Summary

- As Grab-AGC merger draws near, new insights derived from auditors and SEC's increased scrutiny of SPACs drastically changed our bullish thesis established 5 months ago.

- Grab's top line and bottom line improved in 2021Q1 as a result of increased GMV per user. However, decline in monthly users suggests that growth momentum at risk due to competitions.

- Although competitions are rising, Grab stated at the regions' market penetration stands at only 11%, offering Grab and competitions plenty of headroom to grow.

- Material changes of our thesis sterns from Grab's valuations based on the revised figures in accordance to IFRS. This offers investors little investment value proposition compared to UBER and DIDI.

- 13F filings suggest Grab's valuations did not deter institutional investors. Perhaps AGC's $10 NAV offers investors enough of a safety net to maintain positions.

Introduction

It's about time to update our investment thesis since we last established it 5 months ago. Many new insights have surfaced, some good, some bad. If you're new to this company, it is highly recommended to read our thesis published here and here. In this article, we're going to examine the following topics:

- Latest merger updates and officially numbers

- Latest business segments performance in 2021Q2

- Prospects vs. Rising Competition

- Value

1. Merger Updates and Official Numbers

Grab's merger with Altimeter Growth Corp (AGC) is expected to be completed by the end of 2021. We're finally given an update after months of waiting. According to Nikkei Asia, it is implied that Grab's merger was expected to be completed by 2021Q2 but was delayed due to auditing U.S. Securities and Exchange Commission's (SEC) tightened scrutiny of SPACs. If you're doubtful about Grab's interest to go public, remember that the 2 main pieces of evidence are the contracted agreement with Uber (NYSE:UBER) to go public before 2023 and to meet the ambitions of 2 million daily bookings.

During this process, we finally have Grab's official numbers. Grab clarified several issues with the auditors and the SEC. Perhaps investors would be most concerned about its revised FY20 revenue to $0.469bn from $1.2bn (61% reduction). The revision saw several operating expenses being labeled as contra revenue items instead.

The bad news is, this 61% in reduction has a huge impact on our thesis. Since Grab is not profitable, we had to observe the growth of its sales. Before the official numbers are released, we pulled information from sources and estimated that Grab's sales in FY2020 would be around $1.87bn to $3.91bn. It's a far cry from our estimation. We'll discuss more of this in the valuation section.

The good news is, this delay turned out to be a blessing in disguise. AGC's $10 net asset value (NAV) saved investors (including us) from a worse drawdown (below $10) since the market crash in Feb. However, the days of this safety net are numbered as Grab's merger is around the corner.

Other factors should also be considered, such as AGC shareholders' approval of the merger.

2. Latest business segments performances in 2021Q2

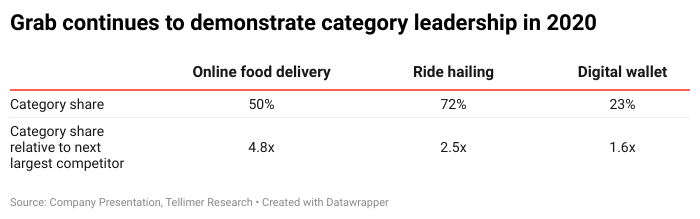

Grab is Southeast Asia's (SEA) super-app that dabbles in many business segments, including ride-hailing, food delivery, shipping, digital banking, insurance, and investments. Even though Grab dabbles in diverse business segments, Grab has established itself as a convincing market leader in several segments. Figure 1 illustrates that.

Detailed 2021Q1 quarterly performance can be found directly from Grab's websitehere. Here's a summary of Grab's performance in each segment.

- Ride-hailing: Although activity level (measured in Gross Merchandise Value or GMV) is only at 68% of 2020Q1 due to ongoing travel restrictions in SEA, revenue and EBITDA increased 18% and 42% to $145mill and $115mil, respectively.

- Deliveries: This segment is probably Grab's best performing business segment during the pandemic. This has helped compensate for losses from Grab's ride-hailing business. Food delivery activities (GMV) increased 49% from 2020Q1 to $1.7bil. Adjusted Net Sales increase 96% YoY, and revenue (Adjusted Net Sales minus incentives) turn positive. GMV of GrabMart, Grab's new product in this segment, increased 36x from YoY. However, GrabMart's actual contribution to Food Deliveries' growth is unknown. Shipping is also unknown.

- Financial Service: This segment also showed strong growth. Grab's overall financial service total payment volume increased 18% YoY while Adjusted Net Sales increased 31% YoY. Revenue (Adjusted Net Sales minus incentives) also turn positive. Grab stated that loan disbursals and insurance offerings showed strong growth, but no concrete breakdown was given.

* Adjusted Net Sales = Revenue + consumer incentives and excess driver/merchant incentives

Figure 1

Figure 2

3. Prospects and Rising Competition

With such strong growth demonstrated by Grab, investors must ponder the question, "How sustainable is this growth"?

The answer is rather simple: "How big is the total addressable market?"

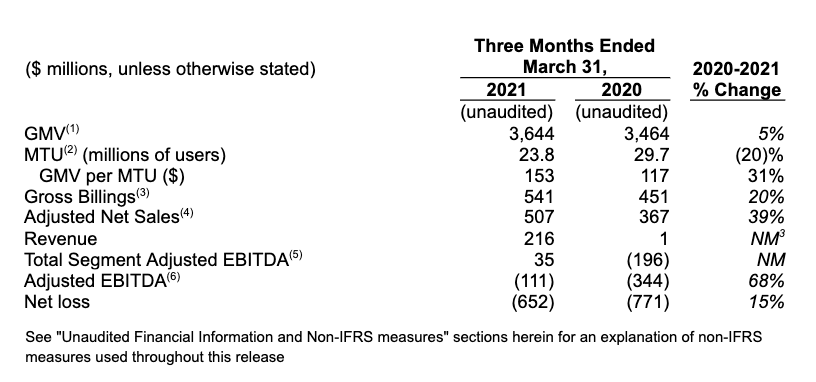

Since Grab's food delivery segment has become Grab's primary source of revenue and has helped narrow Grab's total losses from $771mil to $652mil (Figure 2), Grab's food delivery segment is a reliable proxy to Grab's overall performance.

Demi Yu, regional head of deliveries at Grab, gave very encouraging guidance toward's Grab's growth in the food delivery segment. Shesaidthat SEA's food delivery market penetration is only at 11% compared to around 20% in China and the US. This implies that around 89% of the food delivery market remains untapped. This is a 10x potential growth for Grab assuming Grab is able to maintain market share. This is the tricky part.

Although Grab's overall performance in $ is impressive, one red flag was the decrease in monthly transacting users (MTU). Although the GMV per user increased 30% YoY, Grab's MTU dropped 20% YoY.

There are 2 takeaways: (1) Grab is losing users to competition, (2) Grab is establishing a network effect where retained users are using the platform more. Since takeaway (2) is good, let's focus more on rising competition's downside risk.

A new strong contender has entered the arena, AirAsia. No one will blame you take AirAsia as an airline business. However, AirAsia is now repositioning itself as a data-driven technology company. AirAsia chief executive officer Tan Sri Tony Fernandes said that:

People are too focused on our airline business, but AirAsia is now a multi-business company and a very valuable data-driven technology company with a strong brand

This is very true, as evident from AirAsia's latest string of acquisitions. The company recently acquired a Malaysian online food delivery platform DeliverEat and Gojek’s operation in Thailand for $50mil to strengthen the company's logistics chain and e-commerce presence. Not to mention, These business segments will form a very synergistic relationship with AirAsia's airline and hotel business operations.

Therefore, the key takeaway for Grab's "prospect vs. competition" debate is that competition is not a major concern at this stage as market penetration is still low, and there is still a lot of headroom to grow for players in this space.

4. Valuation

Here is where our thesis changed the most. The material changes in our thesis are derived from Grab's accounting changes. The accounting changes come from Net Adjusted Sales vs. Revenue where

Adjusted Net Sales = Revenue + consumer incentives and excess driver/merchant incentives

The easier way to understand adjusted net sales is Tesla's (TSLA) revenue from the carbon tax credit. It is still contributing to Tesla's revenue, but it is not from Tesla's operation and is not guaranteed to recur.

Our past valuations were unknowingly based on Net Adjusted Sales, making it more comparable to the likes of Uber. However, this changes if incentives are not considered. By removing incentives from Grab's adjusted net sales, Grab's valuation will deter investors, especially when Uber or DiDi (DIDI) currently present investors with much better valuation after a recent decline in share price.

Grab's current annualized revenue for FY21 is $864mil (= $216mil x 4). Given AGC's share price of $10.64, Grab is currently valued at a 49 Price-to-Sales(NASDAQ:PS)ratio. For comparison sake, Uber and DiDi's PS ratios are 6.22 and 1.77. Moreover, DiDi managed to reach profitability in 2021Q1 for the first time despite China's crackdown on Chinese tech companies.

DiDi's share price decline has also negatively impacted Uber as Uber is DiDi's second-largest shareholder (12% ownership) behind Softbank(OTCPK:SFTBY). Similarly, Grab's decline in share price will also negatively impact Uber, as Uber owns about 27.5% of Grab.

Investors might sneer at Grab due to its high valuations. However, some analysts are rather bullish towards Grab.Telimer gave AGC a target of $16.50, which puts Grab at $66bil or a PS Ratio of 76.4. Moreover,institutions are accumulating in 2021Q2 when SPACs (including AGC) were hit hard by inflation fears.

However, at this time (before the merger), since AGC offers a floor of $10 while AGC is currently trading near the floor of $10, this provides investors a safety to capitalize on Grab's growth with minimal downside.

5. Conclusions

We had established our bullish thesis 5 months ago due to its impressive reported growth in sales. However, Grab's recent audited numbers reported a rather less impressive top line when incentives are not considered. Grab's valuation based on the revised figures in accordance with IFRS offers investors little investment value proposition.

Rising competition is putting Grab's continuous strong growth momentum at risk. This is evident from Grab's decrease in monthly transacting users. Although market penetration is only at 11% and with plenty of headroom to grow, one might wonder whether this potential has already been priced in based on Grab's current valuations in accordance with IFRS.

As the old saying goes, "never overpay for growth." Nevertheless, despite Grab's high valuation, 13F filings suggest institutional investors are undeterred from investing in Grab via AGC.

We'll be maintaining our positions on Grab, simply due to its safety net offered by AGC's $10 floor.

Comments