After months of prolonged slump and historic valuation compression in 2026, the U.S. cybersecurity and enterprise software sectors staged a strong rebound last week, riding the broader market’s recovery rally. The Dow Jones Industrial Average and the S&P 500 have fully recouped all losses stemming from the U.S.-Iran conflict. As the extreme bearish sentiment of “AI will disrupt everything” fades, Wall Street has reassessed the long-term impact of artificial intelligence on the industry, with many leading investors and analysts turning pessimism into optimism toward the software sector.

The Misalignment Between Sentiment Selloff and Fundamentals

The prolonged selloff was driven by deep market concerns that AI-native enterprises such as Anthropic and OpenAI would disrupt the traditional business models of software firms. Investors feared that AI would permanently erode enterprise software’s pricing power, revenue growth and profit margins, thereby wiping out the sector’s long-standing high valuation premium. However, such disruptive risks are largely reflected in market sentiment rather than corporate financials. Meanwhile, sharp valuation declines amid prior selloffs have created attractive entry opportunities for bargain-hunting investors.

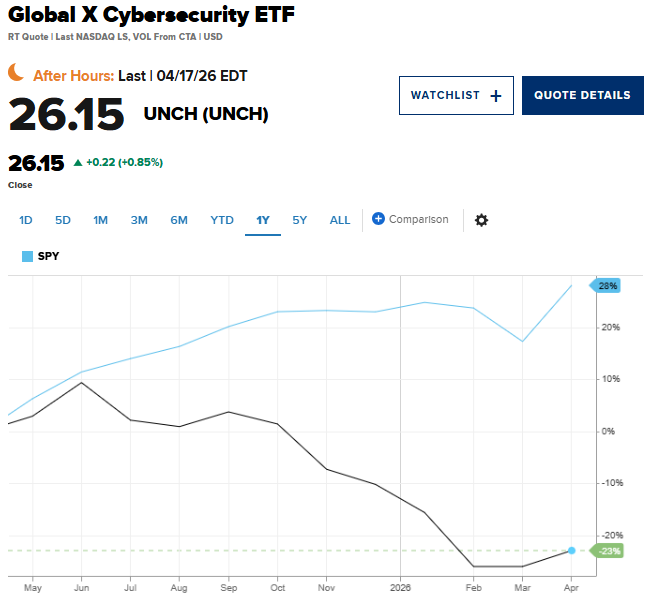

Data shows that the Global X Cybersecurity ETF (BUG.US) remains down roughly 12% year-to-date, yet it surged 12% last week; the First Trust Nasdaq Cybersecurity ETF (CIBR.US) also gained 9% over the week. This sharp reversal indicates the sector’s downturn stemmed not from earnings deterioration, but from extreme sentiment suppression.

Improved valuation appeal and marginal upgrades to earnings expectations have jointly fueled capital inflows. Industry research shows Wall Street analysts have quietly raised their outlooks for the software sector. Profit growth for software and services firms is projected to reach 16.5% in 2027, up from the 15.7% forecast in late February, with revenue expectations revised upward in tandem.

Christian Magoon, CEO of Amplify ETFs, described the sector as “a victim of AI-related headlines”. He noted that the core trigger for software stocks’ collapse was capital rotation toward AI infrastructure and semiconductors, while cybersecurity firms failed to benefit despite solid fundamental growth.

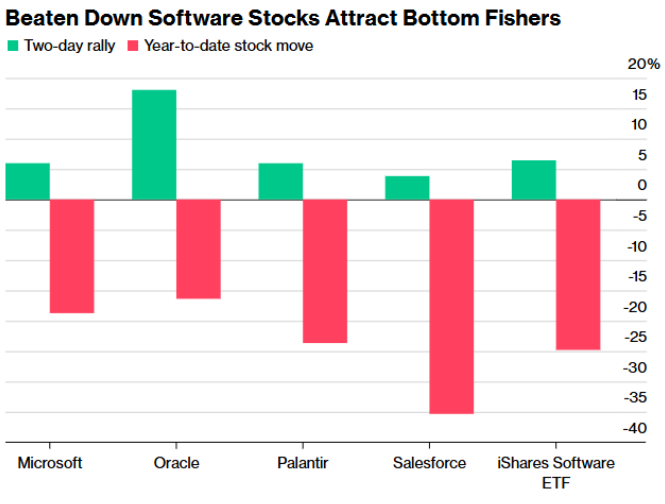

This divergence between valuation and fundamentals is prominent among leading tech names. Microsoft (MSFT.US) tumbled nearly 20% year-to-date before spiking 13% in a single week. Following Piper Sandler analyst Rob Owens’ reiterated “Overweight” rating on Palo Alto Networks (PANW.US), the stock jumped 7% in one day, though it still fell nearly 6% for the year. Peer players including CrowdStrike (CRWD.US) posted similar deep V-shaped rebounds.

Magoon added that AI brings both opportunities and uncertainties to the cybersecurity industry, driving higher demand while introducing new competitive threats.

Institutional & Legendary Investors Shift Stance: The Logic of Contrarian Capital

From Crowded Trades to Positive Feedback Loops

Market sentiment has seen a clear reversal as compressed valuations dismantle Wall Street’s bearish narratives. Brent Thill, tech analyst at Jefferies, stated that the worst period for the software sector is likely over, arguing that claims of a “dying software industry” and wholesale disruption by Anthropic and OpenAI are vastly overstated.

Marking a notable sentiment signal, legendary investor Michael Burry, the prototype of The Big Short, has revised his bearish views following the massive sector selloff. Burry commented last Wednesday that sharp declines in software stocks and the positive feedback loop between share price weakness and bank debt market dynamics have made software stocks worthy of close attention.

He explained that plummeting share prices have triggered a positive feedback loop in the credit market: collapsing equities may breach convertible bond covenants or trigger collateral shortfalls, forcing creditors into technical liquidation and exacerbating irrational downside pressure. Burry focuses on the fundamental bottom formed once deleveraging ends and weak hands finish selling.

Veteran strategist Ed Yardeni pointed out that U.S. tech stocks, after tumbling from record highs last year, have reached compelling valuation levels for long-term investors. Bill Baruch, head of Blue Line Capital, also argued that software stocks have been irrationally oversold. High-quality names including ServiceNow (NOW.US), Oracle (ORCL.US) and Microsoft present strong value, and the firm has allocated half of its cash reserves to increase positions in software stocks.

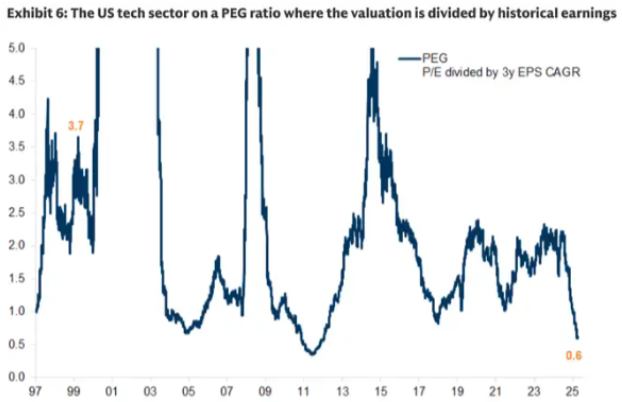

Major Wall Street banks have also issued bullish research notes. Peter Oppenheimer, strategist at Goldman Sachs, emphasized that the tech sector’s pullback represents a value opportunity. Global tech stocks’ forward PEG ratio has fallen below 1, hitting a multi-year low since 2005. Continuous upward revisions to 2026 and 2027 earnings forecasts and solid ROE levels further underpin current valuations.

Wells Fargo also acknowledged that IT sector valuations have turned highly attractive. The Wells Fargo Investment Institute upgraded the sector’s rating from Neutral to Favorable, citing its underperformance against the S&P 500 and robust long-term prospects supported by widespread AI adoption.

Market insights suggest steep valuation corrections have compressed the price-to-sales ratios of many SaaS enterprises to historic lows and may revitalize leveraged buyout activities in the private equity space. Meanwhile, rising AI-driven cyber threats are set to boost M&A activities among large tech firms in the cybersecurity sector, providing solid bottom support for stock prices.

Magoon added that contrarian investors typically step in once sector sub-sectors correct by more than 10%. Growing cyber risks in an AI-powered era will further accelerate cybersecurity M&A, offering sustained upside catalysts.

Lingering Risks: Long-Term Allocation Amid the Midterm Election Overhang

Despite the powerful short-term rebound, Wall Street remains cautious over blind chasing. Thill indicated that institutional investors still maintain an underweight stance on software stocks, while Magoon issued clear macro warnings.

Historical data cited by Magoon reveals that 2026, as a U.S. midterm election year, is historically characterized by sharp market pullbacks and elevated volatility. He warned that current market pressures may worsen in the short term.

Nevertheless, periodic downturns create long-term opportunities for patient investors. Historically, markets have delivered strong 12-month returns after midterm election-driven corrections. Citing Bank of America data, Magoon noted that the best-performing contrarian assets are often those with the lowest institutional positioning at the early stage of a downturn, citing energy stocks’ explosive rebound after multi-year low institutional holdings. Such contrarian logic requires a longer time horizon for application in the software sector.

Although some analysts such as Thill still recommend underweighting beaten-down software stocks and seeking marginal opportunities, Magoon advised long-term investors with no urgent liquidity needs to focus on high-quality sub-sectors and maintain holdings during market downturns, to capture full recovery dividends in the next cycle.

Comments