Escalating Iran-U.S. tensions continue to roil global markets, with crude oil prices swinging sharply and showing clear signs of a peak. Post-surge oil prices driven by geopolitical conflicts typically follow two trajectories: prolonged consolidation at elevated levels or a sharp pullback. These two scenarios lead to vastly different pricing dynamics for equities, gold, industrial metals and energy commodities.

Iran-U.S. geopolitical frictions have intensified again this week. Following a month of geopolitics-driven trading in March, market risk appetite has gradually recovered, with investors becoming desensitized to negative headlines and pricing shifting toward ceasefire expectations.

According to strategy analysts at GF Securities, equity markets are set to rebound under both oil price scenarios, yet the timing of a sustained rally hinges on inflation peaking, rather than an oil price peak. Persistently high oil prices will fuel stagflation expectations, benefiting gold and energy products, while industrial metals will face downward pressure amid economic recession risks. In the event of a rapid oil price decline, gold will lack sustained upward momentum, and industrial metals will only stage a rally once economic demand recovery is confirmed.

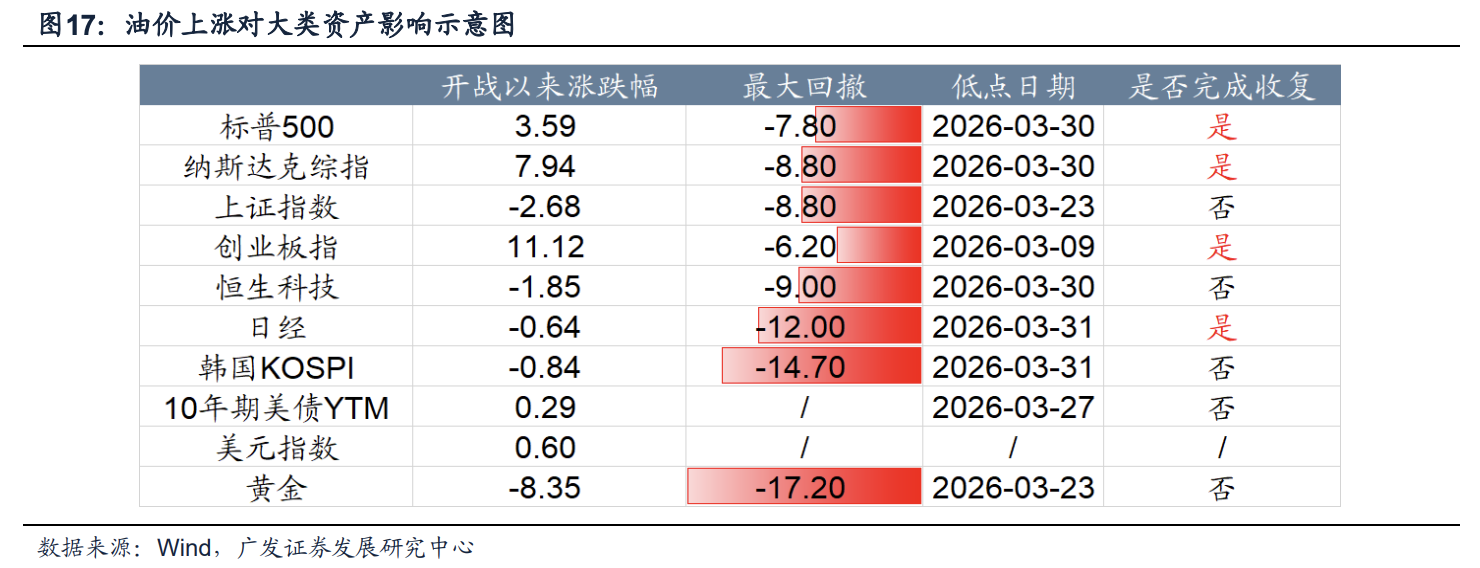

The recovery of major asset classes has become highly divergent. The S&P 500, Nasdaq Composite, ChiNext Index and Nikkei Index have fully erased losses incurred since the outbreak of geopolitical conflicts. By contrast, the Shanghai Composite Index, Hang Seng Technology Index, KOSPI, 10-year U.S. Treasury bonds and gold have yet to complete their recovery, reflecting a highly fragmented market landscape.

Elevated Consolidation, Sharp Correction and Pre-war Macroeconomic Fundamentals

Historically, oil price spikes triggered by wars tend to evolve in two patterns. The first is prolonged high-level consolidation after hitting a peak; the second is a swift retreat to pre-conflict price levels.

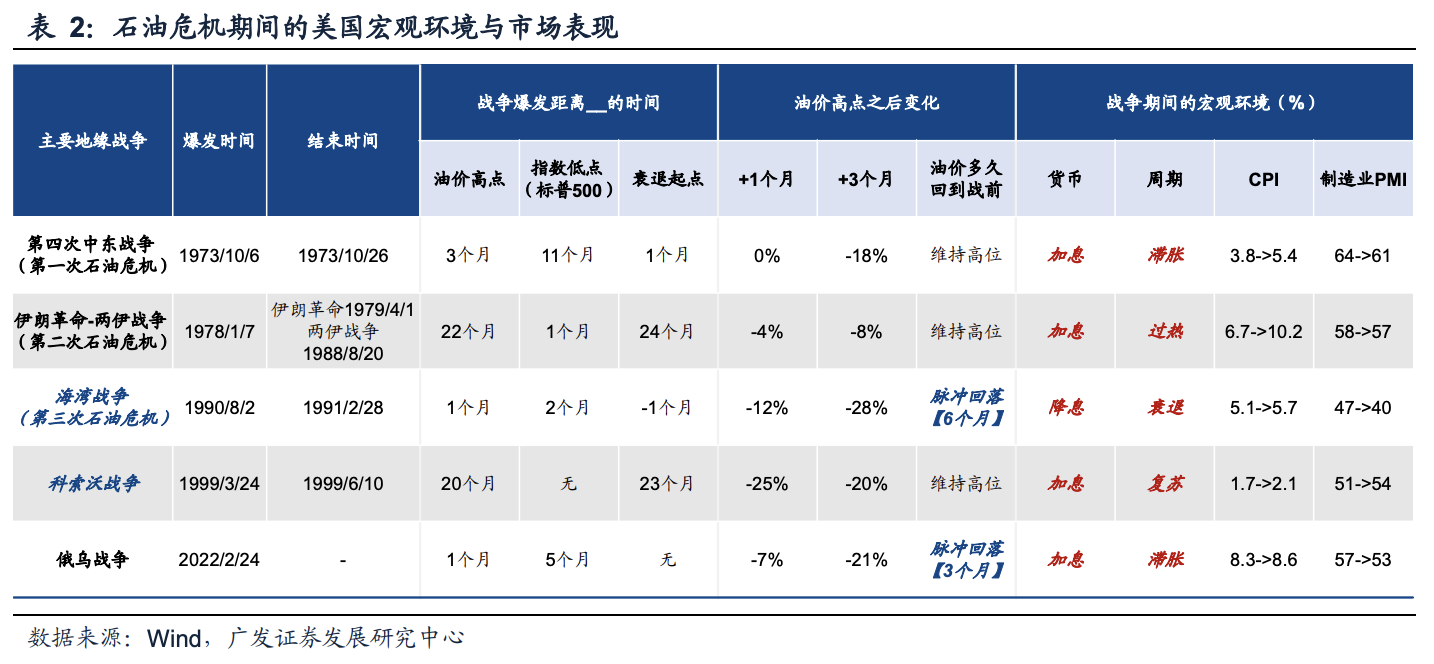

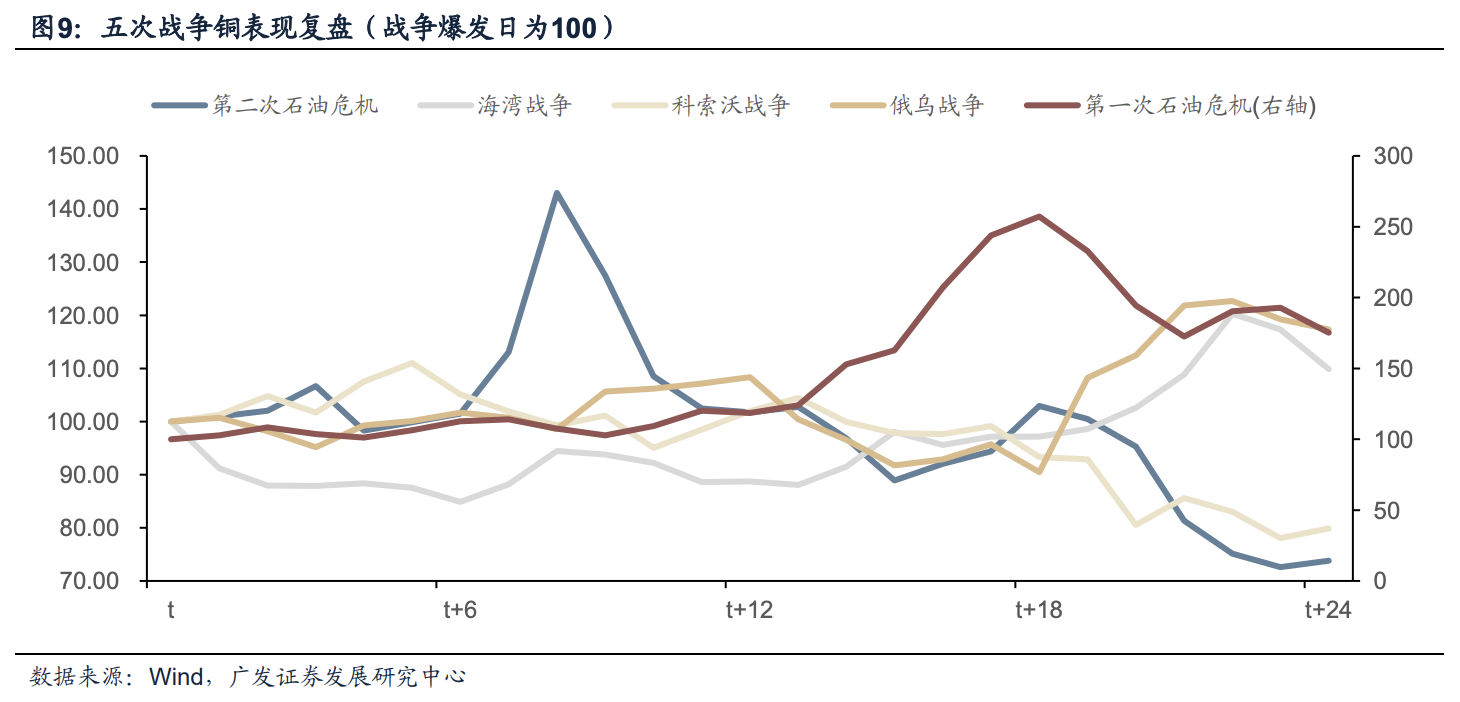

GF Securities reviewed five major geopolitical crises, including the 1973 First Oil Crisis, the 1979 Second Oil Crisis, the 1990 Gulf War, the 1999 Kosovo War and the 2022 Russia-Ukraine conflict. The review reveals systemic differences in asset performance under the two oil price trajectories.

The high-consolidation pattern is represented by the two oil crises and the Kosovo War, while rapid oil price corrections characterized the Gulf War and the Russia-Ukraine conflict. Pre-war macroeconomic fundamentals serve as a core determinant of the magnitude of oil supply shocks.

Ahead of the First Oil Crisis, the U.S. manufacturing PMI stayed firmly above 50 and even exceeded 60, pointing to an overheating economy. Strong consumer demand compounded by supply-side shocks drastically amplified stagflation risks.

Prior to the Gulf War, U.S. GDP growth had slowed from over 4% in 1988 to 2.41% in the quarter before the war, as the economy slid toward recession. This enabled the market to absorb oil price shocks at a much faster pace.

Equity Market: Inflation Inflection Point Remains Core Catalyst for Rebounds

Historical data indicates equities will rebound in both oil price regimes, albeit with distinct timelines and momentum. When oil prices plateau at high levels, stock rebounds take longer to materialize but deliver stronger upside elasticity. A sharp oil price decline, by comparison, supports a much quicker market bounce.

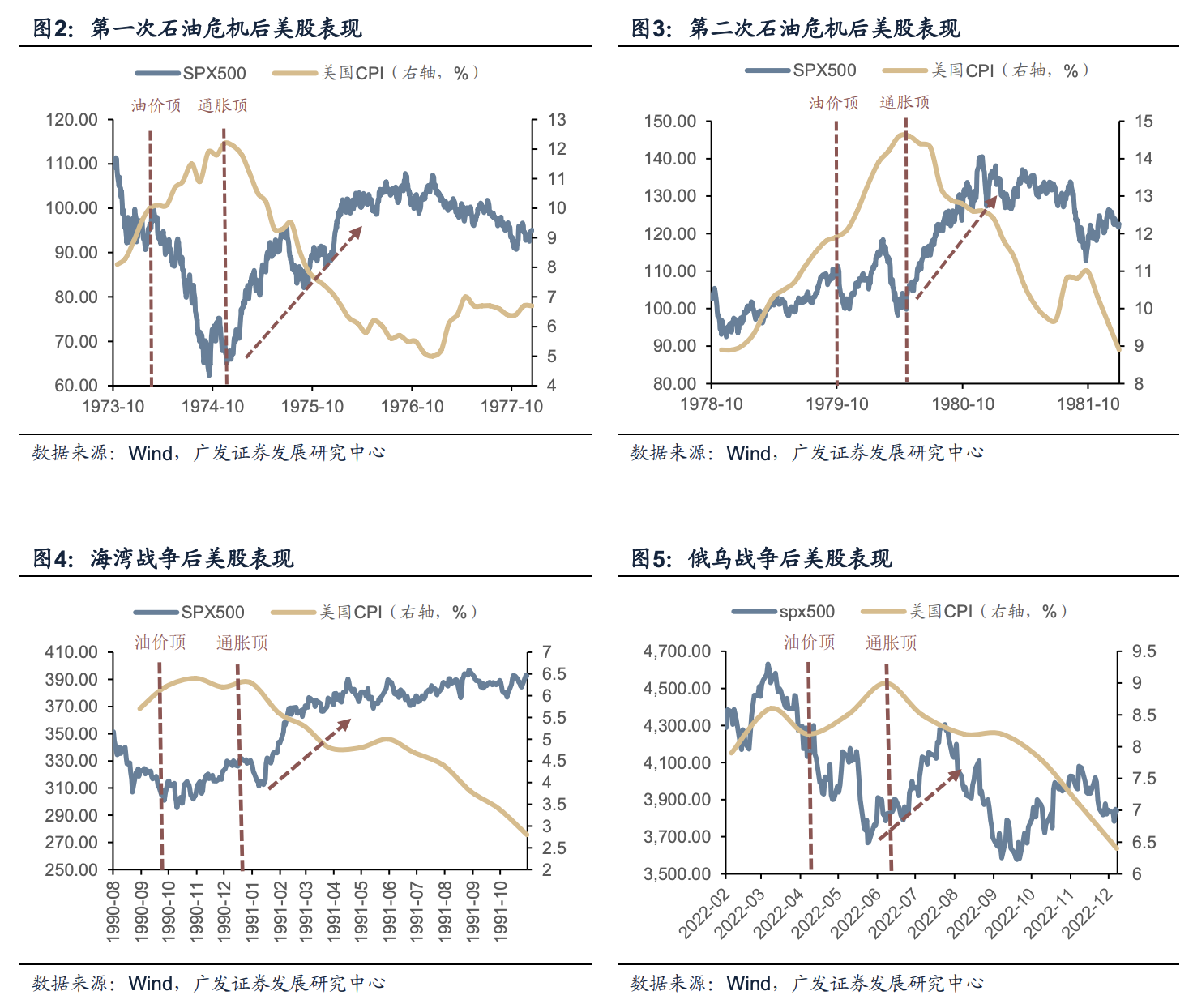

Inflation peaking, instead of oil prices topping out, acts as the decisive signal for market recoveries. The transmission mechanism of oil price shocks on equities remains consistent: higher crude prices fuel elevated inflation, erode corporate earnings and tighten liquidity. This linkage has been validated across five wartime cycles.

Oil price peaks consistently precede inflation peaks. Equities face mounting pressure in the late stage of inflation acceleration, and a sustained uptrend only emerges after CPI growth decelerates from multi-year highs.

Notably, robust industrial prosperity can break this traditional macro transmission chain. During the Kosovo War, oil prices remained elevated, yet the booming internet technology revolution and pre-emptive Fed rate hikes effectively anchored inflation expectations. U.S. CPI saw only a mild uptick, providing strong endogenous support for equity markets.

Divergent Performance: Gold, Industrial Metals and Energy Commodities

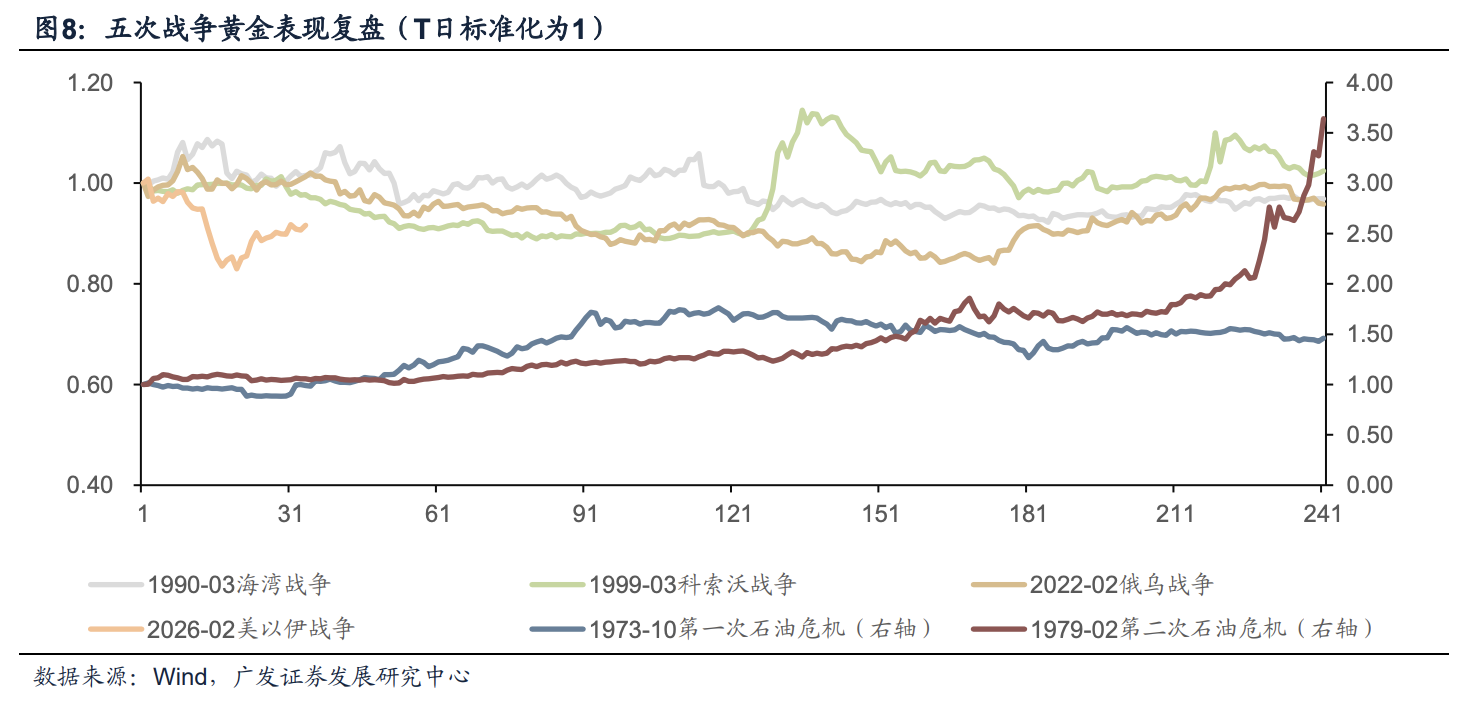

Gold delivers far more pronounced medium and long-term gains in a high oil price consolidation regime. Sustained elevated crude prices lift stagflation concerns, offering solid fundamental support for gold. Bullion registered substantial gains during the two oil crises and the Kosovo War. In contrast, during the Gulf War and Russia-Ukraine conflict marked by rapid oil declines, gold only recouped losses triggered by hawkish monetary policy, without launching a structural bull run.

For industrial metals such as copper, prices initially rise on inflation expectations amid prolonged high oil prices, before declining as recession risks widen supply-demand imbalances. When oil prices correct rapidly, industrial metals fluctuate range-bound in the short term and embark on upward trends only after tangible economic recovery signals emerge.

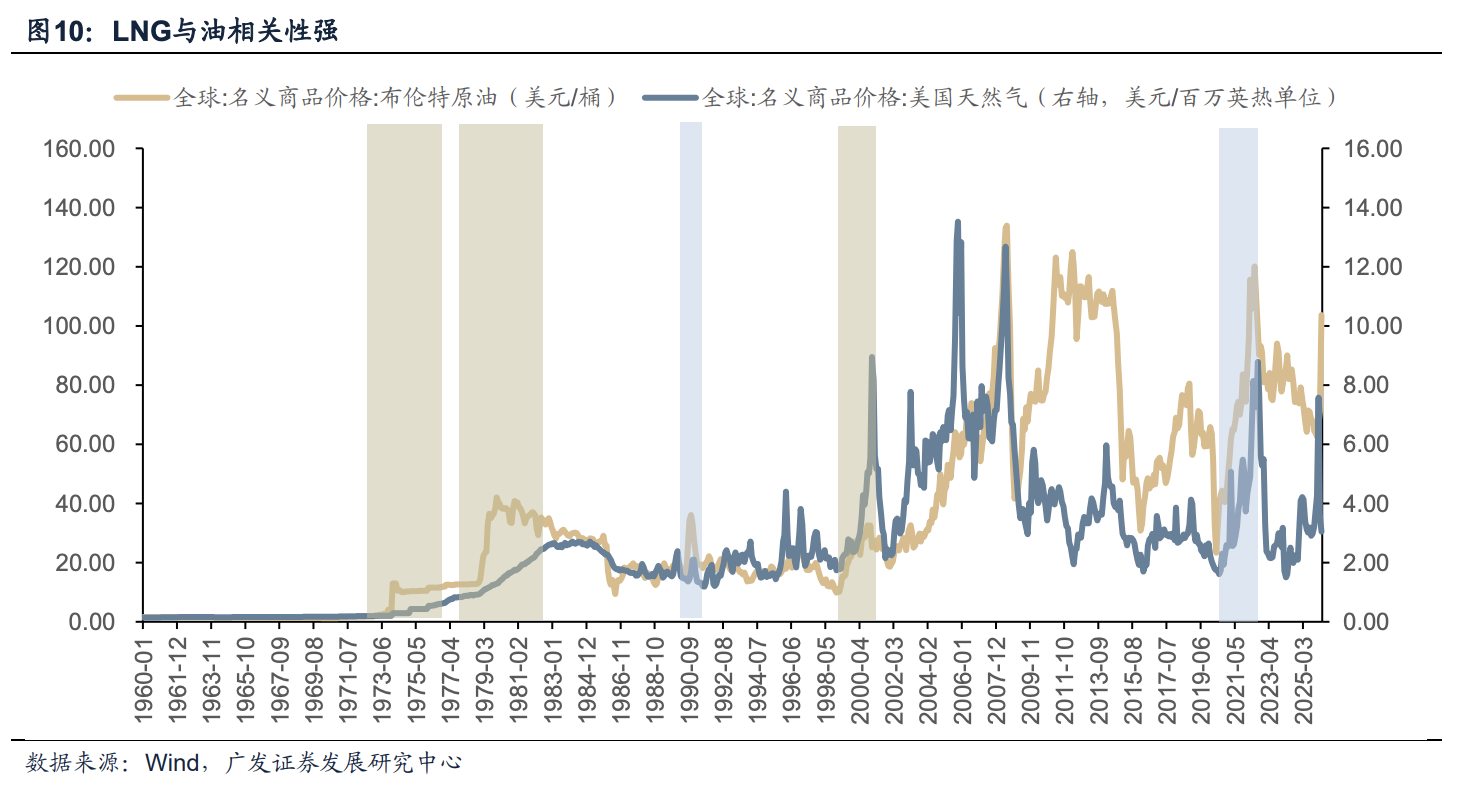

LNG maintains a strong correlation with crude oil. In a high-consolidation oil regime, LNG prices keep climbing; when crude slumps rapidly, LNG prices follow suit with synchronized declines.

The U.S. Dollar Index shows limited long-term correlation with oil prices, and the two assets do not follow a strict inverse relationship. The dollar trades in a firm sideways range when oil stays elevated, before weakening amid rising recession risks and rate cut expectations. A rapid oil price drop, meanwhile, tends to weigh on the U.S. dollar.

Post-crisis Policy Responses: Balancing Inflation Control and Recession Mitigation

Advanced economies share systematic policy responses after geopolitical shocks fade. In periods of high oil prices and entrenched inflation, central banks typically adopt a policy mix of rate hikes followed by cuts. When oil and inflation cool rapidly, monetary authorities tend to implement direct rate cuts.

During the First Oil Crisis, the Fed adopted accommodative monetary policies to counteract economic downturns. However, supply-side shocks unanchored inflation expectations, pushing U.S. CPI and PPI into double-digit territory in 1974. The central bank was forced to launch aggressive monetary tightening, which curbed inflation but triggered a severe recession, before shifting back to rate cuts.

After the Gulf War, faced with supply shocks and weakening demand, the Fed swiftly shifted its policy focus from inflation containment to mitigating recession and credit contraction risks. As CPI moderated and oil prices retraced, the central bank accelerated rate cuts, facilitating a steady economic recovery.

In terms of energy and industrial policies, the two global oil crises drove widespread energy transition across Western economies. Nuclear power generation surged in the U.S., Europe and Japan in the post-crisis era. France launched the Messmer Plan for large-scale nuclear construction, while Japan prioritized nuclear energy to reduce crude oil reliance.

Based on U.S. March inflation data, the spillover effects of high oil prices on inflation are weaker than previously anticipated. Policymakers are likely to prioritize recession risk mitigation and accelerate monetary easing as inflationary pressures ease.

Outlook for Major Assets: Undervalued Hong Kong Stocks and Strengthened Medium-Term Gold Bull Case

GF Securities shared its forward-looking views on global asset allocation:

The U.S. stock market boasts solid fundamentals and sustained AI industrial expansion, underpinning its structural strength over the medium term. Nevertheless, U.S. equities have entered short-term overbought technical territory. The recent recovery is largely driven by short covering and CTA trend capital inflows, rather than proactive long positioning, requiring caution over weaker-than-expected earnings in the technology sector.

Hong Kong equities present attractive short-term valuation upside. The Hang Seng Technology Index has yet to recover geopolitics-related losses and trades at depressed valuation levels, leaving ample room for rebound if ceasefire-related positive catalysts materialize.

In the A-share market, the ChiNext Index has notably outperformed the Shanghai Composite Index, driven by robust earnings growth in high-growth tracks including AI infrastructure and new energy in the first quarter. Heavyweight ChiNext constituents are largely concentrated in high-prosperity sectors such as lithium batteries and optical modules. Allocation structure outweighs overall position size, with four core investment themes recommended: energy storage and lithium batteries; domestic AIDC including semiconductors; overseas AI infrastructure supply chain; AI short drama and comic content sectors.

The medium and long-term bullish logic for gold continues to strengthen. On one hand, central banks maintain steady and rising monthly net gold purchases. On the other hand, weakened U.S. geopolitical control over the Strait of Hormuz may dilute petrodollar dominance and erode the U.S. dollar’s reserve asset status, creating favorable tailwinds for gold.

Comments