Tesla delivered 343,830 vehicles in the third quarter, missing analysts' expectations of 358,520 vehicles, suggesting third-quarter revenue may be lower than expected.

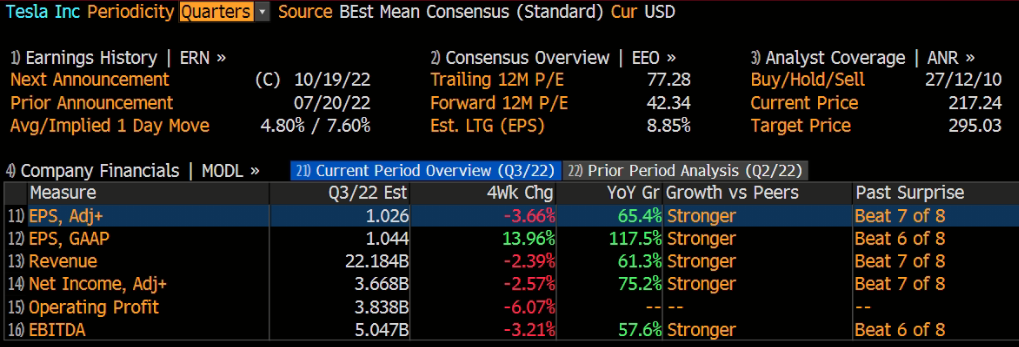

Tesla Inc. announced that it will release its Q3, 2022 earnings report after the closing bell on Wednesday, October 19. Analysts anticipate the revenues of Tesla to reach 22.18 billion, up 61.3% from the same period of the last year. It is expected that Tesla to post earnings of 1.026 per share, up 65.4% year-over-year.

Overall, the Street is optimistic about Tesla stock, with a Buy consensus rating based on 27 Buys, 12 Holds, and 10 Sells. The average price target of $295.03 implies a 35.8% upside potential from current levels.

Things To Watch Before Q3 Earnings Release

Tesla Q3 Deliveries Reach a Record

Tesla Inc. delivered a record 343,830 cars worldwide in the third quarter, 42% higher than the prior year period. Tesla had said that its delivery count is conservative and that final numbers could vary by 0.5% or more. The company produced 365,923 vehicles for the quarter, representing a pace of 1.45 million vehicles produced annually.

However, the Q3 delivery miss is just a short-term speed bump. Tesla produced 365,923 vehicles in Q3 and delivered 343,830. These numbers still represent remarkable growth (in the range of 40-50% YOY growth and the range of 30-40% QoQ).

The company said it is working to find enough "vehicle transportation capacity and at a reasonable cost." Those logistics issues for shipping finished products are magnified thanks to the sharp increase in production growth.

That's a good problem to have and should really encourage investors rather than scare them. Many EV makers are having trouble getting parts, but Tesla is navigating supply chain disruptions well.

The carmaker doesn’t break out sales by geography, but the U.S. and China are its largest markets. The overwhelming number of sales were of the Model 3 sedan and Y crossover, with 325,158 delivering in the third quarter.

Quarterly deliveries are among the most closely watched indicators for Tesla since they underpin the carmaker’s financial results. Though legacy automakers and new entrants alike are bringing more EVs to market, Tesla has led the charge for battery-powered cars since the first Model S sedans were delivered to customers a decade ago.

According to new registration data from Experian, Tesla now has about two-thirds of the EV market in 2022 as of August.

Tesla’s supremacy is not expected to be challenged much in the short term due to the massive lead, but several electric vehicles are expected to see significant ramp-ups in the short term.

Tesla Has Improved its Optimus Robot

As Tesla's Humanoid Robot is still under development, they were able to show their prototype "Bumble C," which is to become a low-cost and mass-producible Optimus robot. Tesla has significantly improved its Optimus robot in a very short time.

The initial release and demonstration of the product was followed by a variety of reactions from experts in the robotics industry and the investment community. Interestingly, Tesla received high praise from experts from the robotics industry, while there were many skeptics from the investment community.

The Tesla stock has been tumbling ever since AI Day with other issues like weaker-than-expected delivery results and the news of Elon Musk announcing he was purchasing Twitter again.

Right before Tesla’s AI Day started, the stock price was at $265.25. The Tesla stock price has plummeted since, it’s priced at $219.35 as of October 18. The market is not always rational and overreacts to the news cycle as it attempts to forecast the future months ahead of time.

Many experts were hoping for a clear update on when fully self-driving cars and working robots would be ready to launch. The Optimus was clearly not yet a working robot, even though Musk speculated that they would be able to mass produce it and sell it for less than $20,000 in three years. AI experts were not impressed by the limited capabilities of the robot, and they felt that Musk had overpromised.

Optimus is intended for mass production (i.e., thousands or millions of units). Project progress was made in just 6 to 8 months, compared with decades at competitors. The robot is expected to be affordable, costing only US$20K to manufacture, or "significantly less expensive than an EV."

Tesla's robot may not have the same dexterity and human-like character because it is not primarily intended to perform tasks such as parkour or dancing. Tesla has a head start on developing a functional AI-driven humanoid robot.

It is also important to note that this event was not aimed at investors, as the sole purpose was to recruit the best possible talent for Tesla and its Optimus project. Recruiting the most talented engineers and employees at Tesla is a huge advantage for innovation within the company and staying ahead of the competition.

Non-linear Growth Drivers

Looking further out, there are longer-term growth drivers that are highly nonlinear. Currently, TSLA is still a "car" company that derives the bulk of its income from manufacturing and selling cars (84.7% of its total revenue).

However, its other segments, the non-manufacturing segments, are growing rapidly. As a notable example, its automotive services now represent 7.06% of its total revenue. With its FSD potential, such services can break all the limitations of hardware manufacturing. It could become totally scalable just like a software platform, and as a result, enjoys higher-order nonlinear growth.

Tesla isn't just about electric cars, either. The company will share its full third-quarter results on Oct. 19, 2022, and there will likely be other news items of interest from that. CEO Elon Musk has previously said he expects the Tesla Semi battery-electric truck to begin shipping this year and the Cybertruck next year. Those could both become further growth drivers for the company.

The company is also now investigating whether to build a lithium refining facility in the U.S. Its battery production gigafactories support internal production, but Tesla has also been increasing production of battery storage and solar systems that it sells to outside customers. In its second-quarter report, the company said it continues to ramp up Megapack storage production as customer interest "remains strong and well above our production rate."

Cautious Bullishness from Analysts

Goldman Sachs favors Tesla even during an economic slowdown

Goldman said it now expects Tesla to make 2.4 million cars worldwide in 2024, up from its previous forecast of 2.275 million.

The note to its clients revealed that the American investment bank had a buy rating on Tesla with a 12-month price target of $305 — a 40% upside from current trading levels. Tesla shares have fallen by more than 38% this year.

Wedbush analyst considers Tesla’s logistical challenges “a speed bump”

Wedbush Securities analyst Dan Ives said that Tesla’s demand “continues to be robust.” However, Tesla’s demand also continues to “outstrip supply.” Elon Musk and other Tesla executives share the Wedbush analyst’s thoughts on the topic of demand.

“I believe this is more of a speed bump in logistical issue in terms of delivering cars to customers at the end of the quarters rather than ultimately demand really starting to come off,” Ives said.

Wedbush Securities believes Tesla is still a “BUY.” Ives reiterated that the investment firm believes Tesla’s Q3 2022 delivery results are just “a narrow speed bump.” He added that Tesla’s current stock price is a buying opportunity for investors.

Comments