Tesla reduced prices for inventory vehicles sold in the United States and Canada in the last quarter of 2023, likely to counteract the impact of high interest rates on consumer sentiment, indicating a potential further decline in gross profit margin in Q4.

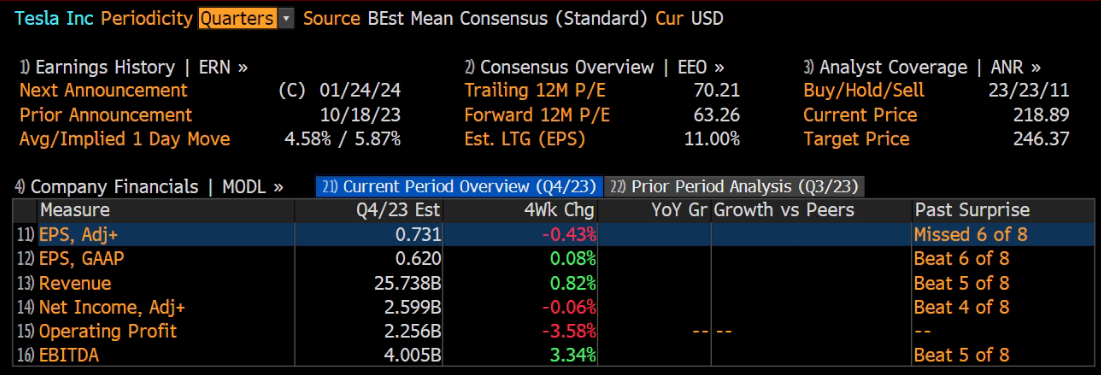

Tesla, Inc. is scheduled to release its fourth-quarter results after the market close on Jan. 24, and the company is widely expected to report lower revenue and earnings relative to the year-ago period. Adjusted earnings are likely to come in at about $0.731 per share and quarterly revenue will be $25.74 billion, according to Bloomberg's unanimous expectations.

Previous Quarter Review

Tesla saw a 102% increase in 2023, primarily due to a price reduction at the beginning of the year, leading to a significant surge in deliveries in the first two quarters, with 440,808 and 479,700 vehicles delivered, respectively.

However, in the third quarter, deliveries declined to 430,488 due to factory upgrades. Tesla's revenue for the last quarter was US$23.35 billion, showing a modest year-over-year growth of 8.8%. The adjusted EPS was $0.66, reflecting a 37% decrease compared to the previous year. The gross profit margin remained at 17.9%, staying below 20% for the third consecutive quarter.

Due to the underwhelming performance in Q3, Tesla's stock price briefly dropped below $200 in late October. However, driven by expectations of a Federal Reserve interest rate cut, the stock has been steadily rebounding since November, recovering all the losses incurred after the Q3 financial report.

Gross Profit Margin May Decline

In Q4, Tesla exceeded Wall Street expectations regarding deliveries, producing 494,989 vehicles and delivering 484,507. Notably, Model 3/Y contributed 461,538 units.

Despite achieving a record annual delivery of 1.81 million vehicles in 2023, surpassing the 1.8 million target, they fell short of Elon Musk's 2 million goal. As such, market response has been muted.

Tesla's stock experienced a 4.42% decline in the first week of January. Investors will likely closely watch the fourth-quarter gross profit margin performance, especially considering Tesla's four consecutive price hikes in November for vehicles sold in China. These were driven by profit concerns and increased competition from other electric vehicle manufacturers.

The price adjustments might be aimed at leveraging the "buy high, sell low" psychology of investors to stimulate sales. However, Tesla also reduced prices for inventory vehicles sold in the United States and Canada in the last quarter of 2023, likely to counteract the impact of high interest rates on consumer sentiment, indicating a potential further decline in gross profit margin in Q4.

Tesla's 4Q EPS is likely to be in line with consensus, and the company could project 2024 deliveries of 2.2 million vehicles (up 18% year over year), after a series of price cuts in 2023. Deliveries appear to have accelerated in 4Q vs. 3Q amid some pull-forward demand ahead of lower federal purchase-tax credits in 2024. The elevated volume likely offset year-end incentives, which dent profit margin. The electric-vehicle maker ramped up production to catch up on lost production in 3Q, when plants were shut down to upgrade vehicles.

Tesla's Performance in 2024

Looking ahead to 2024, the era of subsidies for new energy vehicles is ending. Germany's subsidy program for electric cars concluded on December 18, 2023, and France tightened subsidies, limiting them to a maximum of €7,000 for electric cars manufactured in Europe as of December 15 2023.

The subsidy policy decline in European and American countries and low demand caused by high-interest rates may compel Tesla to sustain its low-price strategy. Profit margins may be challenging to improve significantly, and economic downturn expectations might impact sales.

While Tesla may maintain its market share through a low-price strategy, Elon Musk acknowledged significant production challenges for the newly released Cybertruck.

The company's advanced neural network, with petabytes of training data, is likely to substitute its rule-based code in 2024. Yet, robotaxi service could significantly add to revenue in 2027 and not 2024.

In the Chinese market, several local manufacturers continued price reduction activities in 2024, indicating an ongoing price war. With new entrants like Xiaomi, competition is expected to intensify.

Tesla's main competitor, BYD, surpassed Tesla for the first time in Q4, becoming the global leader, selling 526 409 electric vehicles in the quarter and achieving total annual sales of 3.024 million electric vehicles.

Comments