Summary

- Microsoft will acquire Activision Blizzard for $95 per share.

- This makes for a hefty premium compared to where ATVI traded in recent months, but ATVI traded at higher prices one year ago.

- This deal makes a lot of sense for MSFT, as it will be accretive while there is also a strategic rationale to get gaming IP.

- Looking for a helping hand in the market? Members of Cash Flow Kingdom get exclusive ideas and guidance to navigate any climate.

Activision Blizzard, Inc. (ATVI), a leading gaming company, is getting acquired by Microsoft (MSFT), one of the largest tech companies in the world. The deal allows for compelling share price gains for those that bought into ATVI in the recent past when shares were pretty inexpensive. At the same time, I do believe that the takeover also makes a lot of sense for Microsoft. Not only is the deal immediately accretive thanks to ATVI's not very demanding valuation, but Microsoft is also able to access strong intellectual properties and will grow its strategic gaming division massively thanks to this takeover.

ATVI Overview

Activision Blizzard is a company that was, in its current form, created in 2007 when Vivendi (which owned Blizzard) and Activision agreed on a merger. Activision Blizzard is one of the largest gaming companies in the world, with annual sales of around $10 billion. Its intellectual property includes many established and sought-after franchises, including the Call of Duty franchise, the Tony Hawk franchise, the Warcraft and StarCraft franchises, the Diablo franchise, and many more. Some of the company's products utilize a free-to-play approach where in-game upgrades etc. can be purchased, such as Candy Crush. Other titles, such as the CoD franchise, come with a one-time purchase price, while others, such as World of Warcraft, require a monthly subscription fee. Some of the company's IP can be seen in the following graphic:

ATVI IP

ATVI presentation

There is a wide range of products addressing different groups of gamers across age groups, platforms (mobile, PC, gaming consoles), and content. This allows ATVI to address hundreds of millions of gamers with its products, although it should be noted that many of those users are non-paying gamers that play ATVI's free-to-play mobile games. Still, even the company's premium products, such as the CoD franchise and the Blizzard products, have monthly users of more than 100 million (in total), per ATVI's most recent quarterly report.

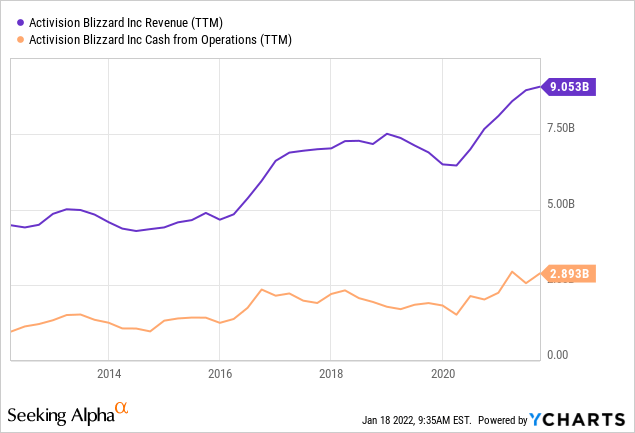

Over the last decade, ATVI has grown its revenue by 100%, and its cash flow by 200%. This makes for an annual growth rate of 7% and 12%, respectively, which I deem attractive. Revenue growth is, at least partially, driven by the growth across the global gaming industry. Playing games across a wide range of platforms is a type of entertainment that is becoming more popular over time, and thatgains shareversus other forms of entertainment, such as watching TV. In this growing market, ATVI didn't have any problems in generating business growth. Thanks to its strong IP and some takeovers, the company was able to grow its business quite meaningfully. Operating leverage, in turn, allowed the company to grow its profits and cash flow significantly faster than its revenue. Producing a title does come with relatively fixed costs, and selling the title to a growing number of consumers leads to outsized gains in profits and cash flow.

The global gaming market will, according to most forecasts, continue to grow rapidly for the foreseeable future. Some experts forecast that revenues will grow by10%+through the 2020s. Even if that turns out to be a too aggressive estimate, it seems pretty clear that global gaming sales will rise in the future. Current consensus estimates see ATVI grow its revenue from a little more than $9 billion this year to $18 billion in 2027, while its earnings per share are forecasted to grow from $3.80 this year to more than $9 over the same time frame. These analyst estimates may not be 100% precise, but they should be in the ballpark of where ATVI's actual results will land. Clearly, Activision Blizzard is thus a company with a compelling longer-term growth outlook, thanks primarily to strong macro tailwinds for its industry.

The Deal With Microsoft

Microsoft agreed to acquire Activision Blizzard for$95 per share, which makes for a 45% premium to the price per share before the deal was announced. This will be an all-cash deal, thus Microsoft will not issue any new shares to finance the acquisition - investors thus don't have to worry about dilution.

At the time of writing, ATVI trades at $86 per share, there thus is considerable room left versus the takeover price of $95. The takeover process will take some time, however, and management has guided that the deal will likely close in 2023. Investors will thus have to wait quite some time if they want to hold out for $95 per share, which is why I believe that selling in the high $80s or low $90s could make sense, as funds could be deployed elsewhere. Investors should also consider the risk that the acquisition could fall through, although I do not deem this particularly likely. It should be noted that it is also possible that another suitor comes out with a competing bid in the coming months, although I do not deem this especially likely, either.

Based on a share count of around 780 million, the deal values the company at $74 billion. We should adjust this for ATVI's net cash position, however, which stands at $6 billion. The actual price that Microsoft will pay for Activision Blizzard, net of cash and debt acquired, is thus $68 billion. For a company with around $3 billion in operating cash flow that isn't a low amount of money, but it isn't especially much, either. In fact, ATVI's cash flow multiple (at the takeover price) of around 23 is lower than Microsoft's current cash flow multiple of 28.

Microsoft is thus acquiring a company that is cheaper than Microsoft itself, even factoring in the takeover premium. At the same time, ATVI is forecasted to grow faster than MSFT, thus this deal looks pretty good for Microsoft: Microsoft can use a portion of its (non-productive) cash pile to acquire a company that is growing faster than itself and that trades at a lower valuation.

At the same time, there is also a strong strategic rationale for Microsoft to do this takeover. Microsoft's gaming franchise is solid, but lacking scale and strong/attractive intellectual property. By acquiring ATVI, with its established huge franchises, such as CoD or Diablo, Microsoft can strengthen its position in an area where it is currently looking relatively weak. At the same time, with Microsoft's massive resources, investments in ATVI's franchises could be increased, which would possibly allow for a better output when it comes to class A titles in the future. Since Microsoft already owns one of the major gaming platforms (Xbox), getting a stronger hold on the software side will make Microsoft a stronger player in the gaming industry overall. I wouldn't be surprised to see Microsoft develop more exclusive Xbox titles in the future, using ATVI's IP, which should also drive sales for Microsoft's gaming hardware side.

What It Means For ATVI And MSFT Shareholders

For Microsoft's shareholders, this seems like a huge win - which is why I was surprised to see MSFT's shares decline initially. Microsoft gets to deploy cash in an accretive way (more accretive than buybacks) while strengthening the company's position in a huge growth market. There is, from Microsoft's side, nothing to dislike about this deal, I believe. I personally think that it makes more sense than the LinkedIn acquisition, for example.

For Activision Blizzard's shareholders, the acquisition looks pretty solid as well - especially for those that bought when shares were pretty inexpensive over the last couple of months. Those that bought in early 2021, when shares traded at as much as $100, might feel that the takeover price is too low. A case could be made that ATVI deserves a higher takeover price based on its future growth outlook, but I believe that ATVI's shareholders are getting a pretty reasonable payment here.

I own shares in both companies, with the ATVI position being a relatively new one, bought in late 2021 at around $65 per share (missing the bottom, which was at $56). I am happy to bag a 30%+ return for a couple of months and plan to sell my shares in the near term, even though I won't receive the full $95 per share by doing so. I might deploy some of the proceeds into MSFT, although not all of them, as I deem Microsoft pretty expensive right now. MSFT is, after all, trading at more than 33x this year's net profits (ATVI, for reference, was trading at just 17x forward profits when I bought my stake).

For those ATVI investors that want to have exposure to ATVI's IP, buying MSFT is a logical choice, although they should be clear about the fact that ATVI will only be a relatively small part of the much bigger MSFT. For those that want to deploy their money into a 100% gaming-focused pick, Take-Two Interactive (TTWO) could be a reasonable choice - its shares have become less expensive following the announcement of the Zynga (ZNGA) deal, and TTWO owns strong IP as well (e.g., GTA).

Comments