Investment Thesis

Apple (NASDAQ:AAPL) designs, manufactures, and distributes smartphones, personal computers, wearables, and related services. Apple has been one of the most valuable companies in the world for a while and has leadership positions in numerous fields. Its massive installed device base (1.8B active devices) is pushing Apple's service revenue upwards at a rapid pace, and the overall company's profit margin is also improving. Furthermore, Apple is moving to become self-sufficient to reduce costs and mitigate supply chain disruptions, and the effort has been paying off. I expect Apple to continue its success well into the future, and the current volatility in the tech sector is presenting a huge opportunity to grab Apple shares at a discount because:

- Apple's high margin businesses (Mac and Service segments) are growing at a rapid pace, contributing to great revenue growth and margin expansion.

- Revenue growth trajectory remains solid with an increasing subscription base and new product releases (iPad Air, iPhone SE, and etc.).

- The market volatility and tech sector sell-off dragged Apple's stock down, and it is now being sold under its pre-pandemic level. This presents a great opportunity.

Growing in Right Segments

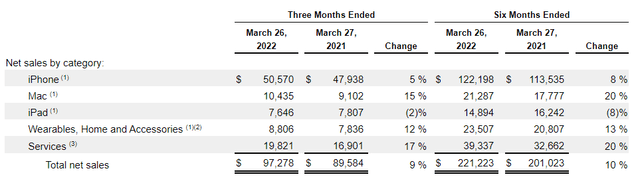

Since I wrote my last article, Apple reported quarterly earnings in late April, and the results continue to demonstrate that Apple is focusing on the correct segments for growth and profitability. Overall revenue grew 9% YoY to $97.3 B, and they generated a whopping $28 B operating cash flow. Particularly, their Mac segment and services segment led the charge.

Apple has been working on becoming self-sufficient and manufacturing key product components internally. A couple of years ago Apple took the noteworthy action of severing ties with Intel and making their own computer chips. The effort has been paying a great dividend. The Apple M1 (their own chip) has been performing very well against Intel and other chips on the market, and Mac sales have been very strong. Additionally, producing their own chips boosted the profit margins on Mac products.

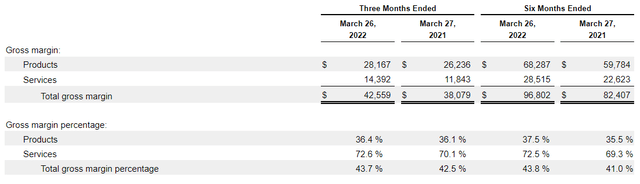

Strong performance by Apple Services segment (advertising, AppleCare, Cloud, Digital Content, Payment) is also welcome news for investors. The services segment is a 2x higher gross margin business (72.6%) than the products segment (36.4%), and it has higher growth potential from cloud and digital content. Assisted by its massive installed device base (1.8 B active devices), AppleCare has great potential for increasing revenue as well. Overall, the strong performance from Mac and Services shows that there are good days ahead.

Performance by Segments (SEC Filings)

Gross Margins of Apple by Segments (SEC Filings)

Strong Revenue Growth Trajectory

Apple has been growing at a solid pace (10% per year, 5-year average) in the past several years, and the revenue growth is accelerating. This acceleration is due to multiple factors. The first one is the continuing strong performance from new products, and there is no sign that this trend is going to end. During the last quarter, Apple released iPhone SE with 5 G technology, iPad Air with M1 chip, all-new Mac Studio, and all-new Apple Studio Display.

As mentioned before, Apple currently has 1.8 B active device bases, and the number is expected to grow with the release of new products. The active base has been growing at about 100-150 million per year (1.4 B, 1.5 B, 1.65 B, and 1.8 B in 2019, 2020, 2021, and 2022, respectively). Also, this larger installed base will translate into greater revenue growth from AppleCare, advertising, and cloud services. Currently, Apple has about 785 M subscribers to these services.

Favorable Valuation Thanks to Volatility

Ongoing volatility caused by supply chain disruption, inflation, war, and Federal Reserve's changing policies dragged the whole tech sector severely down. Nasdaq index is down from 16,000 in November 2021 to below 12,000. This volatility dragged great companies like Apple along, and now Apple stock is trading below its pre-pandemic level (current P/E ratio of 23.8x vs. pre-pandemic P/E around 25.5x). This presents a great opportunity for investors to grab Apple shares at a bargain.

Nasdaq Index (CNBC)

Intrinsic Value Estimation

I used DCF model to estimate the intrinsic value of Apple. For the estimation, I utilized current EBITDA ($130 B) as a proxy for cash flow and WACC of 9.0% as the discount rate. For the base case, I assumed EBITDA growth of 20% (Sector median) for the next 5 years and zero growth afterwards (zero terminal growth). For the bullish and very bullish case, I assumed EBITDA growth of 22% and 24%, respectively, for the next 5 years and zero growth afterwards.

The estimation revealed that the current stock price presents 20-30% upside. Given their technological superiority, organic/inorganic growth, and market dominance, I expect them to achieve this upside with ease.

Price Target | Upside | |

Base Case | $170.23 | 16% |

Bullish Case | $182.92 | 24% |

Very Bullish Case | $196.41 | 34% |

The assumptions and data used for the price target estimation are summarized below:

- WACC: 9.0%

- EBITDA Growth Rate: 20% (Base Case), 22% (Bullish Case), 24% (Very Bullish Case)

- Current EBITDA: $130 B

- Current Stock Price: $147.11 (05/14/2022)

- Tax rate: 20%

Cappuccino Stock Rating

The details of the metric is explained in this article.

| Weighting | AAPL | |

| Economic Moat Strength | 30% | 5 |

| Financial Strength | 30% | 4 |

| Growth Rate vs. Sector | 15% | 3 |

| Margin of Safety | 15% | 5 |

| Sector Outlook | 10% | 4 |

| Overall | 4.3 |

Economic Moat Strength - 5/5

Apple gets 5 out of 5. Apple is a clear leader with exceptional competitive edge. Their competitive edge stems from technological superiority, switching costs, and network effects.

Financial Strength - 4/5

Apple has $51.5 B in cash and a high covered ratio (45.13x), but their liquidity (current ratio at 0.93x and quick ratio of 0.76x) is in line with the sector.

Growth Rate - 3/5

Apple is growing at a pace consistent with their overall industry. Apple’s most recent annual revenue growth was 18.63% (vs. sector median of 19.98%). Given their leadership position and strong revenue, these revenue growth numbers are great. However, compared to hyper growth companies in the start-up or ramping-up phase with 50-60% growth rates, it’s hard to give out 4 or 5 stars.

Margin of Safety - 5/5

Apple is trading ~25% under intrinsic value at this point. The ongoing market volatility and tech sector struggles are providing a great opportunity to grab Apple’s shares under intrinsic value. Their P/E ratio is below pre-pandemic level, which just doesn't make sense.

Sector Outlook - 4/5

The tech sector will keep on growing at a rapid pace with new technology and markets, but the smartphone and laptop segments won’t be the fastest growing segment in tech. There will be adequate, but not exceptional, growth.

Risk

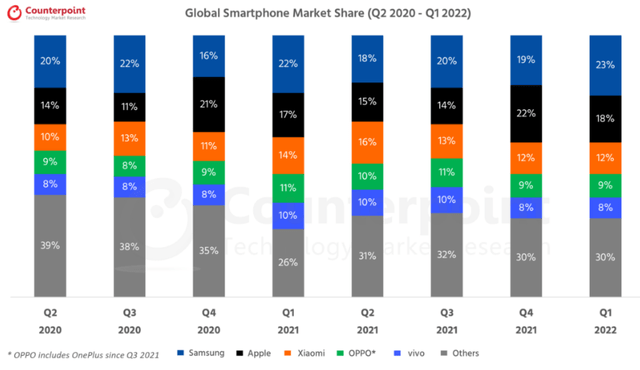

Apple's main segment is still the iPhone, and competition within the smartphone market is only increasing and getting complex. Also, consumer preference is diversifying in terms of preferred features (camera quality, computing/memory performance, weight/size, etc.). The iPhone family still commands a leadership position based on technological superiority, switching cost, and brand image, so I don't expect Apple to struggle. However, I wouldn't expect large growth from the iPhone segment in the future.

Global Smartphone Market Share (Counterpoint)

As mentioned before, Apple has been moving towards self-sufficiency by manufacturing their own parts. So far, the effort has impacted the business in a positive way by improving margins and mitigating supply chain disruption. However, relying on their own parts can result in isolation, lower technological development, and less market penetration. One example is the Japanese cellphone makers (Panasonic, Sharp, or NEC). They were way ahead in terms of innovation, but they failed to achieve global success. This is an extreme case, and I don't expect this will be the problem for Apple. However, investors should monitor whether Apple is maintaining its cutting-edge technology as they transition towards being more self-sufficient.

Conclusion

Apple has been an outstanding investment for a couple of decades at this point. Their technological superiority, brand image, and switching cost provide a great economic moat, and new products and services will keep their growth engine running. Based on their strong financials and market leading position, I expect Apple to excel in the foreseeable future. I expect 20-30% upside.

Comments