Summary

- Intel forecasts weaker results in the current quarter compared to guidance just at the end of April.

- The chip giant continues to lose market share on the premium chips while chasing an expensive foundry plan leading to substantial gross margin pressure.

- The stock isn't attractive, even at 52-week lows, due to the falling EPS profile.

For years now, investors have tried to bottom fish on Intel(NASDAQ:INTC). The chip giant continues to grab investors on hopes of a return to past glory while the reality is that business continues to sink while competitors take market share. My investment thesis remains ultra Bearish on the lagging chip giant chasing a costly foundry business.

Another Bad Quarter

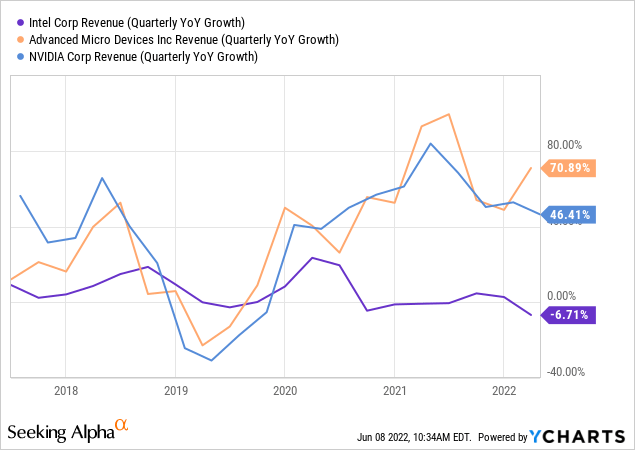

The problem ailing Intel is the last few years is actual growth in the business while chip competitors are reporting booming growth. In most cases, AMD(AMD) and NVIDIA(NVDA) lacked the chip supplies to meet demand due to fast growth. The indication here was that the chip giant would ultimately give up more market share leads once the competitors sourced more supplies from foundries like TSMC(TSM).

At the BoA Securities Global Technology conference, CFO David Zinsner further highlighted the troubles facing Intel:

Macro side, clearly it's weaker you know, and we like everyone else will be impacted by the macro events that are unfolding here more recently, that's clearly going to impact us as it will virtually everybody else in not only the semiconductor industry, but globally in terms of corporations...I think in all three cases the circumstances at this point are much worse than what we had anticipated coming into the quarter. So that certainly is an impact to the business as well.

The chip giant had highlighted three issues facing their business as follows:

- Match set issue with components

- Customer inventory reductions

- China lockdowns

While AMD continues to face issues with supplies keeping up with strong demand in data center and premium PCs, Intel has repeatedly reported problems with demand due to these primary issues repeated by the CFO. Intel had already provided mixed guidance for Q2'22 and the rest of the year.

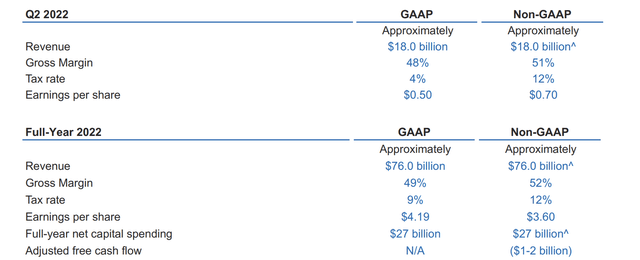

Source: Intel Q1'22 earnings release

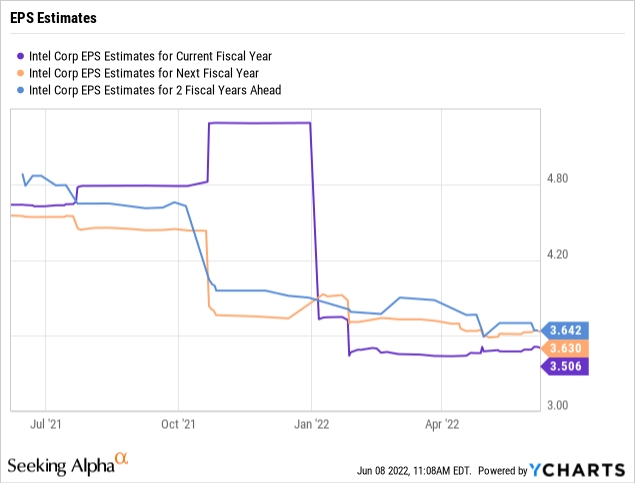

In essence, Intel guided to a slight increase in revenues with EPS plunging to just $3.60. The company actually said numbers are worse than those expectations when guiding back in April. The consensus estimates had the 2022 EPS down at $3.51 rising to $3.63 in 2023 for the trough. In reality, the numbers for the next 3 years are virtually flat around $3.50 to $3.60 per share.

Citi analyst Christopher Danely actually cut 2022 EPS to $2.33, down from $2.63. Nikko Securities analyst cut the 2022 EPS target to $3.40, down from $3.63.

The key here is that both analysts cut numbers far below consensus estimates. In the case of Citi, the analyst was substantially below corporate targets already and still felt the need to cut numbers by $0.30.

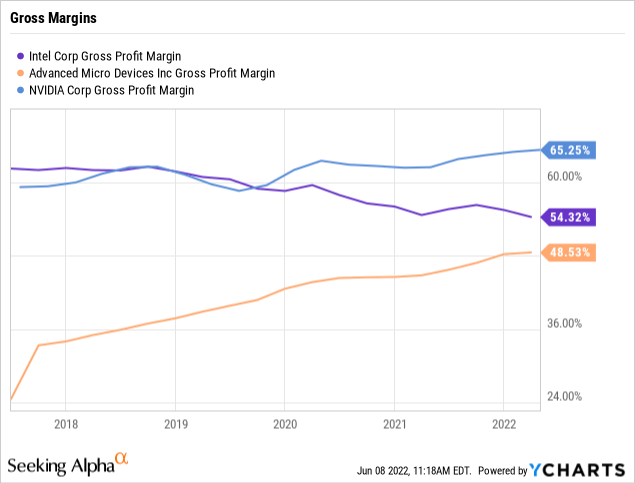

Gross Margin Signal

Intel only guided to gross margins of 51% for Q2'22 and 52% for the year. At these low gross margins, any further pressure very much pressures profits to once unexpected levels for a company once dominating the market with gross margins far above 60%.

The push into the foundry business isn't going to help with these margin pressures either. Per the CFO, the IDM business is in the 50% range now with a goal of approaching 60% in the future.

Only a few years ago, Intel was the leader in gross margins in an indication of the pricing power the firm had due to a leadership position in the market. The forecast is now for AMD to surpass Intel gross margins this year while NVIDIA is the clear leader above 65%.

*Note these are the GAAP gross margins. AMD has guided to54% non-GAAP gross margins this year.

One of the major concerns with the foundry business is the potential for customers to use Intel as a negotiating tool for lower foundry prices. As highlighted in past research, the top TSM foundry customers are all mostly competitors of Intel in various markets, so these chip companies have no interest in using Intel for legitimate production of sensitive chip technology.

The comment by Intel's CFO at the BoA conference continues to suggest a market focused on using the IDM business for pricing concessions:

But to me that has been a big surprise as how engaged we are with customers, that I really would have expected we'd have that level of engagement in or with - that really gives me like a lot of optimism around this business.

Until Intel can tell a better story on gross margins, the stock isn't appealing even at $40. Intel is spending $27 billion this year on capital spending to chase the IDM market. A huge risk remains that all of this spending is chasing a market that might not exist in the volumes forecast by the chip giant when so many of the large chip companies have no reason to trust Intel with sensitive new chip designs.

The biggest news from the Apple(AAPL) WWDC was the new M2 chip. The tech giant is pulling further way from using Intel chips in Macs and the company surely isn't going to switch this Intel-replacement chip to an Intel foundry.

Takeaway

The key investor takeaway is that investing in Intel here is akin to catching a falling knife. The chip giant continues to face pressure with competitors taking market share in premium chips leaving the company focused on the low end where supply appears to exceed current demand.

The stock trades at ~12x current EPS that appear far too high. Intel remains a value trap until business prospects actually turn around.

Comments