Summary

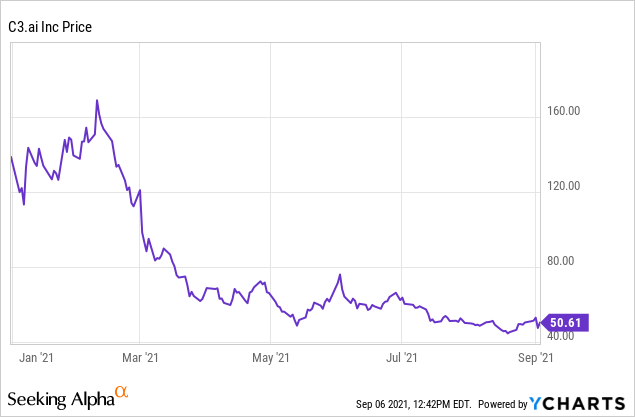

- C3.ai has lost 70% of its value relative to all-time highs near $170 that it notched immediately after its IPO.

- The stock's downfall is a reflection of only middling results, and its relatively tiny traction within its market.

- C3.ai's customer concentration, especially on Baker Hughes, still remains a consistent problem.

- Still, C3.ai is approaching a buyable valuation as it hits a mid-teens multiple of this year's revenue.

Sooner or later, the law of gravity comes for software stocks too: what comes up, must come down. Such was the case with C3.ai (AI), one of the hottest IPOs of the past year that immediately saw its stock price quadruple. C3.ai is an enterprise AI platform - that is, a technology base that lets its clients build and deploy artificial intelligence applications with preset tools. Investors had wide hopes for this company given the open-ended use cases this type of product can offer - but so far, C3.ai hasn't delivered the kind of growth rates that investors typically come to invest with these startup-like public equities.

C3.ai hit an all-time high of ~$170 this February, representing a quadrupling from its IPO price of $42. Since then, the stock has crumbled and given back ~70% of its value. In early September, the company released fiscal Q1 results, which were a cause for further disappointment in the stock that caused a further ~5% dip.

For now, the bearish thesis has won out

I had been bearish on C3.ai since its IPO. I've consistently called out a number of flaws with the company, including:

- Huge valuation for relatively normal growth rates.C3.ai, at its peaks, was trading at >40x forward revenue despite a ~30% y/y revenue growth rate - which is a massive valuation premium for what is considered a "normal" growth rate in enterprise software.

- Customer concentration.C3.ai only has a handful of customers, and its largest customer Baker Hughes, the oil services giant, is also a reseller of its product. Oil and gas companies overall represent about a third of its revenue.

- Massive losses.C3.ai loses nearly a dollar, in GAAP terms, for every dollar of revenue it generates.

The only reason investors clung onto this stock was for its thematic buzz (AI, needless to say, is one of the hottest areas in software) as well as their confidence in C3.ai's founder and CEO Tom Siebel, who founded and sold Siebel Systems to Oracle (ORCL) and has many deep-seated relationships in Silicon Valley.

But rest assured that a buy-the-dip opportunity may be emerging

Yet as my readers know, I'm a big believer in buy-the-dip. I prefer buying into companies when sentiment is weak and waiting for the rebound, rather than risking a purchase at market tops (this is especially true as the post-pandemic bull market continues to notch new, lofty highs with each trading day). In my view, the C3.ai slump is close to breaking.

Valuation is the key here, as C3.ai's correction has no longer left the company egregiously overvalued. At current share prices near $51, C3.ai has a market cap of $5.23 billion. After we net off the $1.10 billion of cash on C3.ai's balance sheet (for a company of this size, C3.ai's cash pile is quite enormous, which is one reason to be comfortable with this stock), the company's resultingenterprise value is $4.14 billion.

For the current fiscal year high ends in April 2022, meanwhile, C3.ai has guided to a revenue range of $243-$247 million, representing 33-35% y/y growth. It's going to need to stretch to get there: Q1 growth clocked in at only 29% y/y, but the company is guiding to acceleration in Q2 to 35-40% y/y growth.

Figure 1. C3.ai guidance update

If we take the midpoint of C3.ai's FY22 guidance range at face value, the company's valuation sits at16.9x EV/FY22 revenue.That's hardly a cheap multiple, but it's far cheaper than what C3.ai was trading at earlier this year.

The bottom line here: I'mupgrading my view on C3.ai to neutral,and putting the stock on my watch list. I'm interested in dipping my toes into this stock if it reaches a$41 price level,representing12.5x EV/FY22 revenue.Given the fierceness of C3.ai's recent correction, we may hit those levels within the month.

Q1 download

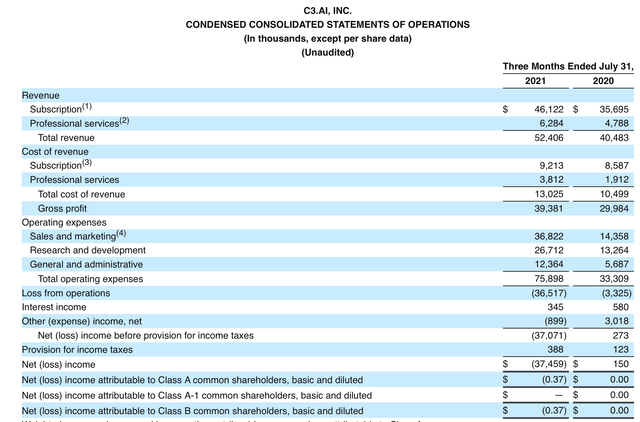

C3.ai's Q1 update wasn't perfect, but it wasn't all bad, either. Take a look at the earnings summary in the chart below:

Figure 2. C3.ai Q1 results

C3.ai grew its revenue at a 29% y/y clip to $52.4 million in revenue, which was only a minor beat versus Wall Street's expectations for $51.3 million (+27% y/y) in revenue. At the same time, C3.ai saw a minor acceleration as well from 26% y/y growth in Q4, which was a plus.

Here's some more good news: C3.ai's enterprise AI customer base hit 98 in the quarter, up 85% y/y. One of my biggest concerns with C3.ai is the fact that it still has only a fledgling customer base; at the time of its IPO, the company's ~50 customers could hardly be construed as a true enterprise software giant in the making. Yet C3.ai's clientele does skew large, and its progress in adding new customers is a promising sign.

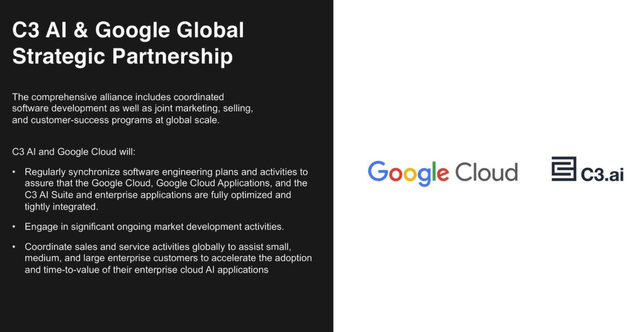

Another positive development: C3.ai has entered into both a product and go-to-market partnership with Google Cloud (GOOG). Building on top of an existing commercial agreement with Microsoft Azure (MSFT), this partnership will give C3.ai even more expansion potential into Google Cloud's universe of customers, as well as gain access to Google Cloud's sales force. The Azure partnership has yielded $200 million of closed business to date, with $350 million more in the pipeline: we hope the Google Cloud partnership can yield similar fruitful results.

Figure 3. C3.ai/Google Cloud partnership

Going forward, management expects C3.ai to lead with some smaller, lower-priced, and high-value products like C3.ai CRM. These purpose-built applications are more plug-and-play and give a chance for C3.ai to "land" more customers and seed the "expand" opportunity for later. Per CEO Tom Siebel's prepared remarks on the Q1 earnings call:

As we have previously discussed, historically, our business has been characterized by quarter-to-quarter lumpiness due to the substantial size of our average order value.

Now as application sales become an increasingly large part of our revenue mix, roughly 50% of our subscriptions last quarter in Q1 accrued from application software. We are increasingly offering lower priced, high-value products like C3 AI CRM and Ex Machina. And as we've discussed, we've been diversifying our distribution model to complement enterprise selling with telesales, distributors, market partners and direct marketplace selling."

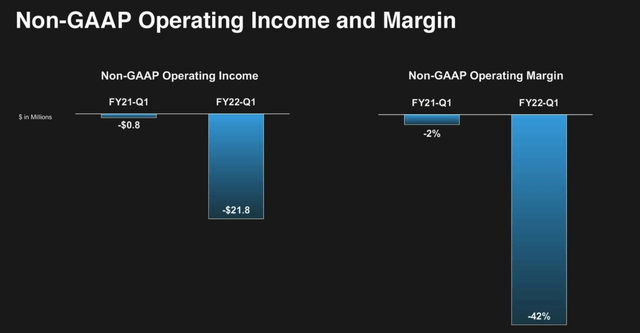

However, C3.ai's investments into sales and marketing have continued to burn holes through margins, which is a chief investor concern that has been a primary catalyst in dragging the share price down. Due to a massive increase in sales and marketing costs to 58% of revenue (25 points more than 33% in the year-ago Q2), C3.ai's pro forma operating margins hit a -42% mark in Q1, 40 points worse than the year-ago quarter. This was buffeted as well by a 12-point increase in R&D expense as a percentage of revenue and a 4-point increase in general and administrative expenses, and only partially offset by a three-point bump in pro forma gross margins.

Figure 4. C3.ai operating margin trends

Key takeaways

C3.ai remains a grab bag of pros and cons, in my mind. On the positive front, C3.ai possesses a broad technology base, and its recent go-to-market developments (leading with smaller products like CRM to bag more customers, and a new partnership with Google Cloud) are promising growth levers. At the same time, C3.ai's relatively limited market penetration and heavy losses are worrying.

At the right price, I'm a buyer. I'm waiting for a further ~20% dip in C3.ai to the low $40s before diving in, but this stock is now a firm watch list item for me.

Comments