Summary

- This is an updated coverage of an analysis I published in August 2021 on Intel Corporation.

- The main update is twofold. First, it has just released its 2022 Q1 earnings and some of the financials in my original analysis need updating.

- Second, the business fundamentals have also changed in several respects.

- Both its fab initiative and Mobileye have achieved major milestones, and it also announced new R&D and fab investments in Europe.

- All told, it is a growth stock priced as a value stock. It is similar to owning an equity bond with ~9% yield and coupon payments that grow up to ~9% per year.

The investment thesis

This is an updated coverage of an analysis I published on August 26, 2021, on Intel Corporation (NASDAQ:INTC). That article argued that INTC was a good fit for Buffett’s 10xPretax Rule. At that time, it was valued at 10x of its pretax earnings, and the article argued it was similar to owning an equity bond with a 10% yield and at the same with a coupon payment that increases 6~9% per year.

Since then, a few things have changed and the thesis deserves a reassessment. The conclusion is that it is still a good fit for Buffett’s 10x pretax rule. And I am still maintaining my bullish thesis and am optimistic about its double-digit annual return potential in the next few years. More specifically, the updates will be twofold.

First, the bad news is that both the stock price and its earnings have declined since then. The earnings have declined faster than the price, so as a result, the valuation has slightly expanded to about 11.6x pretax earnings now. Thus, its valuation is not exactly the best fit for the 10x pre-tax rule anymore, but still pretty close. And we will interpret the valuation implications more closely when we review its financials released in the 2022 Q1 earnings call.

Secondly, this article will also provide an updated evaluation of its growth potential. Since my last thesis, there have been more developments in these new growth areas such as the fab initiatives and Mobileye. And in Q1 2022, 3 of its 6 newly formed business segments (NEX, Mobileye, and IFS) all achieved record quarterly revenue. Going forward, it projects large CAPEX expenditures in the next few years (around $27B in 2022 alone) to support further growth. We will explore the implications of these developments in our thesis too.

What is Buffett’s 10x Pretax Rule?

As detailed in my other earlier writings, it is not a coincidence that many of Buffett's best and largest investment successes are from buying businesses at 10x pretax earnings, because:

- Buying an average business that stagnates forever at 10x pretax would already provide a 10% pretax earnings yield, directly comparable to a 10% yield bond.

- In case you get to buy an above-average business (like INTC here) at 10x pretax, then any growth would be a bonus on top of the 10% yield above, leading to a double-digit return.

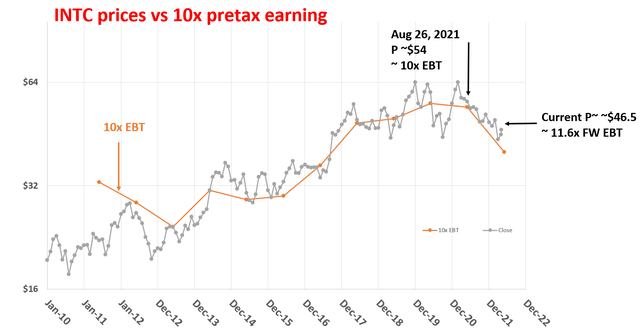

As seen from the chart below, the market now presents INTC as such an opportunity. The following chart shows the price history of INTC and its 10x pretax earnings. Pretax earnings are also referred to as "EBT", Earnings Before Taxes, in this article. As seen, for a business like INTC, whenever the price is near or below 10x EBT, it had a good time to buy (and vice versa). At the time of my last analysis, its valuation was at 10x EBT, and now it is about 11.6x FW EBT. Not the exact fit for the 10x EBT rule, but pretty close.

Source: author based on Seeking Alpha data

So, in this case, even if INTC stagnates forever, by paying 11.6x pretax, the investment would already provide a 9% pretax earnings yield, directly comparable to a 9% yield bond. And to be seen next, INTC has an excellent prospect to grow also.

As also detailed in my earlier writings, a strong warning is in order here:

- I am NOT suggesting you go out and start buying every/any stock that is below 10x EBT. Investors face two major risks A) quality risk or value trap, i.e., paying a bargain price for something of horrible quality, and B) valuation risk, i.e., paying too much for something of superb quality. The 10x pretax rule is mainly to avoid the type B risk AFTER the type A risk has been eliminated already.

- Then how do we eliminate type A risks? I look for three things primarily. First, the business should have not an existential issue in the long run (largely a subjective judgment in the end). Second, the business should have no existential issue in the short run either. This can be quite reliably and objectively evaluated based on the cash flow and debt coverage. And finally, the business should have a decent chance to grow its earnings in the long term (and estimate the so-call perpetual growth rate). This will be a plus.

So with this framework, let’s examine INTC more closely.

INTC: does it have any short-term existential issues?

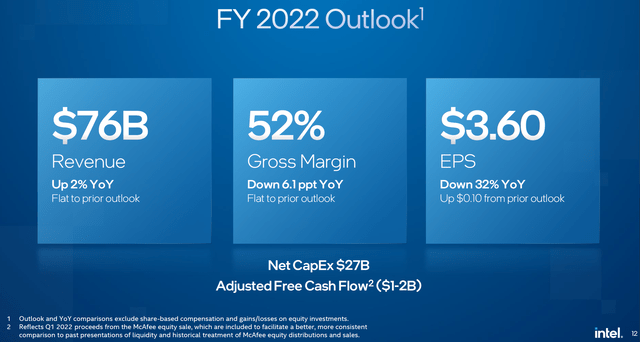

With INTC's market-leading position, scale, and management, I do not see any short-term survivability issues at all. As a matter of fact, INTC just affirmed a quite healthy 2022 outlook as shown below.

It projects a $76 billion revenue, representing a 2% year-over-year growth. And the management raised its EPS guidance by about $0.10 to $3.6 (non-GAAP) from its previous guidance. Note that the GAAP EPS outlook is $4.19. Also, the outlook for the tax rates is 9% in GAAP terms and 12% in non-GAAP terms. In my analysis here in this article, I used an effective tax rate of 10%.

Another reliable metric for checking on the short-term survival issue is debt coverage. The business is essentially debt-free with an average debt coverage above 50. Looking forward, its debt coverage will be a bit lower with the lowered EPS guidance and the heavy CAPEX expenditures expected. But it is still above 40 based on my projections, nowhere near levels that need to be concerned.

INTC 2022 Q1 earnings report

NTC: does it have any long-term existential issues?

If any of us think INTC has issues surviving in the long term (say 10 to 20 years), it is probably mainly because of the competition from other chipmakers like Advanced Micro Devices (AMD), NVIDIA Corporation (NVDA), et al. I think these perceived threats are exaggerated for several reasons.

- Investors should not be too alarmed by the competition, especially not by the quarter-to-quarter fluctuations in their active users and margins. Furthermore, the pie is getting bigger at the same time. Emerging technologies such as autonomous driving, artificial intelligence, and smart appliances create an almost insatiable demand for chips. The global market for Multi-Core Processorswas estimated at $36.2 Billion in the year 2020. It is projected to reach $76.5 Billion by 2026, growing at a CAGR of 13.3%.

INTCiswell-positioned to compete on scale, existing products,new products, and its fabrication initiatives, etal.INTC's new CEO, Gelsinger's priorities on manufacturing are expected to tap into a high growth area and further diversify its revenue sources.

At the same time, the chip business also enjoys the government’s long-term support. The government now understands the chip business is a matter of national security. And INTC’s investment in foundry also enjoys support from the U.S. government. The Biden administration had recently pledged $52 billion toward building out domestic production.

As such, the current valuation views INTC as a business that will never increase profits, but I think in the mid to long term, it will – which brings me to the third and last requirement.

INTC 2022 Q1 earnings report

INTC: what are its perpetual growth prospects?

With the above, I would be already happy to buy a quality business like INTC at 10x EBT if it stagnates forever. But in INTC's case, I think there are good perpetual growth prospects too. As detailed in my original article,

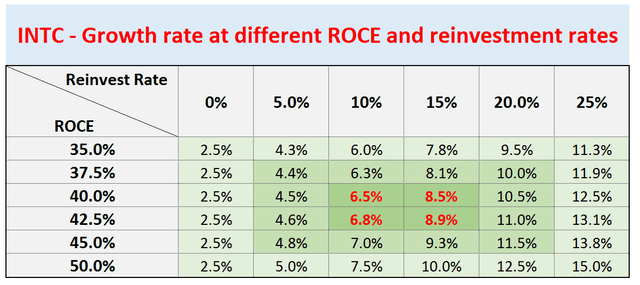

In the long term (like 10 years or more), the growth rate is “simply”:

Longer-Term Growth Rate = ROCE * Reinvestment Rate

ROCE stands for the return on capital employed.

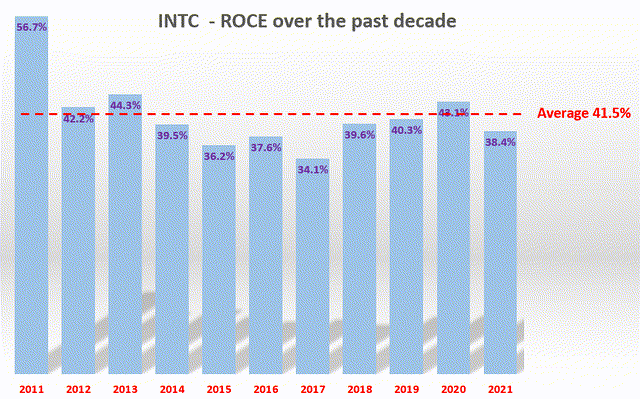

Detailed analysis of ROCE has been provided in my earlier article and I will just show the results directly. As seen, it was able to maintain a respectably high ROCE over the past decade: on average 41.5% for the past decade.

Source: author.

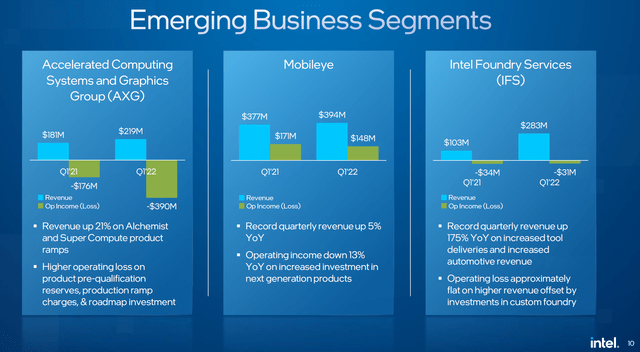

I am optimistic that INTC can maintain and even improve its ROCE In the near future. It has been pursuing several high-growth and high-margin future directions. In Q1 2022, 3 of its 6 newly formed segments (NEX, Mobileye, and IFS) all achieved record quarterly revenue. Mobileye saw a record quarterly revenue of $394M, up 5% YoY. Mobileye also demonstrated its Level 4 self-driving system in Jerusalem, a major milestone in preparation for its upcoming robotaxi services. IFS also saw record quarterly revenue up 175% YoY thanks to increased tool deliveries and increased automotive revenue.

Going forward, INTC projects large CAPEX expenditures in the next few years to support further growth. We will explore the sustainability and implications of the CAPEX expenditures next.

INTC 2022 Q1 earnings report

With the ROCE estimated, we can estimate the long-term growth rate, as shown in the next chart. This table shows the long-term growth rate at different combinations of ROCE and reinvestment rate. I assume a 10~15% as a long-term reinvestment rate for INTC even though it will be reinvesting more in the next few years due to the foundry initiative. Note that in this table, I also added 2.5% of inflation to the growth rate. I think this is justified as INTC has demonstrated in the past it has the pricing power to adjust for inflation.

As seen, the long-term growth rate is in the single upper-digit range, about 6~9%. Now to put the pieces together and conclude:

- In INTC's case here, its current valuation is about 11.6x EBT, equivalent to a 9% yielding equity bond.

- At the same time, there is a good prospect of 6%~9% long-term growth – a growth rate that can be funded organically and sustained by the business itself.

- So an investment here is similar to owning a bond with a ~9% yield and at the same time with the coupon payment increase of 6~9% per year, leading to very favorable odds of double-digit return in the long term.

Source: author.

Final thoughts and risks

This article analyzes INTC, an industry leader that is for sale around 11.6x EBT. The current valuation views INTC as a business will stagnate permanently. Well, under its current valuation, our investment generates a handsome return already if it does.

Furthermore, on the contrary, there are good odds that it can grow its profits, by a healthy 6~9% per year. Its strategic initiatives in AXG (Accelerated Computing Systems and Graphics Group), IFS (Intel Foundry Services), Mobileye, and new expansion of R&D and fab investments in Europe add further growth catalysts.

Although, INTC faces some macroscopic risks and also risks unique to its operations as detailed below:

- Macroscopic risks. The Ukraine/Russian conflict is a big near-term uncertainty. The ripple effects (such as disruption to the supply chain) create further and higher-order risks.

- Also, the PC demand is showing a declining trend in the post-COVID market, which can soften the demand for INTC chips. The COVID pandemic has boosted PC demand when people change their working habits, and now the worldwide PC demand is showing signs of renormalization. The duration and degree of such decline is an uncertainty.

- In the longer term, INTC competes with other players in the chip space. Even though INTC still dominates the chip market, it has lost significant market share to AMD in recent years.

Comments