Though Intel already revised its full-year 2022 view by about $10 billion during 2Q, the company could lower its 4Q view further amid waning PC demand.

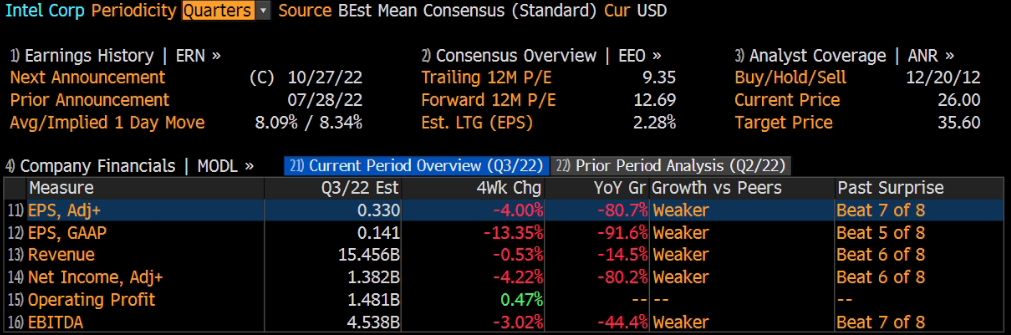

Intel Corporation will report third-quarter 2022 financial results on Thursday, Oct. 27, 2022. The chip giant is expected that revenue is $15.456 billion, adjusted net income is $1.382 billion, and adjusted EPS is $0.33, according to Bloomberg's consensus expectation.

Last Quarter Review

Intel last posted its quarterly earnings data on Thursday, July 28th. The chip maker reported $0.29 earnings per share for the quarter, missing the consensus estimate of $0.69 by ($0.40). The company had revenue of $15.30 billion for the quarter, compared to analysts' expectations of $17.93 billion. Intel had a net margin of 26.03% and a return on equity of 16.65%. The business's quarterly revenue was down 17.3% compared to the same quarter last year. During the same quarter last year, the business posted $1.28 EPS. On average, analysts expect Intel to post $2 EPS for the current fiscal year and $2 EPS for the next fiscal year.

Current Period Overview

Though Intel already revised its full-year 2022 view by about $10 billion during 2Q, the company could lower its 4Q view further amid waning PC demand, which was reflected in AMD's negative pre-announcement. Sales might be down sequentially for Intel's Client computing and Datacenter segments, which could further pressure gross margin to drop below consensus' 46% in 3Q. Despite some help from the recently passed CHIPs Act in the US, Intel might pare back its own costs and capital-spending spending amid unit slowdowns in PCs and servers.

Intel's limited traction with hyperscale cloud customers continues to hurt prospects in its high-margin Datacenter segment, where it's lost share to AMD and Nvidia. Intel's IFS segment may remain a drag on gross margin and could see underutilization charges.

Gartner PC Shipment Report and AMD’S Pre-Release Are Red Flags

Gartner, a consulting firm, recently reported a 19.5% decline in third-quarter worldwide PC shipments, with all major vendors seeing a significant drop in shipments. Gartner’s research revealed the steepest drop in PC shipment volume since the 1990s which is when the company began tracking such data. The deceleration of growth in the PC market indicates big trouble for Intel’s Client Computing Group which sells the chip maker’s processors and other PC components. The Client Computing Group generates about half of the company’s revenues. In the second-quarter, also according to Gartner, worldwide PC shipments declined 12.6% year over year, so the decline in the PC market actually gained significant momentum in the third-quarter.

Related to the massive decline in PC shipments in the third-quarter, Intel’s rival AMD also issued a profit warning that showed a sharp down-turn in its Client business. AMD’s Client segment generates revenues from the sale of Ryzen desktop and laptop processors.

Based off of Intel’s last guidance in Q2’22, the company expects FY 2022 revenues of $65-68B, but given most recent shipment data for the PC market, Intel may be forced to further cut its top line outlook for the current fiscal year.

Intel may not be able to meet low EPS expectations

Intel and AMD are both dependent on the number of PC and laptop shipments, so the accelerating down-turn in the third-quarter is set to be a big problem for Intel… especially because Intel’s CEO said in Q2’22 that the third-quarter would be the “bottom”. Since the market’s down-turn accelerated in Q3’22, I am not sure Intel’s CEO will still be able to defend this statement later this month.

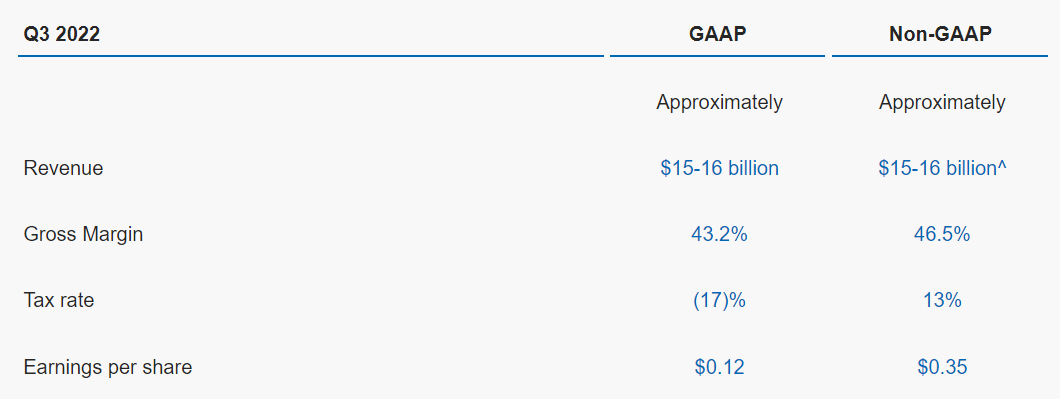

As a result, Intel’s third-quarter performance could even under-perform low EPS expectations. For Q3’22, the company expects revenues of $15-16B and and EPS of $0.35.

Analyst views

Bloomberg data shows a consensus of (12) analyst ratings at ‘buy’ for Intel. A mean of estimates suggests a long-term share price target of $35.6 for the company. The current share price trades at a 37% discount to this assumed long term fair value (as of the 19th of October 2022). While Since October this year, we have seen some analysts successively lowered Intel's target price.

Deutsche Bank analyst Ross Seymore lowered the firm's price target on Intel to $32 from $35 and keeps a Hold rating on the shares. Fears of fundamental deterioration are "leading to very bearish investor positioning" into the Q3 results for semiconductors, Seymore tells investors in a research note. Fundamentally, the analyst expects Q3 earnings season to "yield more pervasive signs of weakness" and for the second consecutive quarter, he sees downside risk to 2023 estimates. As for the semiconductor stocks, Seymore is becoming "incrementally more constructive," saying the drop in the sector and relative underperformance verses the S&P 500 "have clearly priced in significant rev/EPS estimate cuts" and left the group valuation 20% below the its 5-year average.

Barclays analyst Blayne Curtis lowered the firm's price target on Intel to $30 from $35 and keeps an Underweight rating on the shares. September notebook volumes were slightly worse but the outlook for Q4 "moves much lower," Curtis tells investors in a research note. The analyst says the PC market looks to be nearing a bottom with 2022 close to pre-pandemic levels.

Needham analyst N. Quinn Bolton lowered the firm's price target on Intel to $32 from $40 and keeps a Buy rating on the shares as part of a broader research note on Semiconductors & Semiconductor Equipment. Industry conditions deteriorated further in September, with reduced demand spreading across most end-markets like analog, industrial, automotive, and data center, but with semiconductor valuation multiples at multi-year lows, stock prices in the group are more likely to be driven by changes in earnings estimates in the near-term, the analyst tells investors in a research note.

Wells Fargo analyst Aaron Rakers lowered the firm's price target on Intel to $32 from $45 and keeps an Equal Weight rating on the shares. The analyst thinks increasing concern over year-over-year data center revenue declines in 2023 will persistently weigh on shares.

The biggest risk for Intel is a continual slowdown in the CCG business and, related to this, a sequential cut to the company’s FY 2022 guidance. Besides these two big risk factors, investors must brace themselves for a decline in gross margins in the third-quarter as well as weaker volume shipments likely affected product pricing in a big (and negative) way.

Given that Intel shares have fallen about 50% so far this year, It’s Q3’22 earnings sheet could be yet another catalyst for a direction selection revaluation. Should you be greedy or fearful?

Comments