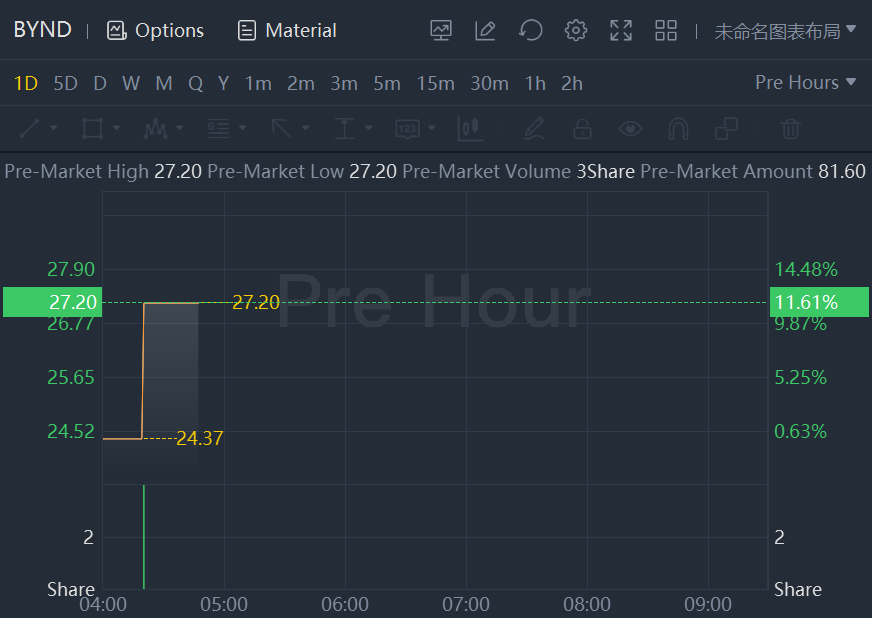

Beyond Meat shares jumped 11.6% in premarket trading.

Beyond Meat: Might Find A Bottom Soon

Summary

- The massive sell-off created a tempting entry point opportunity for risk-seeking investors. Despite the drop, the risk for additional downside remains but BYND might find its bottom soon.

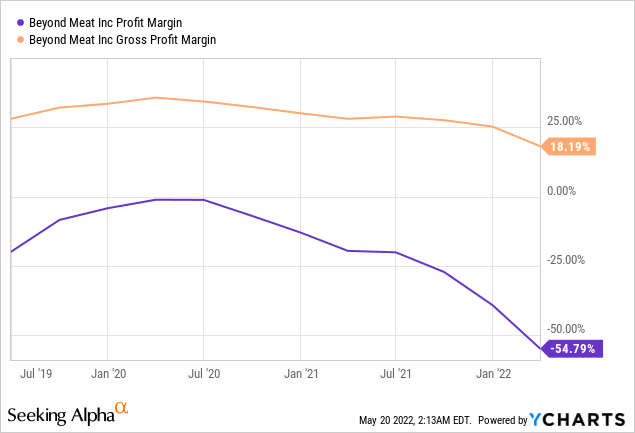

- The company has neither an economic moat nor a durable competitive advantage supported by its declining profit margins.

- The following quarters are critical for BYND and will clarify its future trajectory.

Investment Thesis

While the market remains pessimistic following the first-quarter results, the plunge in Beyond Meat, Inc. (NASDAQ:BYND) stock has incorporated into the stock price the relevant risks to a large extent. The massive sell-off createda tempting entry point opportunity for risk-seeking investors that can stomach additional downside risk. Despite the relatively low price of the stock compared to its all-time high levels, BYND needs to deliver meaningful results in the following quarters to qualify for a buy rating.

The Company's Fundamentals

Beyond Meat has a leadership position in the fast-growing plant-based meat (PBM) or the alternative meat industry. The company produces PBM products, enabling customers "to experience the taste, texture, and other sensory attributes of popular animal-based meat products while enjoying the nutritional and environmental benefits of eating" such products. Over the past decade, Beyond Meat has successfully innovated and added new products to its portfolio.

While Beyond Burger remains the company's flagship product and a major source of its revenues, it now has multiple products, including Beyond Sausage, Beyond Meatballs, Beyond Breakfast Sausages, Beyond Beef Crumbles, and Beyond Chicken Tenders. As of March 2022, the company's products were available in more than 135,000 retail and foodservice outlets in over 90 countries.

Q1's Results Were Disappointing

The company announced its Q1-2022 results on 11th May 2022, reporting revenues and gross margins below the industry's expectations. Beyond Meat's net revenues for the first quarter stood at $109.5 million compared to the industry expectations of $112.3 million. Although falling short of the industry's expectations, the revenues moderately increased by $1.3 million, up 1.2% YoY from Q1-2021. Despite the muted sales growth, the volume growth was up by 12%.

While commenting on the results, the management noted an increase in volume sold during the quarter, which was partially offset by lower net price per pound resulting from increased trade discounts. In addition, to a lesser extent, changes in product sales mix and foreign exchange rates have also negatively affected the net revenue figure.

As a result, the company's gross profit took a severe hit during the previous quarter and was reported at 0.2% compared to 30.2% in Q1-2021. In a statement, CEO Ethan Brown said that the company saw a "sizable though temporary" hit to its gross margin to support strategic launches, namely that of its plant-based jerky through its joint venture with PepsiCo (PEP). Despite the declining trend in profit margins, as the company scales and brings more production in-house, profits margins will meaningfully expand in the medium term. Undoubtedly, the recent quarters have proved that the company has no durable competitive advantage over its peers.

Increasing Competition

The major competitor that Beyond Meat faces today exists in the form of Impossible Foods. While Impossible collects excellent reviews on the taste of its burger, there is an important distinction that separates Impossible from Beyond Meat. Impossible uses GMO (genetically modified organisms) in its product, while Beyond Meat is GMO-free. Not surprisingly, GMO foods are still not popularly accepted by the general public. A survey conducted by the International Food Information Council found that nearly half of the American public tends to avoid GMOs.

Moreover, due to its linkage with diseases, Europe banned GMOs, allowing BYND to gain greater market access than Impossible, which uses GMO ingredients. As a result, although there is immense competition in the market and several plant-based meat-producing companies have emerged in the recent past, Beyond Meat has the first-mover advantage. In addition, the company has formed strategic partnerships with well-known retail brands, which will enable the company to at least maintain its competitive position in the market.

Strategic Partnerships During Q1 2022

Beyond Meat formed partnerships with the leaders in the fast-food chain industry to take advantage of their retail chain as the demand for plant-based meat increases worldwide. Not surprisingly, during the first quarter, BYND announced partnerships with renowned brands like McDonald's (MCD), Pizza Hut, KFC, and PepsiCo.

As per the agreement with McDonald's Corporation, Beyond Meat became the preferred supplier of McDonald's for the patty in the restaurant's new plant-based burger, McPlant. McDonald's has already conducted market tests of McPlant in the US and added the product to menus across the UK, Ireland, and Austria. In addition, Pizza Hut included Beyond Meat as a permanent menu item across Canada. At the same time, KFC conducted a nationwide limited-time offering in the US, noting recently that its launch of Beyond Fried Chicken resulted in more media impressions than any other product launch in KFC's history. The company also launched a joint venture with PepsiCo and introduced three SKUs of Beyond Meat Jerky as part of the Planet Partnership. As a result, BYND, through its strategic partnerships, will gain additional global recognition and access to new markets.

Plant-Based Meat Expected CAGR Of 18.3%

The PBM industry is growing and presents a compelling future outlook as the awareness regarding the health benefits of a plant-based diet and social consciousness regarding the negative consequences of animal farming increases worldwide. According to a report by KBV research, The global market for plant-based meat is expected to reach $12.3 billion by 2027, suggesting a CAGR of 18.3%.

A paper published in Nature food stated that food production is responsible for 35% of all global emissions. The use of cows, pigs, and other animals for food and livestock feed is responsible for 57% of all food production emissions.Therefore, an increasing population and rising awareness among the masses on the carbon footprint of the traditional meat industry will serve as growth drivers for the plant-based meat industry as it promises fewer carbon emissions and a consumption style that doesn't weigh on the consciousness of people.

Beyond Meat embraces green initiatives as its products emit 90% fewer greenhouse gases and require 93% less land, 99% less water, and 46% less energy to produce than their meat equivalents. Finally, as Beyond Meat expands its product portfolio and matches the taste with animal-based meat, it sets the foundation for switching consumption behavior from consuming animal-based meat to the alternative PBM options.

The Untapped Huge Market In Asia

The PBM market has tremendous opportunities for growth in Asia, especially in China and India. The two countries inhabit around 35% of the world's population and therefore have a great demand for food products. A survey found significantly higher acceptance of clean and plant-based meat in India and China compared to the USA. China has minimal arable land and a large population to feed, so it has become the world's largest food importer. While India, with a largely vegetarian population, presents an excellent product-market fit for Beyond Meat. Beyond Meat has already expanded into China as the company opened its first production plant in China on April 7th, 2021. The facility's opening has opened up possibilities for the company to expand into the Chinese market in the future, which could significantly expand the company's global footprint.

Concluding Thoughts

The PBM industry still faces an uncertain future, and the demand for the products can fade away with changing trends or due to a perception of health risks associated with artificial meat. Moreover, the elevated prices of the company's products are also a big factor that can hamper future growth. The products offered by the company now might not be economically viable for everyone and currently attracts high-end customers for its premium and pricey products compared to primary raw animal meat.

The company faces a tough challenge to bring down its costs and make it financially viable for the consumers to purchase its products. Despite the disappointing Q1 results, BYND may find a bottom soon. I own BYND as part of my small model portfolio, and any unexpected drop below the $20 share price level might lead to a reassessment of the hold rating. Nevertheless, there is still a lot of progress to be made, and the following quarters will provide more clarity on BYND's future trajectory.

Comments