spread

Here are the results of the bull call spread screener:

A bull call spread is created through buying a call and then selling a further out-of-the-money call.

Selling the further out-of-the-money call reduces the cost of the trade but also limits the upside.

A bull call spread is a risk defined trade, so you always know the worst-case scenario. Bull call spreads are positive delta (bullish) and positive vega (benefit from a rise in implied volatility).

The first item on the screener involves buying the October expiration, 52.50-strike call and selling the 65 strike call.

The trade cost would be $504 (difference in the option prices multiplied by 100), and the maximum potential profit would be $746 (difference in strike prices, multiplied by 100 less the premium paid).

This trade has a max profit potential of 148.02% and a probability of 42.2%.

The final idea we will look at is a covered call trade.

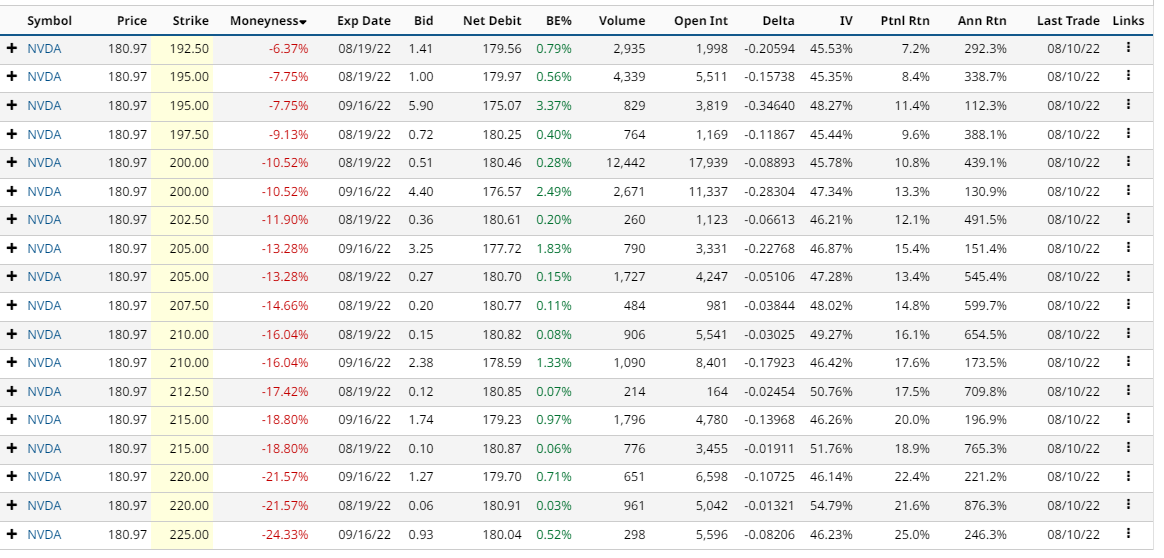

NVDA Covered Call

First, let’s run our covered call screener:

Let’s evaluate the first NVDA covered call example. Buying 100 shares of NVDA would cost around $18,097. The August 19, 192.50 strike call option was trading yesterday for around $1.41, generating $141 in premium per contract for covered call sellers.

Selling the call option generates an income of 0.79% in 9 days, equalling around 31.85% annualized. That assumes the stock stays exactly where it is. What if the stock rises above the strike price of 90?

If NVDA closes above 192.50 on the expiration date, the shares will be called away at 192.50, leaving the trader with a total profit of $1294 (gain on the shares plus the $141 option premium received). That equates to a 7.2% return, which is 292.3% on an annualized basis.

Conclusion

There you have three different bullish trade ideas on three different stocks. Remember to always manage risk and have stop losses in place.

Please remember that options are risky, and investors can lose 100% of their investment. This article is for education purposes only and not a trade recommendation. Remember to always do your own due diligence and consult your financial advisor before making any investment decisions.

Comments