There’s Nvidia —and then there’s everybody else. Once again, the chip maker has proven that it stands alone as the king of the artificial intelligence boom.

Let’s look at the numbers. Nvidia was the last member of the Magnificent Seven to report this earnings season. The disparity between its results and its rivals almost reads like a typo.

The other six technology giants posted revenue growth, averaging in the midteens versus the prior year, ranging from 2% for Apple on the low end to Meta Platforms at 25% at the high end. Meanwhile, Nvidia’s major chip rivals, Advanced Micro Devices and Intel, both grew revenue by 10%.

Nvidia’s fiscal fourth quarter, reported Wednesday, is simply in a different league from the rest. Revenue for its latest quarter, which ended in January, grew by 265% year-over-year to $22.1 billion. Its data-center business, primarily driven by AI chip demand, was even more impressive, up 409% from last year, to $18.4 billion.

The guidance was also strong. For the current quarter, Nvidia provided a revenue forecast range with $24 billion at the midpoint. That’s way above the Wall Street consensus of $22.2 billion, and suggests another 234% of revenue growth in the current quarter.

There’s no precedent for this kind of growth at a tech company as large as Nvidia. For bullish investors—and executives—it speaks to the power of AI. “Accelerated computing and generative AI have hit the tipping point,” Nvidia CEO Jensen Huang said during the company’s earnings release. “Demand is surging worldwide across companies, industries, and nations.”

Nvidia said the rise in its data-center results reflected growing shipments of its Hopper GPUs used for running large language AI models and generative AI applications. Large cloud-computing providers—like Amazon AWS, Microsoft Azure, and Google Cloud—accounted for more than half of the data-center revenue for the quarter.

Taking a step back, the company’s performance and strong outlook highlight Nvidia’s unassailable advantages: its prowess in managing its manufacturing supply chain and its ability to innovate quicker than its rivals.

Quintupling data-center revenue is an incredible feat given that Nvidia is selling physical hardware. Unlike software, which essentially scales at no cost, Nvidia is producing and shipping complex products—the company’s high-end AI systems consist of 35,000 parts.

In an interview after earnings, Nvidia Chief Financial Officer Colette Kress told me that the company’s growth was only possible thanks to the company’s three-decades-long relationships with key suppliers. “It’s a very complex process, and it takes both knowing your partners and understanding how they work,” the executive said, adding that Nvidia staff are on the phone with Taiwan Semiconductor Manufacturing, the company’s manufacturing partner, on a near-daily basis.

Beyond the supply chain, Nvidia has also started to release chips at a faster pace. In October, management updated its investor presentation, showing that the company has moved from a two-year product cycle to a one-year cadence for its AI data-center product portfolio.

I asked Kress about the new accelerated product launch cycle, and she confirmed that the one-year cadence remains the plan. “That’s the process we are on now,” she said. “We’ll talk quite a bit about that at GTC,” Nvidia’s developer conference that will be held in late March.

At some point the growth has to slow or end—at least that is Wall Street’s fear. But there’s growing confidence that the chip maker may see a new wave of growth next year too. The company doesn’t officially forecast beyond one quarter, but on Wednesday’s earnings call Huang suggested that he expects Nvidia will grow its revenue in 2025.

There are a couple of things Nvidia management mentioned that I believe can make that forecast a reality: demand for next-generation products and the growing market for large-language-model inference—the process of generating answers from those AI models.

On the earnings call, Kress said that while supply for current AI GPUs is improving, and demand is strong, Nvidia also expects “our next-generation products to be supply constrained as demand far exceeds supply.” Kress told me that “interest is high” from customers for those upcoming products. She didn’t give a specific timeline for their release.

Nvidia has suggested in investor presentations that its next-generation AI GPU, the B100, will be released in the coming quarters. Analysts expect Nvidia to increase the price of the B100 over the current H100 model. The “upcoming Blackwell architecture will drive another step up in performance, while ASPs [pricing] will increase as well,” Baird analyst Tristan Gerra wrote on Tuesday.

This past week’s earnings should put to rest one worry among Nvidia investors that the company’s current dominance in AI training won’t extend to the growing market around AI inference. But Nvidia revealed on Wednesday that inference already accounted for an estimated 40% of the company’s data-center revenue over the past year.

The number is “indicative of the strong competitive position the company maintains for LLM [large-language model] inference,” TD Cowen analyst Matthew Ramsay wrote on Wednesday. Inference “requires full-stack acceleration,” he added, noting Nvidia’s ability to incorporate chips, networking, and software to optimize customer performance.

Kress said that Nvidia’s products are compelling for customers because the company’s GPUs can be used for both training and inference, offering flexibility plus a higher level of performance and power efficiency that rivals can’t match.

With investor worries about a lull in growth and market-share losses now reduced, Nvidia shares hit a record highs on Thursday and Friday, surging 8.5% on the week to $788.

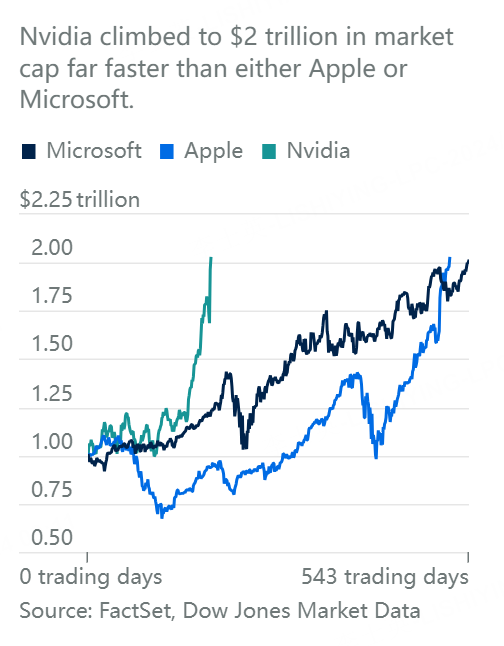

The advance gave the chip maker a $1.97 trillion market cap, pushing it past Amazon.com and Alphabet, to become the third most valuable U.S.-listed company. Just Apple and Microsoft are larger.

If Nvidia posts a few more record-breaking quarters, it won’t be long before it’s king of the entire stock market—not just AI.

Comments