Investors who are worried about the stock market declining, and who don’t mind limiting potential upside gains, can consider a new breed of exchange-traded funds called defined-outcome ETFs.

The funds, also called buffered ETFs, use options to mitigate losses in exchange for capping some gains, creating guard rails on an investor’s return. Since debuting about four years ago, assets in the funds totaled around $13.6 billion as of mid-July and took in $5.4 billion in 2022, according to Bloomberg data provided by Innovator ETFs.

The ETFs protect against a preset amount of losses. Most set loss protection at roughly the first 10%, 15%, or 30% of market downside, and are designed to be held for a full 12 months, although like all ETFs they can be bought or sold at any time.

For example, the Innovator U.S. Equity Power Buffer ETF–July (ticker: PJUL) protected against the first 15% of losses in the SPDR S&P 500 ETF (SPY) for the 12 months ended June 30, 2022. It lost only 0.8%, reflecting the fund’s expense ratio of 0.79%. During that time, the S&P ETF fell 11.87%.

A similar ETF, FT Cboe Vest U.S. Equity Buffer ETF–June (FJUN) from First Trust, protected investors against the first 10% of losses in the SPDR S&P 500 ETF during the 12 months ended June 17. It saw losses of 2.7% (including expenses of 0.85%), compared with the S&P’s loss of 11.8%.

Dave Alison, president of Prosperity Capital Advisors, who uses buffered ETFs as an bond alternative to create portfolio ballast, says these ETFs offered loss protection for clients when the Federal Reserve’s interest-rate hikes caused both stocks and bonds to fall. “They’ve done exactly what they should do in the portfolio,” he says.

There are 149 defined-outcome ETFs available. They follow major indexes, such as the S&P 500, the Nasdaq 100, or the MSCI EAFE. The five main issuers are Innovator ETFs, First Trust ETFs, Allianz, Pacer, and True Shares, with the first two having the vast majority of market share.

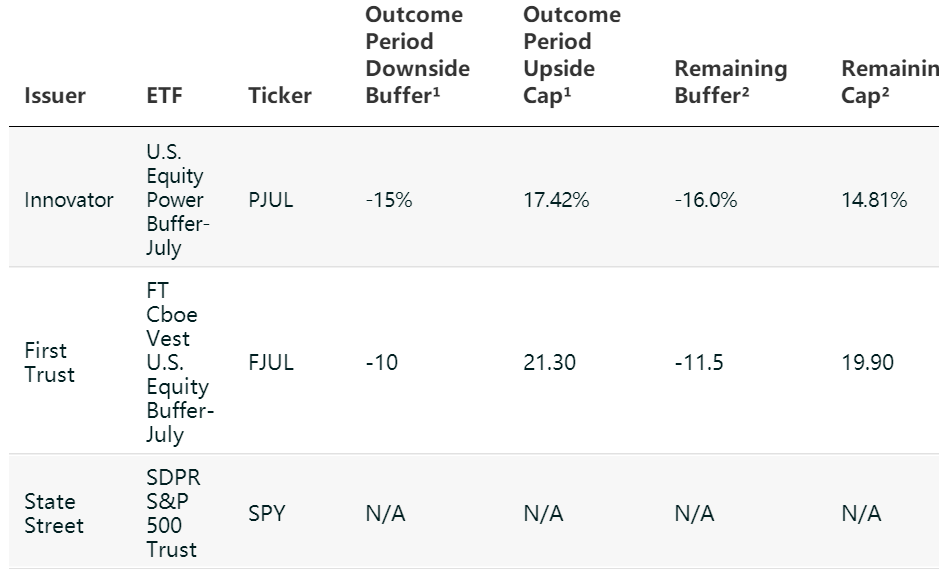

Guardrails for Your Portfolio

How two representative defined-outcome ETFs work.

While each issuer has its own methodology, they all use call and put options to establish the position and offset losses in the index they track. Because hedging is often expensive, the funds sell higher-priced calls to finance the trade. In return, gains are limited, and downside is defined. (Puts give holders the right, but not the obligation, to sell a stock at a set price at a set time, while calls give holders the right, but not the obligation, to buy.)

While the ETFs can be bought or sold at any time, to receive the advertised buffer and cap when the ETF resets, investors have to hold the fund through the full outcome period, which is typically one year from the day that the outcome period starts, says Bruce Bond, CEO of Innovator ETFs, which pioneered the strategy.

Once the ETF starts to trade, the daily return of the fund will change to reflect market movement and to keep the buffer and cap guardrails consistent. For example, for the period from July 1, 2022, to June 30, 2023, Innovator established the July U.S. Equity Power Buffer downside buffer at 15% and its upside cap at 17.42%, based on the price of the SPDR S&P 500 on July 1.

Three weeks into trading, as the S&P 500 rallied, the cap dwindled to 14.7% but the buffer expanded to 16.4%, to stay in line with the original outcome period value.

The fund’s return on July 21 was 2.2%, which is what investors would receive if they sold that day, while the S&P ETF’s return was 5.5%. There are two reasons for the return difference, Bond says: the expense ratio and the slight time lag that options have when keeping up with the reference asset.

There are simpler ways retail investors can try to protect themselves from equity market swings, such as low-volatility equity ETFs, says Aniket Ullal, head of ETF data and analytics at CFRA Research. While he’s a fan of defined-outcome strategies, he says it takes time to understand how they work.

Defined-outcome ETFs are similar to other risk-management products such as structured notes, which are securities issued by financial institutions linked to an underlying index or another benchmark. Daniel Milan, managing partner of Cornerstone Financial Services, who uses buffered ETFs and other structured products in his portfolio, says these ETFs give retail investors access to strategies long used by financial advisors and institutions in an easy-to-use vehicle. ETFs provide more flexibility, since they can be easily bought or sold and users benefit from ETFs’ inherent tax efficiency.

“Now they can go into their E*Trade account and type in a ticker symbol and buy it,” he says.

There are some caveats. The ETFs are significantly more expensive than the S&P 500 ETF or the Nasdaq-based Invesco QQQ ETF (QQQ), which annually cost 0.09% and 0.20%, respectively. Yet Hagen Pruemm, a financial advisor at SIS Financial Group, says if individual investors were to create these options trades on their own, it would be much more work, and much more costly. He uses these ETFs as a way to reduce volatility in equity portfolios.

The biggest caveat are the funds’ upside caps; in strong bull markets, such as 2021’s, they will underperform. That’s seen in the return of the Innovator U.S. Equity Buffer ETF–January (BJAN), which had an outcome period of Jan. 1, 2021 to Dec. 31, 2021. This fund had a 15% downside buffer and a 15% cap. Its return was 14%, net of fees, versus the S&P 500 ETF Trust’s 2021 return of 27%.

“The issue that really comes down to is, people say in this environment, ‘That’s fine, I’m willing to give up the upside.’ And then three years later, they’re like, ‘How come you got me into something that capped me?’ ” Milan says.

Comments