Don’t call it a “pause.”

Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

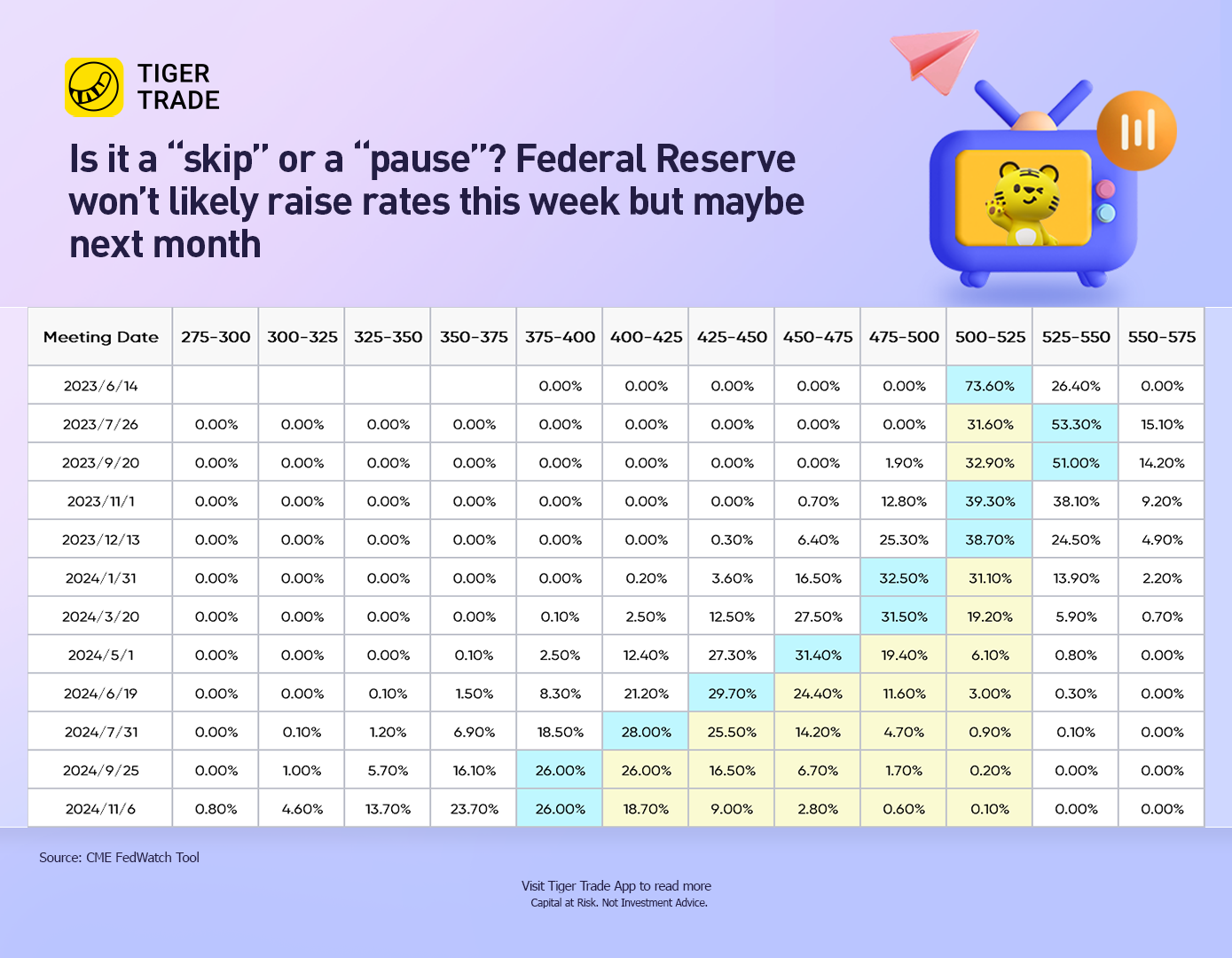

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

But what might otherwise be seen as a “pause” will likely be characterized instead as a “skip.” The difference? A “pause” might suggest that the Fed may not raise its benchmark rate again. A “skip” implies that it probably will — just not now.

The purpose of suspending its rate hikes is to give the Fed’s policymakers time to look around and assess how much higher borrowing rates are slowing inflation. Calling this week’s decision a “skip” is also a way for Chair Jerome Powell to forge a consensus among an increasingly fractious committee of Fed policymakers.

One group of Fed officials would like to pause their hikes and decide, over time, whether to increase rates any further.

But a second group worries that inflation is still too high and would prefer that the Fed continue hiking at least once or twice more — beginning this week.

A “skip” serves as compromise.

When the Fed chair speaks at a news conference this Wednesday, he will likely make clear that the central bank’s key rate — which has elevated the costs of mortgages, auto loans, credit card and business borrowing — may eventually go even higher.

The clearest signal that a skip, rather than a pause, is in the works will likely be seen in the quarterly economic projections that policymakers will issue Wednesday. Those may show that officials expect their key rate to rise a quarter-point by year’s end — to about 5.4%, above their estimate in March.

“That’s probably the only way to keep the committee cohesive in an environment where they have seem to have somewhat broadening disagreements,” said Matthew Luzzetti, chief U.S. economist at Deutsche Bank Securities.

For more than a year, the Fed’s 18-member rate-setting committee has presented a united front: The officials were nearly unanimous in their support for rapid rate hikes to throttle a burst of inflation that had leapt to the highest level in four decades. (The committee has 19 members at full strength; one spot is now vacant.)

The Fed raised its rate by a substantial 5 percentage points in 14 months — the fastest pace of increases in 40 years, to a 16-year high. The policymakers hope that the resulting tighter credit will slow spending, cool the economy and curb inflation.

The rate increases have led to sharply higher mortgage rates, which have contributed to a steep fall in home sales. The average rate on a 30-year mortgage has nearly doubled, from 3.8% in March 2022 to 6.8% now. Compared with a year ago, sales of existing homes have tumbled by nearly a quarter.

Credit card rates have also climbed higher — topping 20% on average nationwide, up from 16.3% before the Fed’s rate hikes began. Many consumers have had to bear the weight of that costlier cost credit card debt.

Auto loans have grown more expensive, too. The average rate on a five-year loan has jumped from 4.5% early last year to 7.5% in the first three months of this year.

Several Fed officials contend that rates are already high enough to slow hiring and growth and that if they go much higher, they could cause a deep recession. This concern has left policymakers deeply divided about their next steps.

The camp that’s leaning against another rate increase is considered “dovish,” in Fed parlance. The doves, who include Powell and other top officials, think it takes a year or more for rate hikes to deliver their full effect and that the Fed should stop hiking, at least temporarily, to evaluate the impact so far.

The more dovish officials also worry that this spring’s banking turmoil, with three large banks collapsing in two months, might have compounded the brake on economic growth by causing other banks to restrict lending. Raising rates again too soon, they feel, could excessively weaken the economy.

The doves also think that pausing rate hikes to ensure that the Fed doesn’t go too far might help achieve the tantalizing prospect of a “soft landing.” This is the hoped-for scenario in which the Fed would manage to tame inflation without causing a recession, or at least not a very deep one.

“Maybe the majority of the tightening impact of what the Fed already did is still to come,” Austan Goolsbee, president of the Federal Reserve Bank of Chicago, said last month. “And then you add the bank stresses on top of it. ... We have got to take that into account.”

Another group expresses a more “hawkish” view, meaning it favors further rate increases. Although food and gas prices have come down, overall inflation remains chronically high, hiring remains hot and consumers are still stepping up their spending — trends that could keep prices high.

And some of the reasons Fed officials had previously cited in support of a pause no longer pose a threat. Congress, for example, approved a suspension of the federal debt ceiling, thereby avoiding a U.S. default that could have caused a global economic meltdown.

“I don’t really see a compelling reason to pause — meaning wait until you get more evidence to decide what to do,” Loretta Mester, president of the Cleveland Fed, said last month in an interview with the Financial Times. “I would see more of a compelling case for bringing (rates) up.”

For now, the doves appear to have the upper hand. Powell signaled his support for a pause in carefully prepared remarks May 19.

“Given how far we’ve come, we can afford to look at the data and the evolving outlook and make careful assessments,” Powell said, referring to the Fed’s streak of rate hikes.

More recently, Philip Jefferson, whom President Joe Biden has nominated to serve as vice chair of the Fed, also expressed support for a pause in rate hikes while making clear that it was likely to be a skip.

“A decision to hold our rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle,” Jefferson said in a speech. “Skipping a rate hike at a coming meeting would allow (the Fed’s policymakers) to see more data before making decisions” about interest rates.

In March, seven Fed officials indicated that they preferred to raise the Fed’s key rate to about 5.4% or higher by the end of 2023. If three more policymakers were to raise their projections this week to that level, that would be enough to boost the median estimate a quarter-point above where it is now.

If only two officials raise their forecasts for rate hikes, it would leave the committee evenly split over whether to hike again later this year. This could create a more muddled message about what comes next.

Still, any skip in rate hikes might not last long. There won’t be much major economic data released between this week’s Fed meeting and the next one in July — just one more jobs report and one more inflation report.

As a result, inflation will likely still remain high, according to the most recent data, when the Fed meets in July, with hiring still strong. The hawks may well prevail at that session and win another rate hike.

A report on inflation in May will be issued on Tuesday, the first day of the Fed’s two-day meeting. But most economists think the officials will largely have their rate decision in mind by then. So the inflation report for May will likely have more influence on what happens at the following Fed meeting in July.

Comments