Summary

- SQQQ provides 3x inverse 1-day returns of the Nasdaq 100 Index.

- Levered ETFs provide positive convexity in the direction of the bet.

- Daily rebalancing of exposure causes value decay, especially in volatile markets.

Investors who are afraid of market volatility often turn to inverse exchange-traded funds ("ETFs") such as the Proshares UltraPro Short QQQ ETF (NASDAQ:SQQQ) to protect their portfolios.

In my opinion, investors should consider reducing their long exposures instead of seeking inverse ETFs as a hedge, especially for holding periods of longer than a few days due to the volatility "decay" from daily rebalancings.

Fund Overview

As the name suggests, the Proshares UltraPro Short QQQ ETF seeks daily returns that is -3x the return of the Nasdaq-100 Index. The fund achieves the -3x daily return target by entering into total return swaps with large banks that are reset nightly.

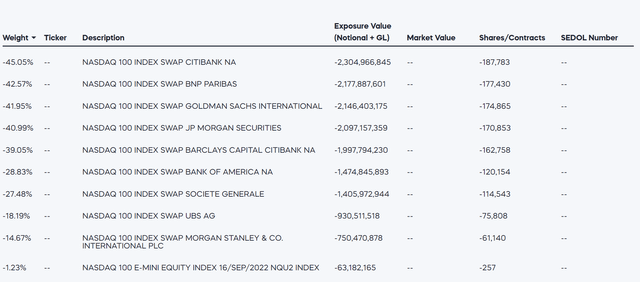

Figure 1 - SQQQ holdings (proshares.com)

Levered ETFs Only Work On Short Time Horizons

Investors who are interested in the SQQQ are highly encouraged to read this disclaimer from the Proshares website:

Due to thecompoundingof daily returns, holding periods of greater than one day can result in returns that are significantly different than the target return, and ProShares' returns over periods other than one day will likely differ in amount and possibly direction from the target return for the same period. These effects may be more pronounced in funds with larger or inverse multiples and in funds with volatile benchmarks.

What this means in layman terms is that the SQQQ is only designed to provide 3x inverse returns for one day. For any holding period longer than 1 day, the returns expectations will differ.

For example, imagine you start off with $100 invested in SQQQ. If the Nasdaq-100 index returns -5% on day 1, your position will grow to $115 (3 times the 1-day return of 5%). If the Nasdaq-100 returns -5% again on day 2, your position will grow to $132.25. The 2 day total is more than 3 times the 2-day compounded return of 10.25% or $130.75, because the two moves are in the same direction.

Conversely, if the returns were consecutive +5% on the Nasdaq-100 index, you would end up with $85 on day 1 and $72.25 on day 2, versus a 2-day compounded loss of 9.75%, or a $70.75 final balance assuming 3 times the returns.

Levered ETFs provide holders with "positive convexity"in the direction of their bet, i.e., with the SQQQ, as the Nasdaq-100 declines, the short exposure grows, and vice versa.

Levered ETFs Decay In Volatile Markets

The biggest problem with levered ETFs is that the daily rebalancing of the fund's exposure means that in volatile markets, the fund can lose value very quickly.

Going back to our example above, if the Nasdaq-100 returned +5% on day 1 followed by -5% on day 2, that should translate to a compounded 2-day loss of 0.25%, or theoretical ending balance of $99.25. However, what happens is that on day 1, the SQQQ balance will fall to $85 (3 times the 1-day return of -5%), and on day 2, the SQQQ balance will only grow to $97.75 (3 times the 1-day return of 5%). $1.50 in "value" will have been lost to volatility. The higher the volatility, the more the "decay."

Inverse ETFs Lose Value Over The Long-Term

Volatility coupled with the fact that markets are upwards trending in the long run means that inverse ETFs like the SQQQ are almost guaranteed to lose money over the long-term.

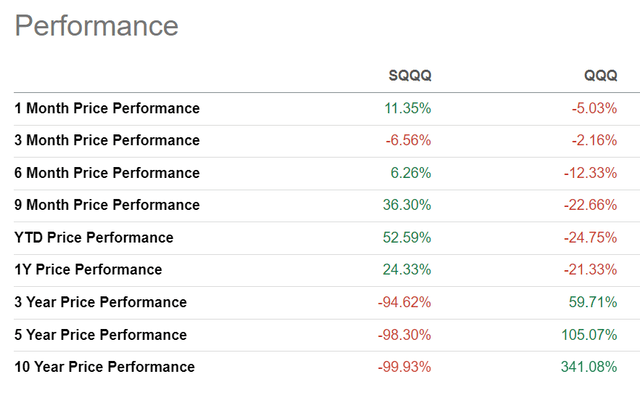

Comparing the performance of SQQQ vs. the Invesco QQQ ETF (QQQ) that tracks the Nasdaq-100 Index, we see that over any reasonably long time horizon, the SQQQ has been a money loser. Over 5 years, the SQQQ has lost $98.3 per $100 invested capital, and over 10 years, it has lost an incredible $99.93 per $100 invested capital.

Figure 2 - SQQQ vs. QQQ performance (Seeking Alpha)

Even YTD, while the QQQ has lost 24.75% of its value, the SQQQ has only gained 52.6%, far less than the theoretical 74.25% gain, because of the volatility decay mentioned above. On a 1 year basis, while the QQQ has lost 21.3%, SQQQ has only gained 24.3%.

Conclusion

If investors are truly concerned about their portfolios, they should consider reducing their long exposures instead of seeking inverse ETFs as a hedge, especially for holding periods of longer than a few days due to the volatility "decay" from daily rebalancing. Nimble traders can try to capitalize on the convex nature of levered ETF returns, but that is not an easy task, especially for novices.

Comments