Big Tech earnings are coming to an end. Tesla's net profit soars, and Amazon is the king of cash.

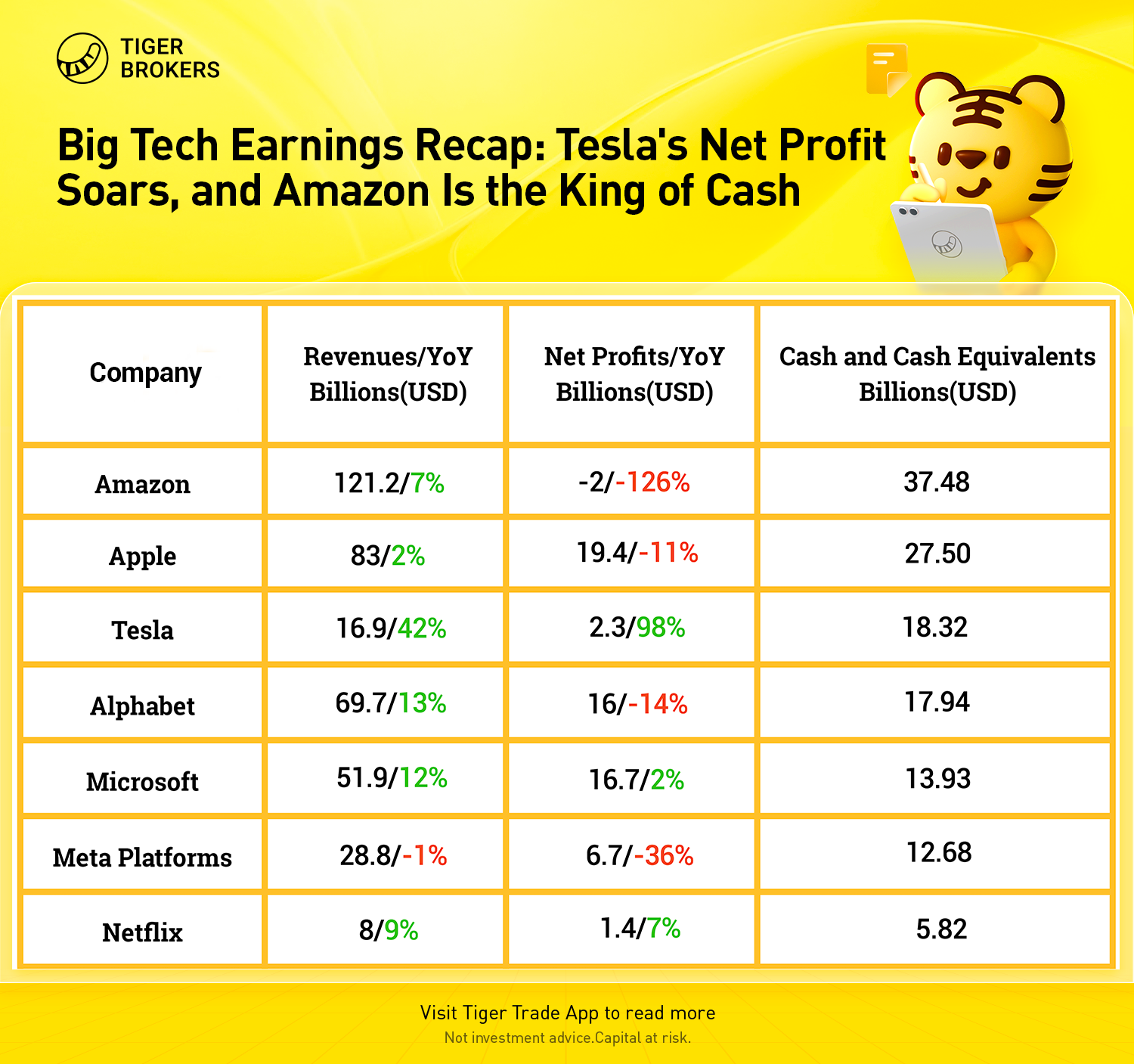

The latest earnings are that Microsoft and Google reported stable revenue growth and margins that are unchanged from recent macro conditions. The strong margins were especially welcomed as many companies have been missing on operating margins and cash flow. Meanwhile, Microsoft delivered free cash flow of $17.8 billion and net profits of $16.7 billion along with upbeat guidance for the year. Similarly, Google reported strong free cash flow of $12.6 billion and net profits of $16 billion in the recent quarter.

The same was not true for Meta, which primarily stumbled on its Q3 guide. The company reported its first decline in revenue in company history and guidance for next quarter missed due to FX headwinds. Analyst expectations for Q3 were for $30.4 billion, or 5% growth. Instead, the company guided for $26 billion to $28.5 billion, or a YoY decline of 6% at the mid-point of the guidance with the current exchange rates creating a 6% headwind.

Amazon: Consumer Demand Resile

Amazon.com Inc said it expects a jump in third-quarter revenue, as the retailer collects bigger fees from Prime loyalty subscriptions and as consumer demand remained high in spite of rising inflation.

Amazon, like much of the retail industry, is facing a reckoning. Major rival Walmart Inc this week said it would make much less this year than it once expected. U.S. consumer confidence has tumbled to a recent low, and some are sticking to lower-priced essentials to manage economic woes.

That has not stopped Amazon. The online retailer projected net sales between $125 billion and $130 billion for the summer period, while analysts were expecting only $126.42 billion, according to IBES data from Refinitiv.

Still, sales growth has slowed year-over-year in some of the retailer's business segments. In North America, the company's largest market, net sales climbed 10% in the just-ended second quarter, compared with a 22% gain in the same period a year ago. Its international unit saw an outright decline of 12%.

Apple: Strong results despite challenges

Apple released strong results despite the challenging macro environment, strong US dollar, and supply chain issues. Revenue grew by 1.9% YoY to $83 billion, which was in-line with the analysts' estimates. It reported EPS of $1.20, which beat estimates by $0.04 (4% beat).

The product segment revenue declined marginally by 0.9% YoY to $63.4 billion and the services segment revenue grew by 12% YoY to $19.6 billion. The company’s installed base of active devices reached an all-time high. It had more than 860 million of paid subscriptions, up 160 million in the past year.

The company did not give exact revenue guidance for the next quarter. Tim Cook, CEO of the company, said in the earnings call,“We’re going to accelerate revenues in the September quarter as compared to the June quarter and will decelerate on the Services side.”

The company’s gross margin was 43.26%, compared to 43.75% in the previous quarter and 43.29% in the same period last year. It was above the management’s guidance of 42% to 43%.

Net income was $19.4 billion or $1.20 per share compared to $21.7 billion or $1.30 per share in the same period last year. It beat the analysts' EPS estimates by $0.04.

The company had cash and marketable securities of $179 billion and a debt of $120 billion. The company reported strong operating cash flows of $23 billion (28% of revenue). The company returned over $28 billion to the shareholders in the recent quarter in the form of dividends and share repurchases.

Tesla: Profit Beats Estimates, Keeps 50% Output Growth Target

Tesla on Wednesday reported a smaller-than-expected drop in quarterly profit, helped by a string of price increases for its cars, which Elon Musk later said were "embarrassingly high" and could hurt demand.

Tesla also sold a majority of its bitcoin holdings, which led to smaller-than-expected impairment charges caused by a decline in the value of the cryptocurrency, analysts said.

Chief Financial Officer Zachary Kirkhorn said Tesla was still pushing to reach 50% growth in deliveries this year, adding that while the target had become more difficult, "it remains possible with strong execution."

Tesla's China factory ended the second quarter with a record monthly production level, after being forced to shut down due to COVID-19 related lockdowns.

Musk said new factories in Berlin and Texas aimed to produce 5,000 cars a week by the end of the year, adding that Berlin produced 1,000 cars a week in June. He had previously said the new factories were "gigantic money furnaces."

The EV maker posted an adjusted profit of $2.27 per share for the second quarter ended June versus analysts' consensus estimates of $1.81.

Automotive gross margin fell to 27.9%, down from a year earlier and the preceding quarter.

Total revenue fell to $16.93 billion from $18.76 billion a quarter earlier, ending its streak of posting record revenue in recent quarters. Analysts expected $17.10 billion, according to Refinitiv.

Alphabet: Search is Resilient

The company reported revenue of 13%, or 16% in constant currency, for a total of $69.7 billion. The operating margin was flat year-over-year, which is a win. Operating expenses grew 24% yet the operating margin was in line with previous quarters at 28% for $19.58 billion in operating income.

The net margin was a bit weaker than previous quarters in 2021 at $16 billion yet in line with last quarter. The company has free cash flow of $12.6 billion. The company has $125 billion in cash and marketable securities. The company reported EPS of $1.21 compared to $1.36 for the same period last year.

Search was stable given the current environment at 13.5% growth to $40 billion and this provided relief that not all ad spend has been paused. Search was strong last quarter at 24% growth to $40 billion, and was flat sequentially in terms of total dollar amount.

The effects of Google’s large R&D department and advances in AI cannot be overstated when it comes to the resiliency of Search in the current environment. We are getting a very slight glimpse of what’s to come for Google in terms of its advertising dominance.

The expectations were that YouTube would weigh on the report yet YouTube provided a bit of growth at 5% year-over-year. The company was adamant that YouTube growth is low because of the tough comps. The tough comps was touched on many times, such as this: “the modest year-on-year growth rate primarily reflects lapping the uniquely strong performance in the second quarter of 2021.”

Notably, Google Cloud slowed to 35.6% growth down from 43.8% growth last quarter. This means Google Cloud is growing slower than Azure on a lower revenue base. This is something to monitor in the future.

Microsoft: Double-Digit Guide for FY2023

Many tech companies are declining to give guidance while Microsoft’s management provided strong guidance in both Q1 FY2023 and for FY2023. For Q1 FY2023, management provided a 10% guide across product lines for next quarter (this includes FX headwinds) and also provided guidance for fiscal year 2023 ending in June: “We continue to expect double-digit revenue and operating income growth in both constant currency and U.S. dollars. Revenue growth will be driven by continued momentum in our commercial business and a focus on share gains across our portfolio.”

Revenue grew by 12% YoY to $51.9 billion (missed Wall Street analysts' estimates by 0.94%) and EPS came at $2.23 (missed estimates by 2.9%). The strong US dollar negatively impacted the revenue by $595 million and EPS by $0.04. Microsoft Cloud revenue grew by 28% YoY to $25 billion. The company’s results are good considering the various macro uncertainties, China lockdown, and the strong US dollar. FY2022 revenue grew by 18% YoY to $198.3 billion and net income increased by 19% YoY to $72.7 billion.

The company’s gross income increased 10% YoY to $35.4 billion. The gross margin decreased by 147 bps to 68.2% when compared to the same period last year. Excluding the impact from the change in the accounting estimate, the gross margin was relatively unchanged.

The operating income increased by 8% YoY to $20.5 billion. The operating margin decreased by 187 bps to 39.5%. Excluding the impact from the change in the accounting estimate and FX, the operating margin would be relatively unchanged.

The company’s cash flows continued to be strong in the recent quarter. Cash from operations grew by 8% YoY to $24.6 billion (47% of revenue) and free cash flow increased by 9% YoY to $17.8 billion (34% of revenue). The company has cash and investments of $104.8 billion and debt of $49.8 billion.

Despite weakness in PCs, the company’s other segments continue to grow. Intelligent Cloud grew 20% YoY to $20.9 billion and Productivity and Business Processes segment grew 13% YoY to $16.6 billion.

The company also made an accounting change in the useful life for server and network equipment assets from four to six years which will extend the depreciation expenses for the company.

Amy Hood said in the earnings call, “First, effective at the start of FY '23, we are extending the depreciable useful life for server and network equipment assets in our cloud infrastructure from 4 to 6 years, which will apply to the asset balances on our balance sheet as of June 30, 2022, as well as future asset purchases.

As a result, based on the outstanding balances as of June 30, we expect fiscal year '23 operating income to be favorably impacted by approximately $3.7 billion for the full fiscal year and approximately $1.1 billion in the first quarter.”

Meta: Misses Q3 Expectations

The market does not need a perfect quarter for Q2 given the numerous headwinds facing tech companies. What the market does need is a sign that a company may have bottomed and is able to guide growth (even if minimal) from Q2-Q3.

In Q2, Meta’s revenue declined for the first time in history. This was expected. However, what was not expected was the lower guide for the next quarter. The company guided for $26 billion to $28.5 billion, or a YoY decline of 6% at the mid-point of the guidance. The guidance takes into consideration the weak advertising demand the company experienced in the recent quarter and also the foreign exchange headwinds of 6%. The investors were expecting a return of growth in the next quarter.

The company had a slight beat on DAUs at 1.97 billion versus 1.96 billion expected. Monthly users were 2.93 billion slightly missed expectations of 2.94 billion.

Operating expenses rose 22% YoY to $20.4 billion. This led to the drop in the operating margin to 29% in the recent quarter compared to 43% in the same period last year. It also led to the 36% YoY drop in the net income to $6.69 billion. The EPS came at $2.46 compared to $3.61 in Q2 2021.

The company is looking to further reduce the operating expenses for the year to $85 billion to $88 billion from the last quarter guidance of $87 billion to $92 million and the prior estimate of $90 billion to $95 billion.

Netflix: Customer Growth Forecast Eases Wall Street Concerns

Netflix averted its own worst-case scenario of subscriber losses, posting a nearly 1 million drop from April through June, and predicted it would return to customer growth during the third quarter.

Investors took the forecast as a signal that Netflix could still find new subscribers despite a rocky global economy and signs of saturation in its biggest market, the United States and Canada.

Netflix lost 1.3 million customers in the United States and Canada in the second quarter, and 770,000 in Europe, the Middle East and Africa. That was offset by a gain of nearly 1.1 million members in the Asia/Pacific region.

Netflix remains the dominant streaming service with nearly 221 million global paid subscribers. Co-CEO Ted Sarandos said the company still sees room for "enormous" growth by attracting many of the billions of people worldwide who have yet to sign up.

Comments