Palantir (NYSE:PLTR) stock trades at a fraction of its price just one year ago, in spite of sustaining impressive growth amidst a difficult economic environment. This is the kind of stock that one should hold for very long time periods and add during times of weakness, like now. While the company is still not yet profitable on a GAAP basis, it is generating ample free cash flow and has a cash-rich balance sheet. I rate the stock a strong buy as one of the more compelling opportunities in the tech sector. PLTR is a core holding in the Best of Breed portfolio and one I intend to hold over the long term.

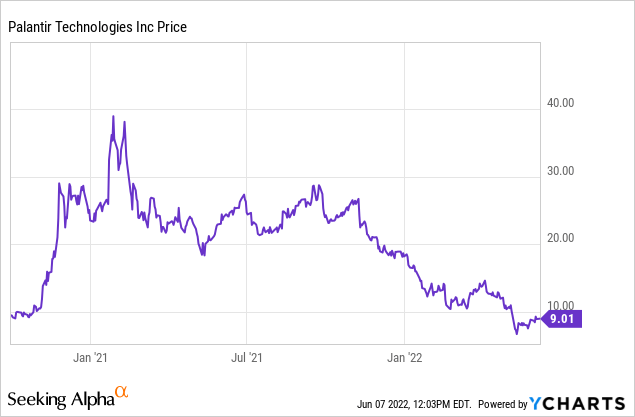

PLTR Stock Price

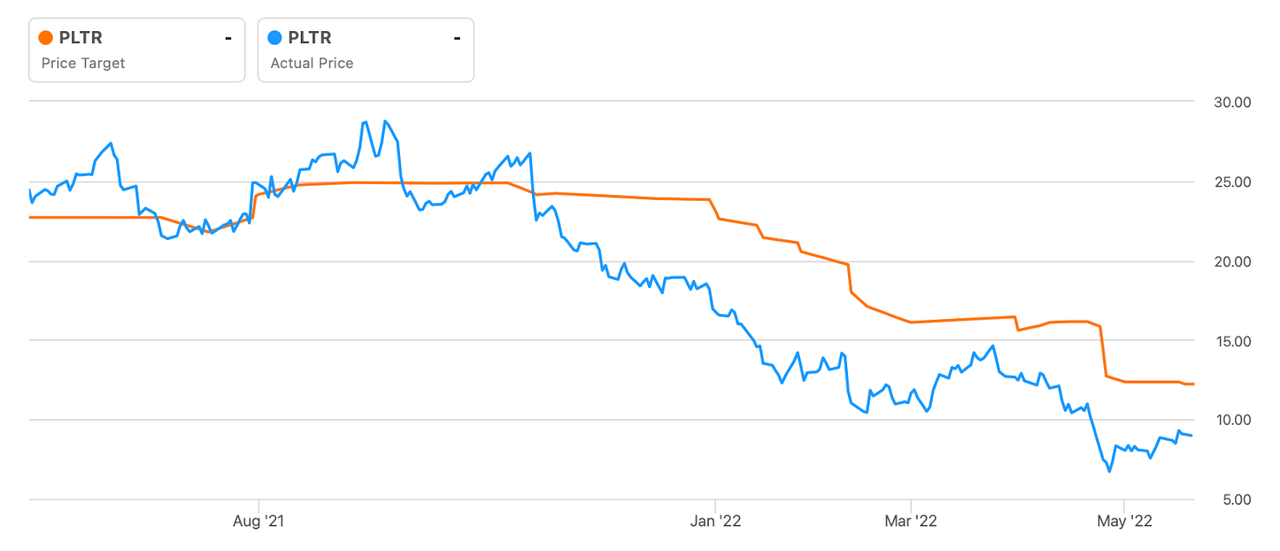

PLTR peaked near $40 per share and was recently trading at around $9 per share, just below the price where it came public nearly two years ago.

I last covered the name in March when I rated it a strong buy and the stock has since dropped another 19%. The ongoing price weakness should be considered a protracted opportunity to accumulate shares on the cheap.

PLTR Stock Key Metrics

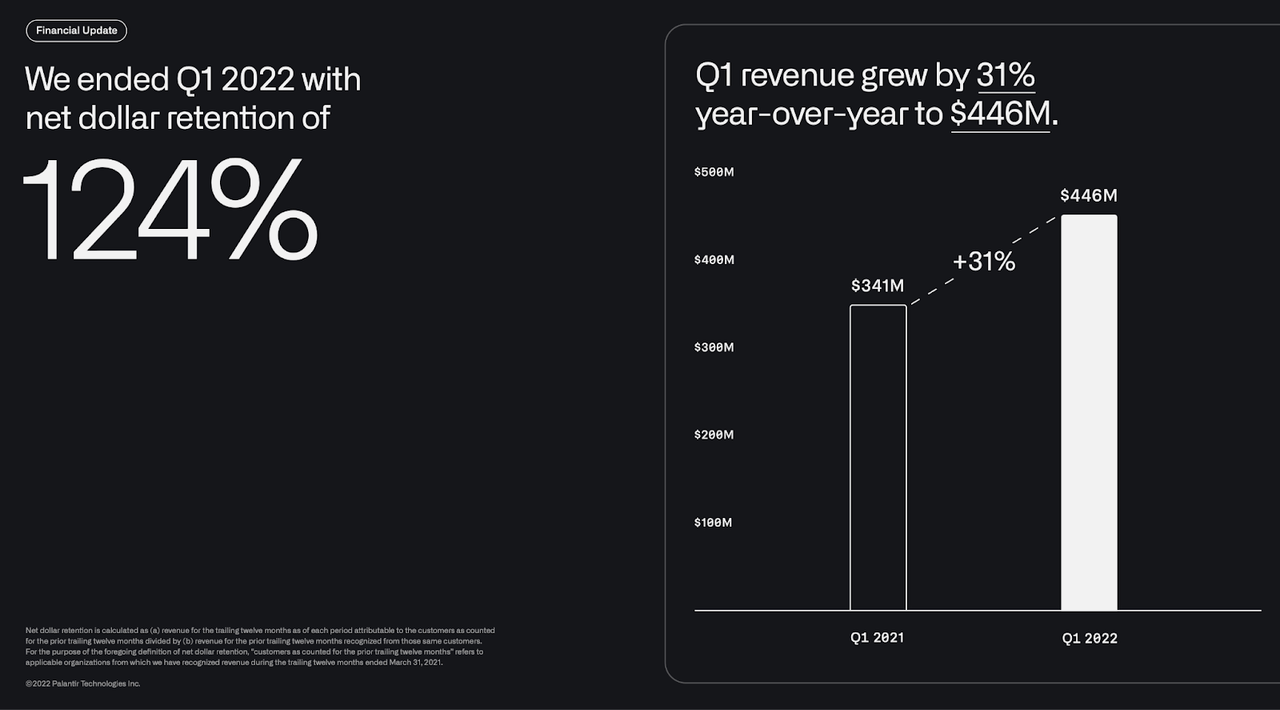

In the latest quarter, PLTR grew revenue by 31% on the backs of 124% net dollar retention.

2022 Q1 Presentation

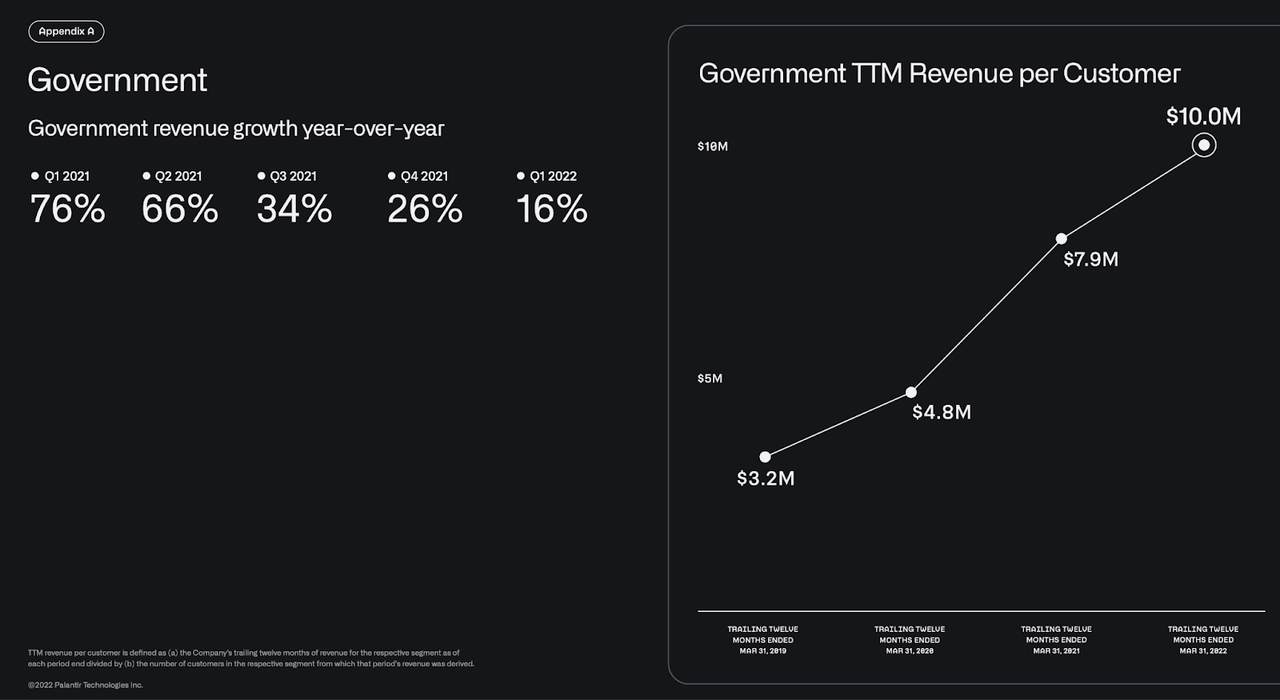

A typical criticism against the company has been its reliance on government revenues. Government revenue growth actually decelerated to only 16% in this past quarter. On the conference call, management indicated that growth of government revenues should accelerate in the second half of the year.

2022 Q1 Presentation

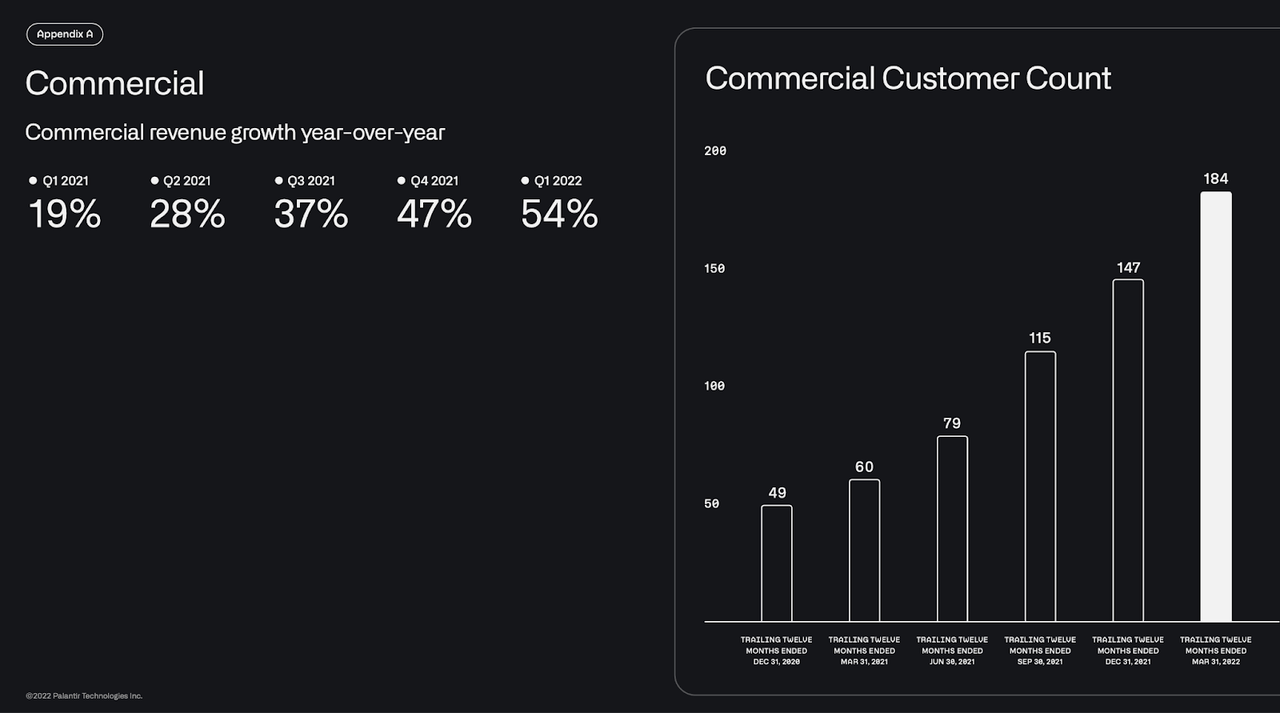

It was commercial revenue growth of 54% that helped offset that slowdown.

2022 Q1 Presentation

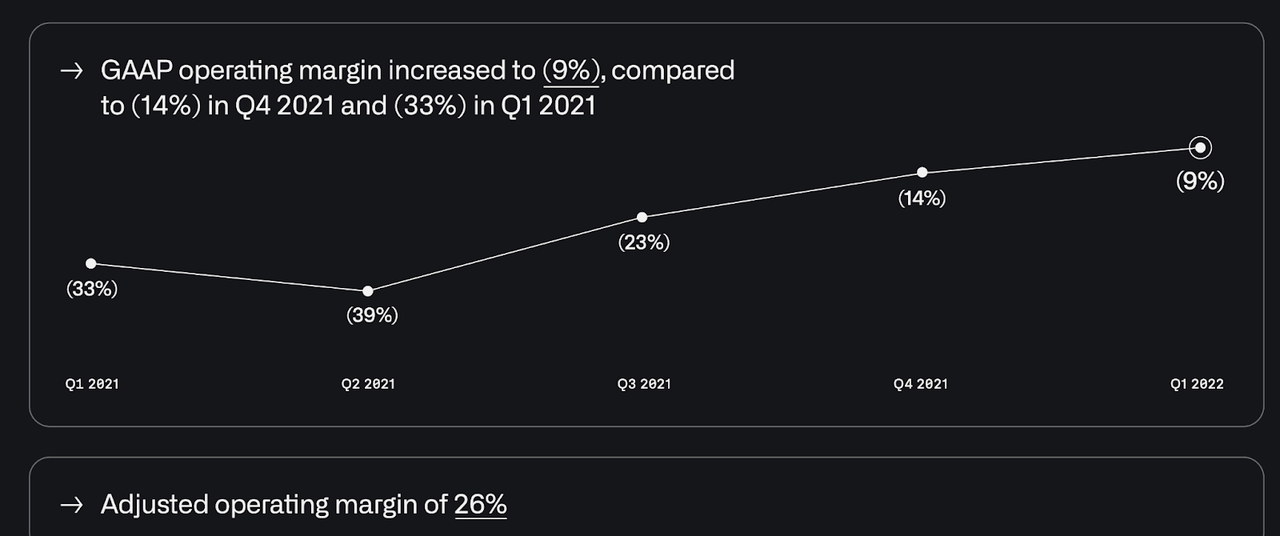

PLTR continues to generate robust free cash flows and generated a 26% adjusted operating margin in the quarter. That margin includes stock-based compensation, so the shares outstanding are still being negatively impacted. Yet from a financial solvency perspective, the company is on strong footing. The company did make progress on profit margins on a GAAP basis, with GAAP operating margin loss compressing to 9%, a sizable improvement from the negative 33% margin in the prior year.

2022 Q1 Presentation

On the earnings call, an analyst asked management about their expectation for when to expect GAAP profitability. Management basically deflected the question - investors should expect the company to continue investing aggressively, at least in the near term. PLTR ended the quarter with $2.3 billion of cash versus no debt. That is good for around 13% of the current market cap.

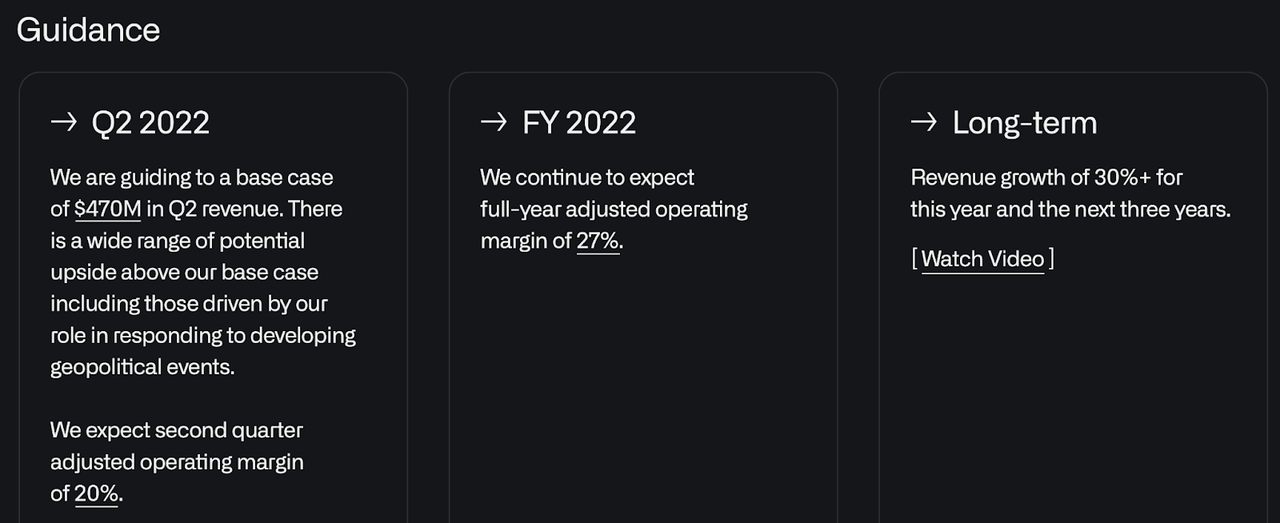

Looking forward, PLTR guided for $470 million of revenue in the next quarter, representing only 25% year over year growth.

2022 Q1 Presentation

Some investors have tried to justify the post-earnings 20% decline by that guidance, as it seems to call into question management’s long-term guidance of 30% growth (even though on that same slide the company reiterated its outlook of at least 30% revenue growth over the next three years). Has the thesis broken down? Hardly. PLTR is a curious example of a business which still operates like it is pre-IPO yet has achieved post-IPO valuations. PLTR’s products are still arguably years ahead of their time, meaning that it will take time for its customers to fully understand how to use its products. This is shown clearly by the fact that the 31% revenue growth lagged the 86% growth in total customers. Given everything that is going on right now, it makes sense that customers aren’t getting too adventurous in using PLTR’s products to the full extent. That will inevitably change as they slowly but surely see the tremendous value that PLTR provides.

Is Palantir Stock A Good Valuation?

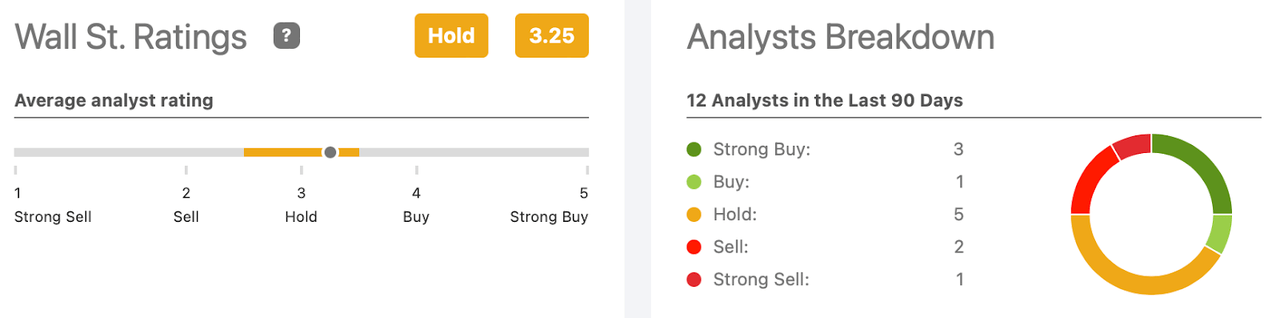

It appears that the falling prices in the tech sector have influenced Wall Street’s sentiment toward the stock. In spite of the huge plunge in the stock price, the average rating stands at only 3.25 out of 5.

Seeking Alpha

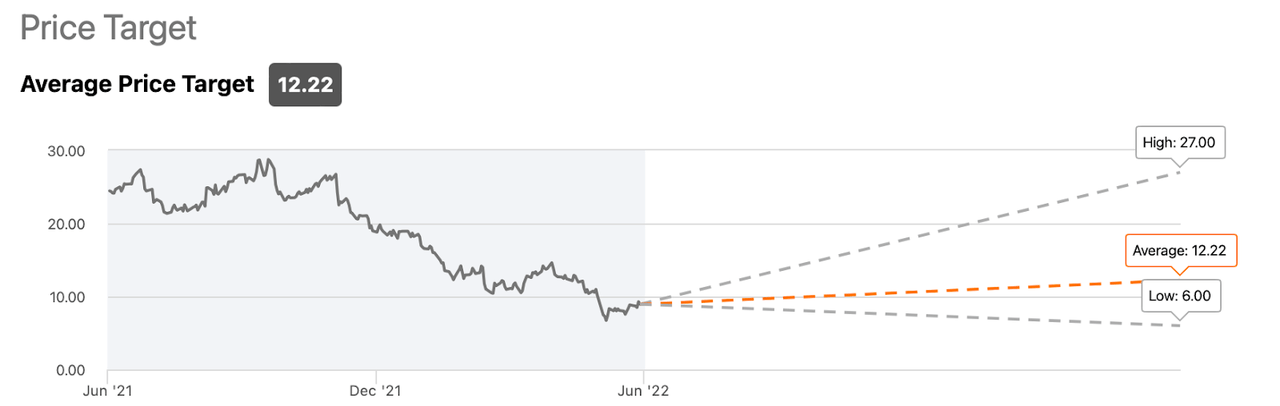

The average price target of $12.22 per share represents only 35% potential upside.

Seeking Alpha

We can see below that the average price target has declined rapidly over the past few months alongside the crash in tech stocks.

Seeking Alpha

Is Now A Good Time To Invest In Palantir?

I have a strong belief that the best time to buy stocks is when sentiment is low. The fact that price targets have come down so rapidly is a good indication of the poor sentiment surrounding PLTR stock. While PLTR stock is trading as if it is a tech stock going out of business, the reality is anything but.

Recall that PLTR is a best of breed operator helping its customers harness the true value of its data. I view PLTR to be as close as any company to being the enabler of “Skynet” (a Terminator reference).

2022 Q1 Presentation

PLTR has made the bold claim that it will be the next Amazon Web Services (‘AWS’).

2022 Q1 Presentation

That’s clearly an ambitious goal. Yet as data continues to grow, PLTR’s products only become more and more valuable as its customers look to further optimize their businesses in ways that humans alone cannot achieve. PLTR remains the best positioned company to help the world harness the power of artificial intelligence.

What Is Palantir's Outlook?

Consensus estimates call for around 28% growth through 2024 - noticeably lower than management’s outlook for at least 30% growth over the next three years.

Seeking Alpha

PLTR’S ability to sustain elevated growth rates for many years is what makes the stock so compelling here.

Is PLTR Stock A Buy, Sell, or Hold?

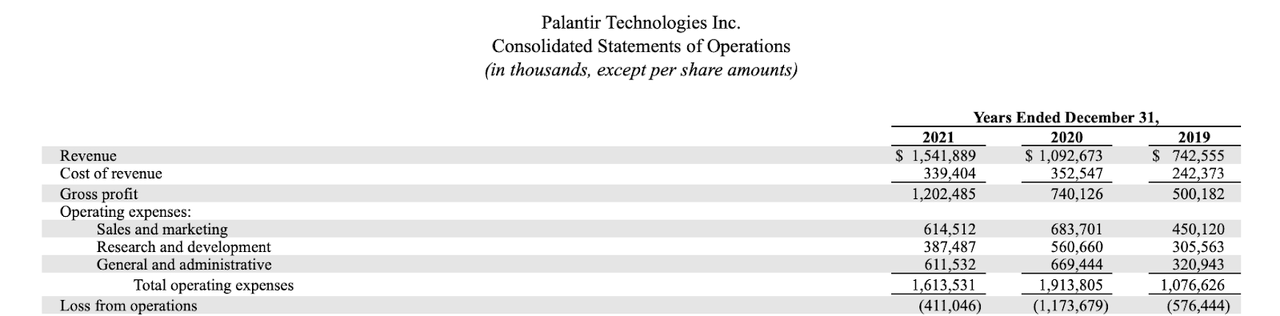

The stock is trading at 9x forward sales. That might not seem that cheap, especially considering that PLTR is still not yet profitable on a GAAP basis. Yet as operating leverage takes hold, I expect PLTR to eventually generate robust profit margins. There are already signs of operating leverage taking place. Below we can see the 3-year financial snapshot - operating expenses have already moderated significantly over the past year.

2021 10-K

I can see PLTR eventually sustaining at least 30% net margins over the long term. Assuming a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see PLTR trading at around 13.5x sales by 2024. That presents 141% potential upside, representing around 40% compounded returns over the next 2.5 years. What are the key risks here? I am not concerned with financial solvency risk due to the cash-rich balance sheet and free cash flow generation. But if the company is unable to realize operating leverage, perhaps due to factors like competition, then it may not produce sufficient GAAP profits to justify an investment over the long term. This is a key risk when investing in any unprofitable company. Over the near term, another risk is if growth rates suddenly decelerate rapidly - this would likely lead to material compression in the valuation multiple. I have the view that PLTR has a long growth runway ahead of it but would be a quick seller if the company was unable to meet its outlook for 30% average growth. I rate the stock a strong buy as the underlying growth and multiple expansion potential both make this a compelling buy at current prices. PLTR is one of the core holdings in the Best of Breed portfolio and one I intend to hold over the long term.

Comments