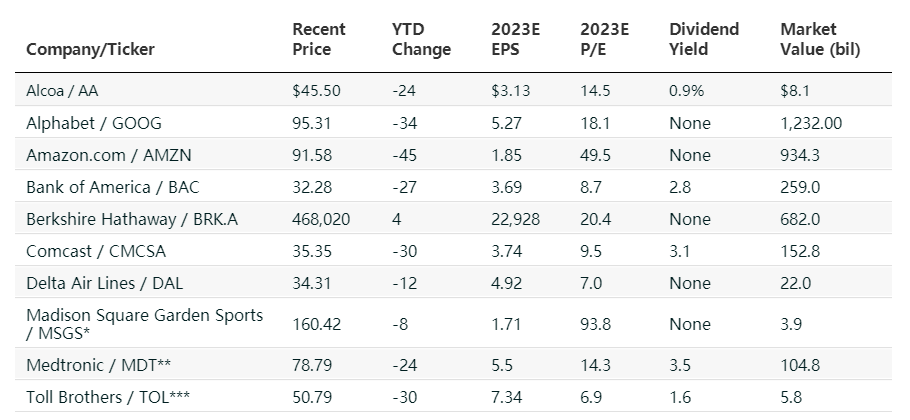

A slowdown at Amazon ‘s cloud-computing and retail units this year hammered its stock, which is off 45% to a recent $91. The coming year should be better, as the company cuts costs and realizes greater efficiencies in its online retail operations after more than $80 billion of investments in fulfillment and transportation over the past three years.

SVB MoffettNathanson analyst Michael Morton, who recently began coverage of Amazon (ticker: AMZN) with an Outperform rating and $118 price target, estimates that Amazon’s retail segment has negative operating margins when excluding lucrative advertising revenue. While Amazon aims to “delight” customers, it also needs to make a profit in its retailing business and is moving in that direction.

“For three years, Amazon has experienced multiple compression as [pretax earnings] estimates declined and capital intensity was greater than expected,” Morton wrote. “We believe we are at the end of the tunnel.”

At 50 times next year’s earnings, Amazon stock isn’t cheap, but few companies have two dominant businesses; the second is Amazon’s highly profitable cloud business, Amazon Web Services, which has ample growth potential. While the stock might not match the 270% gain it posted in 2009 after its last big wipeout, it does seem poised for a better year.

10 for 2023

Good companies at bargain prices could be winners in the new year

Comments