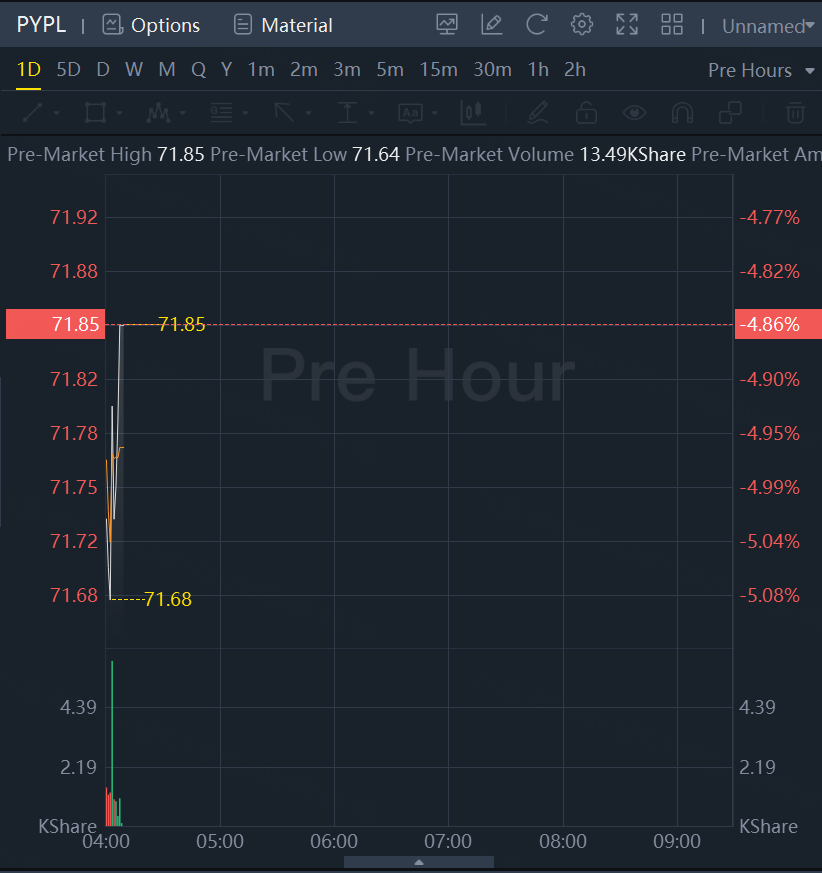

PayPal stock slumped 4.86% as margin talk underwhelms.

PayPal expects adjusted operating margin expansion of 100 basis points this year, compared with its earlier forecast of a 125-basis-point growth.

Investors are assuming that the company's branded checkout button, a high margin business, isn't doing as well as people thought it was and the fear is that they're losing market share to Apple, Dan Dolev, analyst at Mizuho told Reuters, explaining the drop in PayPal shares.

The high interest-rate environment has also begun to discourage expensive purchases as shoppers increasingly find themselves under heavy debt, particularly lower-income bracket customers, analysts have said.

PayPal payments volume on a forex-neutral basis came in at US$354.5 billion in the first-quarter ended Mar 31, compared with US$357.4 billion in the fourth-quarter ended Dec 31.

Executives at the payments firm had earlier cautioned that inflation was impacting discretionary consumer spending.

Still, the payments heavyweight raised its full-year adjusted profit forecast on the back of stronger-than-expected e-commerce trends and improved margins on cost cuts.

It now expects adjusted profit growth of about 20 per cent to US$4.95 per share, above analysts' average estimate of US$4.88 per share,

Adjusted operating margin in the first-quarter came in at 22.7 per cent compared with 20.7 per cent last year.

PayPal's revenue rose 10 per cent on a forex-neutral basis to US$7.04 billion in the first-quarter.

The payments firm posted a profit of US$1.17 per share on an adjusted basis for the quarter, compared with 88 cents last year.

PayPal growth slowed through the past year as countries around the world lifted restrictions and macroeconomic conditions deteriorated.

Comments