Warren Buffett released his annual letter to Berkshire Hathaway shareholders on Saturday. The 91-year-old investing legend has been publishing the letter for over six decades and it has become required reading for investors around the world.

Warren Buffett said he now considers tech giant Apple as one of the four pillars driving Berkshire Hathaway, the conglomerate of mostly old-economy businesses he’s assembled over the last five decades.

In his annual letter to shareholders released on Saturday, the 91-year-old investing legend listed Apple under the heading “Our Four Giants” and even called the company the second-most important after Berkshire’s cluster of insurers, thanks to its chief executive.

“Tim Cook, Apple’s brilliant CEO, quite properly regards users of Apple products as his first love, but all of his other constituencies benefit from Tim’s managerial touch as well,” the letter stated.

Buffett made clear he is a fan of Cook’s stock repurchase strategy, and how it gives the conglomerate increased ownership of each dollar of the iPhone maker’s earnings without the investor having to lift a finger.

“Apple – our runner-up Giant as measured by its yearend market value – is a different sort of holding. Here, our ownership is a mere 5.55%, up from 5.39% a year earlier,” Buffett said in the letter. “That increase sounds like small potatoes. But consider that each 0.1% of Apple’s 2021 earnings amounted to $100 million. We spent no Berkshire funds to gain our accretion. Apple’s repurchases did the job.”

Berkshire began buying Apple stock in 2016 under the influence of Buffett’s investing deputies Todd Combs and Ted Weschler. By mid-2018, the conglomerate accumulated 5% ownership of the iPhone maker, a stake that cost $36 billion. Today, the Apple investment is now worth more than $160 billion, taking up 40% of Berkshire’s equity portfolio.

“It’s important to understand that only dividends from Apple are counted in the GAAP earnings Berkshire reports – and last year, Apple paid us $785 million of those. Yet our ‘share’ of Apple’s earnings amounted to a staggering $5.6 billion. Much of what the company retained was used to repurchase Apple shares, an act we applaud,” Buffett said.

Berkshire is Apple’s largest shareholder, outside of index and exchange-traded fund providers.

Buffett also credited his railroad business BNSF and energy segment BHE as two other giants of the conglomerate, which both registered record earnings in 2021.

“BNSF, our third Giant, continues to be the number one artery of American commerce, which makes it an indispensable asset for America as well as for Berkshire,” Buffett said. “BHE has become a utility powerhouse and a leading force in wind, solar and transmission throughout much of the United States.”

Read the full letter here:

To the Shareholders of Berkshire Hathaway Inc.:

Charlie Munger, my long-time partner, and I have the job of managing a portion of your savings. We are honored by your trust.

Our position carries with it the responsibility to report to you what we would like to know if we were the absentee owner and you were the manager. We enjoy communicating directly with you through this annual letter, and through the annual meeting as well.

Our policy is to treat all shareholders equally. Therefore, we do not hold discussions with analysts nor large institutions. Whenever possible, also, we release important communications on Saturday mornings in order to maximize the time for shareholders and the media to absorb the news before markets open on Monday.

A wealth of Berkshire facts and figures are set forth in the annual 10-K that the company regularly files with the S.E.C. and that we reproduce on pages K-1 – K-119. Some shareholders will find this detail engrossing; others will simply prefer to learn what Charlie and I believe is new or interesting at Berkshire.

Alas, there was little action of that sort in 2021. We did, though, make reasonable progress in increasing the intrinsic value of your shares. That task has been my primary duty for 57 years. And it will continue to be.

What You Own

Berkshire owns a wide variety of businesses, some in their entirety, some only in part. The second group largely consists of marketable common stocks of major American companies. Additionally, we own a few non-U.S. equities and participate in several joint ventures or other collaborative activities.

Whatever our form of ownership, our goal is to have meaningful investments in businesses with both durable economic advantages and a first-class CEO. Please note particularly that we own stocks based upon our expectations about their long-term business performance and not because we view them as vehicles for timely market moves. That point is crucial: Charlie and I are not stock-pickers; we are business-pickers.

I make many mistakes. Consequently, our extensive collection of businesses includes some enterprises that have truly extraordinary economics, many others that enjoy good economic characteristics, and a few that are marginal. One advantage of our common-stock segment is that – on occasion – it becomes easy to buy pieces of wonderful businesses at wonderful prices. That shooting-fish-in-a-barrel experience is very rare in negotiated transactions and never occurs en masse. It is also far easier to exit from a mistake when it has been made in the marketable arena.

Surprise, Surprise

Here are a few items about your company that often surprise even seasoned investors:

• Many people perceive Berkshire as a large and somewhat strange collection of financial assets. In truth, Berkshire owns and operates more U.S.-based “infrastructure” assets – classified on our balance sheet as property, plant and equipment – than are owned and operated by any other American corporation. That supremacy has never been our goal. It has, however, become a fact.

At yearend, those domestic infrastructure assets were carried on Berkshire’s balance sheet at $158 billion. That number increased last year and will continue to increase. Berkshire always will be building.

• Every year, your company makes substantial federal income tax payments. In 2021, for example, we paid

$3.3 billion while the U.S. Treasury reported total corporate income-tax receipts of $402 billion. Additionally, Berkshire pays substantial state and foreign taxes. “I gave at the office” is an unassailable assertion when made by Berkshire shareholders.

Berkshire’s history vividly illustrates the invisible and often unrecognized financial partnership between government and American businesses. Our tale begins early in 1955, when Berkshire Fine Spinning and Hathaway Manufacturing agreed to merge their businesses. In their requests for shareholder approval, these venerable New England textile companies expressed high hopes for the combination.

The Hathaway solicitation, for example, assured its shareholders that “The combination of the resources and managements will result in one of the strongest and most efficient organizations in the textile industry.” That upbeat view was endorsed by the company’s advisor, Lehman Brothers (yes, that Lehman Brothers).

I’m sure it was a joyous day in both Fall River (Berkshire) and New Bedford (Hathaway) when the union was consummated. After the bands stopped playing and the bankers went home, however, the shareholders reaped a disaster.

In the nine years following the merger, Berkshire’s owners watched the company’s net worth crater from

$51.4 million to $22.1 million. In part, this decline was caused by stock repurchases, ill-advised dividends and plant shutdowns. But nine years of effort by many thousands of employees delivered an operating loss as well. Berkshire’s struggles were not unusual: The New England textile industry had silently entered an extended and non-reversible death march.

During the nine post-merger years, the U.S. Treasury suffered as well from Berkshire’s troubles. All told, the company paid the government only $337,359 in income tax during that period – a pathetic $100 per day.

Early in 1965, things changed. Berkshire installed new management that redeployed available cash and steered essentially all earnings into a variety of good businesses, most of which remained good through the years. Coupling reinvestment of earnings with the power of compounding worked its magic, and shareholders prospered.

Berkshire’s owners, it should be noted, were not the only beneficiary of that course correction. Their “silent partner,” the U.S. Treasury, proceeded to collect many tens of billions of dollars from the company in income tax payments. Remember the $100 daily? Now, Berkshire pays roughly $9 million daily to the Treasury.

In fairness to our governmental partner, our shareholders should acknowledge – indeed trumpet – the fact that Berkshire’s prosperity has been fostered mightily because the company has operated in America. Our country would have done splendidly in the years since 1965 without Berkshire. Absent our American home, however, Berkshire would never have come close to becoming what it is today. When you see the flag, say thanks.

• From an $8.6 million purchase of National Indemnity in 1967, Berkshire has become the world leader in insurance “float” – money we hold and can invest but that does not belong to us. Including a relatively small sum derived from life insurance, Berkshire’s total float has grown from $19 million when we entered the insurance business to $147 billion.

So far, this float has cost us less than nothing. Though we have experienced a number of years when insurance losses combined with operating expenses exceeded premiums, overall we have earned a modest 55-year profit from the underwriting activities that generated our float.

Of equal importance, float is very sticky. Funds attributable to our insurance operations come and go daily, but their aggregate total is immune from precipitous decline. When it comes to investing float, we can therefore think long-term.

If you are not already familiar with the concept of float, I refer you to a long explanation on page A-5. To my surprise, our float increased $9 billion last year, a buildup of value that is important to Berkshire owners though is not reflected in our GAAP (“generally-accepted accounting principles”) presentation of earnings and net worth.

Much of our huge value creation in insurance is attributable to Berkshire’s good luck in my 1986 hiring of Ajit Jain. We first met on a Saturday morning, and I quickly asked Ajit what his insurance experience had been. He replied, “None.”

I said, “Nobody’s perfect,” and hired him. That was my lucky day: Ajit actually was as perfect a choice as could have been made. Better yet, he continues to be – 35 years later.

One final thought about insurance: I believe that it is likely – but far from assured – that Berkshire’s float can be maintained without our incurring a long-term underwriting loss. I am certain, however, that there will be some years when we experience such losses, perhaps involving very large sums.

Berkshire is constructed to handle catastrophic events as no other insurer – and that priority will remain long after Charlie and I are gone.

Our Four Giants

Through Berkshire, our shareholders own many dozens of businesses. Some of these, in turn, have a collection of subsidiaries of their own. For example, Marmon has more than 100 individual business operations, ranging from the leasing of railroad cars to the manufacture of medical devices.

• Nevertheless, operations of our “Big Four” companies account for a very large chunk of Berkshire’s value. Leading this list is our cluster of insurers. Berkshire effectively owns 100% of this group, whose massive float value we earlier described. The invested assets of these insurers are further enlarged by the extraordinary amount of capital we invest to back up their promises.

The insurance business is made to order for Berkshire. The product will never be obsolete, and sales volume will generally increase along with both economic growth and inflation. Also, integrity and capital will forever be important. Our company can and will behave well.

There are, of course, other insurers with excellent business models and prospects. Replication of Berkshire’s operation, however, would be almost impossible.

• Apple – our runner-up Giant as measured by its yearend market value – is a different sort of holding. Here, our ownership is a mere 5.55%, up from 5.39% a year earlier. That increase sounds like small potatoes. But consider that each 0.1% of Apple’s 2021 earnings amounted to $100 million. We spent no Berkshire funds to gain our accretion. Apple’s repurchases did the job.

It’s important to understand that only dividends from Apple are counted in the GAAP earnings Berkshire reports – and last year, Apple paid us $785 million of those. Yet our “share” of Apple’s earnings amounted to a staggering $5.6 billion. Much of what the company retained was used to repurchase Apple shares, an act we applaud. Tim Cook, Apple’s brilliant CEO, quite properly regards users of Apple products as his first love, but all of his other constituencies benefit from Tim’s managerial touch as well.

• BNSF, our third Giant, continues to be the number one artery of American commerce, which makes it an indispensable asset for America as well as for Berkshire. If the many essential products BNSF carries were instead hauled by truck, America’s carbon emissions would soar.

Your railroad had record earnings of $6 billion in 2021. Here, it should be noted, we are talking about the old-fashioned sort of earnings that we favor: a figure calculated after interest, taxes, depreciation, amortization and all forms of compensation. (Our definition suggests a warning: Deceptive “adjustments” to earnings – to use a polite description – have become both more frequent and more fanciful as stocks have risen. Speaking less politely, I would say that bull markets breed bloviated bull )

BNSF trains traveled 143 million miles last year and carried 535 million tons of cargo. Both accomplishments far exceed those of any other American carrier. You can be proud of your railroad.

• BHE, our final Giant, earned a record $4 billion in 2021. That’s up more than 30-fold from the $122 million earned in 2000, the year that Berkshire first purchased a BHE stake. Now, Berkshire owns 91.1% of the company.

BHE’s record of societal accomplishment is as remarkable as its financial performance. The company had no wind or solar generation in 2000. It was then regarded simply as a relatively new and minor participant in the huge electric utility industry. Subsequently, under David Sokol’s and Greg Abel’s leadership, BHE has become a utility powerhouse (no groaning, please) and a leading force in wind, solar and transmission throughout much of the United States.

Greg’s report on these accomplishments appears on pages A-3 and A-4. The profile you will find there is not in any way one of those currently-fashionable “green-washing” stories. BHE has been faithfully detailing its plans and performance in renewables and transmissions every year since 2007.

To further review this information, visit BHE’s website at brkenergy.com. There, you will see that the company has long been making climate-conscious moves that soak up all of its earnings. More opportunities lie ahead. BHE has the management, the experience, the capital and the appetite for the huge power projects that our country needs.

Investments

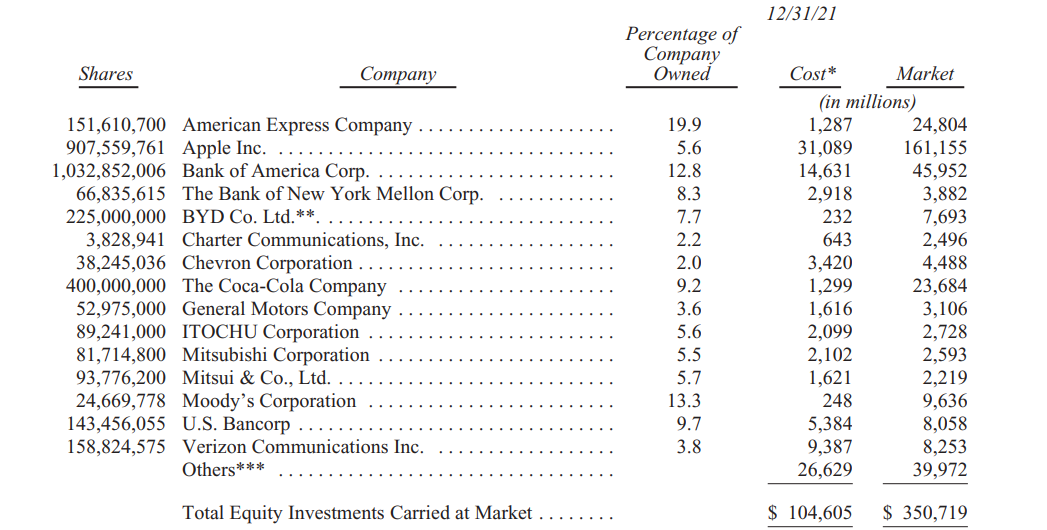

Now let’s talk about companies we don’t control, a list that again references Apple. Below we list our fifteen largest equity holdings, several of which are selections of Berkshire’s two long-time investment managers, Todd Combs and Ted Weschler. At yearend, this valued pair had total authority in respect to $34 billion of investments, many of which do not meet the threshold value we use in the table. Also, a significant portion of the dollars that Todd and Ted manage are lodged in various pension plans of Berkshire-owned businesses, with the assets of these plans not included in this table.

** Held by BHE; consequently, Berkshire shareholders have only a 91.1% interest in this position.

*** Includes a $10 billion investment in Occidental Petroleum, consisting of preferred stock and warrants to buy common stock, a combination now being valued at $10.7 billion.

In addition to the footnoted Occidental holding and our various common-stock positions, Berkshire also owns a 26.6% interest in Kraft Heinz (accounted for on the “equity” method, not market value, and carried at $13.1 billion) and 38.6% of Pilot Corp., a leader in travel centers that had revenues last year of $45 billion.

Since we purchased our Pilot stake in 2017, this holding has warranted “equity” accounting treatment. Early in 2023, Berkshire will purchase an additional interest in Pilot that will raise our ownership to 80% and lead to our fully consolidating Pilot’s earnings, assets and liabilities in our financial statements.

U.S. Treasury Bills

Berkshire’s balance sheet includes $144 billion of cash and cash equivalents (excluding the holdings of BNSF and BHE). Of this sum, $120 billion is held in U.S. Treasury bills, all maturing in less than a year. That stake leaves Berkshire financing about 12 of 1% of the publicly-held national debt.

Charlie and I have pledged that Berkshire (along with our subsidiaries other than BNSF and BHE) will always hold more than $30 billion of cash and equivalents. We want your company to be financially impregnable and never dependent on the kindness of strangers (or even that of friends). Both of us like to sleep soundly, and we want our creditors, insurance claimants and you to do so as well.

But $144 billion?

That imposing sum, I assure you, is not some deranged expression of patriotism. Nor have Charlie and I lost our overwhelming preference for business ownership. Indeed, I first manifested my enthusiasm for that 80 years ago, on March 11, 1942, when I purchased three shares of Cities Services preferred stock. Their cost was $114.75 and required all of my savings. (The Dow Jones Industrial Average that day closed at 99, a fact that should scream to you: Never bet against America.)

After my initial plunge, I always kept at least 80% of my net worth in equities. My favored status throughout that period was 100% – and still is. Berkshire’s current 80%-or-so position in businesses is a consequence of my failure to find entire companies or small portions thereof (that is, marketable stocks) which meet our criteria for long- term holding.

Charlie and I have endured similar cash-heavy positions from time to time in the past. These periods are never pleasant; they are also never permanent. And, fortunately, we have had a mildly attractive alternative during 2020 and 2021 for deploying capital. Read on.

Share Repurchases

There are three ways that we can increase the value of your investment. The first is always front and center in our minds: Increase the long-term earning power of Berkshire’s controlled businesses through internal growth or by making acquisitions. Today, internal opportunities deliver far better returns than acquisitions. The size of those opportunities, however, is small compared to Berkshire’s resources.

Our second choice is to buy non-controlling part-interests in the many good or great businesses that are publicly traded. From time to time, such possibilities are both numerous and blatantly attractive. Today, though, we find little that excites us.

That’s largely because of a truism: Long-term interest rates that are low push the prices of all productive investments upward, whether these are stocks, apartments, farms, oil wells, whatever. Other factors influence valuations as well, but interest rates will always be important.

Our final path to value creation is to repurchase Berkshire shares. Through that simple act, we increase your share of the many controlled and non-controlled businesses Berkshire owns. When the price/value equation is right, this path is the easiest and most certain way for us to increase your wealth. (Alongside the accretion of value to continuing shareholders, a couple of other parties gain: Repurchases are modestly beneficial to the seller of the repurchased shares and to society as well.)

Periodically, as alternative paths become unattractive, repurchases make good sense for Berkshire’s owners. During the past two years, we therefore repurchased 9% of the shares that were outstanding at yearend 2019 for a total cost of $51.7 billion. That expenditure left our continuing shareholders owning about 10% more of all Berkshire businesses, whether these are wholly-owned (such as BNSF and GEICO) or partly-owned (such as Coca-Cola and Moody’s).

I want to underscore that for Berkshire repurchases to make sense, our shares must offer appropriate value. We don’t want to overpay for the shares of other companies, and it would be value-destroying if we were to overpay when we are buying Berkshire. As of February 23, 2022, since yearend we repurchased additional shares at a cost of $1.2 billion. Our appetite remains large but will always remain price-dependent.

It should be noted that Berkshire’s buyback opportunities are limited because of its high-class investor base. If our shares were heavily held by short-term speculators, both price volatility and transaction volumes would materially increase. That kind of reshaping would offer us far greater opportunities for creating value by making repurchases. Nevertheless, Charlie and I far prefer the owners we have, even though their admirable buy-and-keep attitudes limit the extent to which long-term shareholders can profit from opportunistic repurchases.

Finally, one easily-overlooked value calculation specific to Berkshire: As we’ve discussed, insurance “float” of the right sort is of great value to us. As it happens, repurchases automatically increase the amount of “float” per share. That figure has increased during the past two years by 25% – going from $79,387 per “A” share to $99,497, a meaningful gain that, as noted, owes some thanks to repurchases.

A Wonderful Man and a Wonderful Business

Last year, Paul Andrews died. Paul was the founder and CEO of TTI, a Fort Worth-based subsidiary of Berkshire. Throughout his life – in both his business and his personal pursuits – Paul quietly displayed all the qualities that Charlie and I admire. His story should be told.

In 1971, Paul was working as a purchasing agent for General Dynamics when the roof fell in. After losing a huge defense contract, the company fired thousands of employees, including Paul.

With his first child due soon, Paul decided to bet on himself, using $500 of his savings to found Tex-Tronics (later renamed TTI). The company set itself up to distribute small electronic components, and first-year sales totaled $112,000. Today, TTI markets more than one million different items with annual volume of $7.7 billion.

But back to 2006: Paul, at 63, then found himself happy with his family, his job, and his associates. But he had one nagging worry, heightened because he had recently witnessed a friend’s early death and the disastrous results that followed for that man’s family and business. What, Paul asked himself in 2006, would happen to the many people depending on him if he should unexpectedly die?

For a year, Paul wrestled with his options. Sell to a competitor? From a strictly economic viewpoint, that course made the most sense. After all, competitors could envision lucrative “synergies” – savings that would be achieved as the acquiror slashed duplicated functions at TTI.

But . . . Such a purchaser would most certainly also retain its CFO, its legal counsel, its HR unit. Their TTI counterparts would therefore be sent packing. And ugh! If a new distribution center were to be needed, the acquirer’s home city would certainly be favored over Fort Worth.

Whatever the financial benefits, Paul quickly concluded that selling to a competitor was not for him. He next considered seeking a financial buyer, a species once labeled – aptly so – a leveraged buyout firm. Paul knew, however, that such a purchaser would be focused on an “exit strategy.” And who could know what that would be? Brooding over it all, Paul found himself having no interest in handing his 35-year-old creation over to a reseller.

When Paul met me, he explained why he had eliminated these two alternatives as buyers. He then summed up his dilemma by saying – in far more tactful phrasing than this – “After a year of pondering the alternatives, I want to sell to Berkshire because you are the only guy left.” So, I made an offer and Paul said “Yes.” One meeting; one lunch; one deal.

To say we both lived happily ever after is an understatement. When Berkshire purchased TTI, the company employed 2,387. Now the number is 8,043. A large percentage of that growth took place in Fort Worth and environs. Earnings have increased 673%.

Annually, I would call Paul and tell him his salary should be substantially increased. Annually, he would tell me, “We can talk about that next year, Warren; I’m too busy now.”

When Greg Abel and I attended Paul’s memorial service, we met children, grandchildren, long-time associates (including TTI’s first employee) and John Roach, the former CEO of a Fort Worth company Berkshire had purchased in 2000. John had steered his friend Paul to Omaha, instinctively knowing we would be a match.

At the service, Greg and I heard about the multitudes of people and organizations that Paul had silently supported. The breadth of his generosity was extraordinary – geared always to improving the lives of others, particularly those in Fort Worth.

In all ways, Paul was a class act.

* * * * * * * * * * * *

Good luck – occasionally extraordinary luck – has played its part at Berkshire. If Paul and I had not enjoyed a mutual friend – John Roach – TTI would not have found its home with us. But that ample serving of luck was only the beginning. TTI was soon to lead Berkshire to its most important acquisition.

Every fall, Berkshire directors gather for a presentation by a few of our executives. We sometimes choose the site based upon the location of a recent acquisition, by that means allowing directors to meet the new subsidiary’s CEO and learn more about the acquiree’s activities.

In the fall of 2009, we consequently selected Fort Worth so that we could visit TTI. At that time, BNSF, which also had Fort Worth as its hometown, was the third-largest holding among our marketable equities. Despite that large stake, I had never visited the railroad’s headquarters.

Deb Bosanek, my assistant, scheduled our board’s opening dinner for October 22. Meanwhile, I arranged to arrive earlier that day to meet with Matt Rose, CEO of BNSF, whose accomplishments I had long admired. When I made the date, I had no idea that our get-together would coincide with BNSF’s third-quarter earnings report, which was released late on the 22nd.

The market reacted badly to the railroad’s results. The Great Recession was in full force in the third quarter, and BNSF’s earnings reflected that slump. The economic outlook was also bleak, and Wall Street wasn’t feeling friendly to railroads – or much else.

On the following day, I again got together with Matt and suggested that Berkshire would offer the railroad a better long-term home than it could expect as a public company. I also told him the maximum price that Berkshire would pay.

Matt relayed the offer to his directors and advisors. Eleven busy days later, Berkshire and BNSF announced a firm deal. And here I’ll venture a rare prediction: BNSF will be a key asset for Berkshire and our country a century from now.

The BNSF acquisition would never have happened if Paul Andrews hadn’t sized up Berkshire as the right home for TTI.

Thanks

I taught my first investing class 70 years ago. Since then, I have enjoyed working almost every year with students of all ages, finally “retiring” from that pursuit in 2018.

Along the way, my toughest audience was my grandson’s fifth-grade class. The 11-year-olds were squirming in their seats and giving me blank stares until I mentioned Coca-Cola and its famous secret formula. Instantly, every hand went up, and I learned that “secrets” are catnip to kids.

Teaching, like writing, has helped me develop and clarify my own thoughts. Charlie calls this phenomenon the orangutan effect: If you sit down with an orangutan and carefully explain to it one of your cherished ideas, you may leave behind a puzzled primate, but will yourself exit thinking more clearly.

Talking to university students is far superior. I have urged that they seek employment in (1) the field and (2) with the kind of people they would select, if they had no need for money. Economic realities, I acknowledge, may interfere with that kind of search. Even so, I urge the students never to give up the quest, for when they find that sort of job, they will no longer be “working.”

Charlie and I, ourselves, followed that liberating course after a few early stumbles. We both started as part- timers at my grandfather’s grocery store, Charlie in 1940 and I in 1942. We were each assigned boring tasks and paid little, definitely not what we had in mind. Charlie later took up law, and I tried selling securities. Job satisfaction continued to elude us.

Finally, at Berkshire, we found what we love to do. With very few exceptions, we have now “worked” for many decades with people whom we like and trust. It’s a joy in life to join with managers such as Paul Andrews or the Berkshire families I told you about last year. In our home office, we employ decent and talented people – no jerks. Turnover averages, perhaps, one person per year.

I would like, however, to emphasize a further item that turns our jobs into fun and satisfaction working

for you. There is nothing more rewarding to Charlie and me than enjoying the trust of individual long-term shareholders who, for many decades, have joined us with the expectation that we would be a reliable custodian of their funds.

Obviously, we can’t select our owners, as we could do if our form of operation were a partnership. Anyone can buy shares of Berkshire today with the intention of soon reselling them. For sure, we get a few of that type of shareholder, just as we get index funds that own huge amounts of Berkshire simply because they are required to do so.

To a truly unusual degree, however, Berkshire has as owners a very large corps of individuals and families that have elected to join us with an intent approaching “til death do us part.” Often, they have trusted us with a large – some might say excessive – portion of their savings.

Berkshire, these shareholders would sometimes acknowledge, might be far from the best selection they could have made. But they would add that Berkshire would rank high among those with which they would be most comfortable. And people who are comfortable with their investments will, on average, achieve better results than those who are motivated by ever-changing headlines, chatter and promises.

Long-term individual owners are both the “partners” Charlie and I have always sought and the ones we constantly have in mind as we make decisions at Berkshire. To them we say, “It feels good to ‘work’ for you, and you have our thanks for your trust.”

The Annual Meeting

Clear your calendar! Berkshire will have its annual gathering of capitalists in Omaha on Friday, April 29th through Sunday, May 1st. The details regarding the weekend are laid out on pages A-1 and A-2. Omaha eagerly awaits you, as do I.

I will end this letter with a sales pitch. “Cousin” Jimmy Buffett has designed a pontoon “party” boat that is now being manufactured by Forest River, a Berkshire subsidiary. The boat will be introduced on April 29 at our Berkshire Bazaar of Bargains. And, for two days only, shareholders will be able to purchase Jimmy’s masterpiece at a 10% discount. Your bargain-hunting chairman will be buying a boat for his family’s use. Join me.

February 26, 2022

Warren E. Buffett Chairman of the Board

Comments