Times are tough for Tesla. Demand is slowing. Costs are rising. Elon Musk is distracted and a distraction.

It’s time to buy the stock.

Yes, Tesla (ticker: TSLA) is a mess right now, and signs point to difficult times ahead. The wait time for U.S. buyers of its cars has shrunk from more than three months to, well, nothing. Delivery growth has slowed below the company’s own goal, while production has exceeded deliveries by an increasing amount in recent quarters and prices are getting cut, all signs of waning demand. Musk’s behavior since taking over Twitter has also raised questions about whether shoppers will buy other electric vehicles now that they are available. And the U.S. could face a recession by the end of the year.

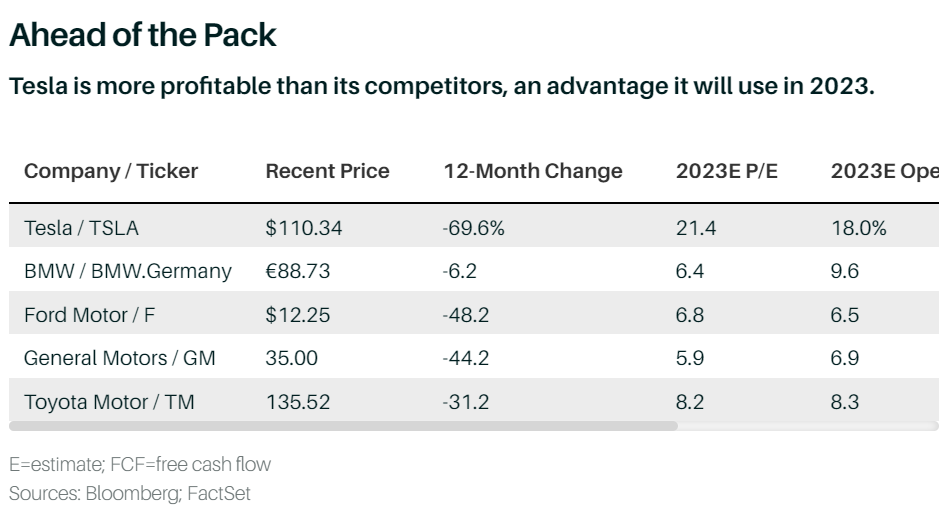

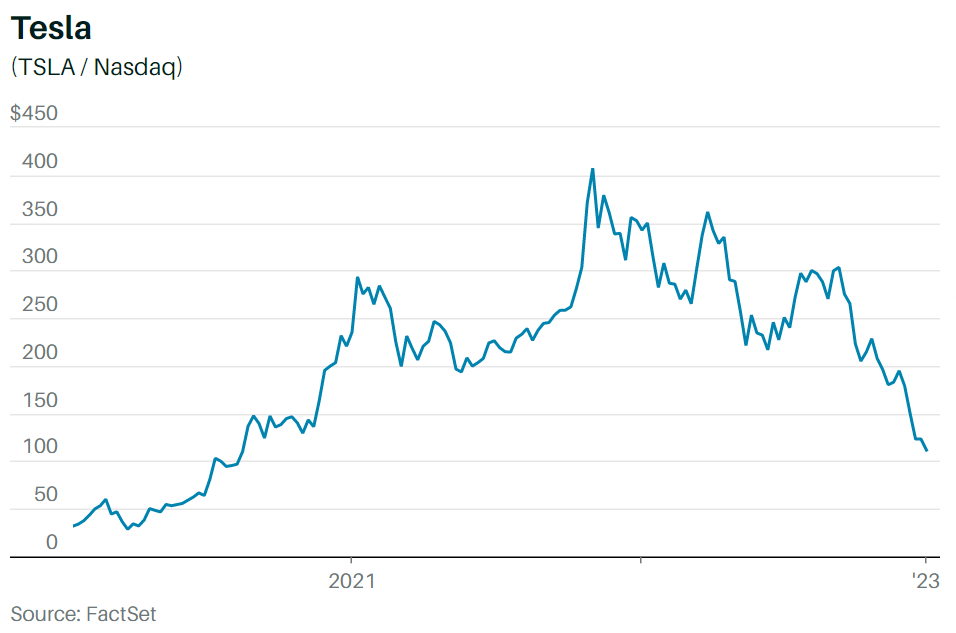

Ignore all that. Instead, focus on what Tesla is—the leading EV manufacturer in the world and one that has a decade-plus head start on other auto makers, as well. Tesla is able to produce cars at a much lower cost than its competitors, giving it room to cut prices to stoke demand in a way others can’t. Tesla stock is a risky bet, to be sure, but with shares off 72% from their all-time high, to $113.06, and near 21 times 12-month forward earnings, down from 201 times two years ago, the opportunity is too good to pass up.

Friday’s news that Tesla would be cutting prices in China underscores the current dilemma. Tesla has been focused on growing production—it plans on making 2 million cars in 2023, up from 1.4 million in 2022—triggering concerns it will make too many cars and then be forced to cut prices to sell them all. That seems to be what’s happening in the world’s second-largest economy, where Tesla cut prices for its Model 3 by 14% and the Model Y by 10%. Those price cuts, which may be coming to the U.S. in the future, will hurt its profit margins, and Wall Street’s per-share earnings estimates for 2023 have already slipped 10% since the end of September. That dynamic puts Tesla in a bind.

“Tesla will need to either reduce its growth targets, and run its factories below capacity, or sustain and potentially increase recent price cuts globally, pressuring margins,” writes Bernstein analyst Toni Sacconaghi, who rates the stock Underperform.

For Tesla, the choice is obvious: It will cut prices to juice sales. That will hit its margins, but Tesla has margin to spare. It is expected to post operating margins of 18% in 2023, while the rest of the industry’s should be closer to 8%. Tesla could sacrifice some 10 percentage points of margin and still be as profitable as, say, BMW (BMW.Germany). Ultimately, Tesla has the ability to sacrifice profitability if it means undercutting competitors on price.

“Arguably, if [Tesla] cuts price, it’s a worse situation for their competitors, given many struggle to make any profit,” explains RBC Capital Markets analyst Joseph Spak.

What’s more, Tesla is one of only two auto makers that makes a profit off EVs; the otheris BYD (1211.Hong Kong). Everyone else is losing money, even General Motors (GM), which sells a $110,000 Hummer and has targeted EV profitability by 2025. Others, like Toyota Motor (TM), appear to be getting cold feet in the rush to meet EV demand that may not materialize.

Most EV start-ups, including Rivian Automotive (RIVN) and Lucid Group (LCID), are far from profitable and don’t have the scale to compete. It’s a precarious position to be in at a time when investors are demanding profitable growth, and not just growth.

Numbers like that demonstrate why Tesla, with a market cap around $350 billion, is the world’s most valuable car company, even after dropping 69% over the past 12 months.

It helps that Tesla is expected to generate the most free cash flow among auto makers in 2023, some $12.2 billion, up from $9 billion in 2022. Toyota, the second-most-valuable auto company, is expected to generate free cash flow of about $10 billion this year and next. But even price cuts shouldn’t hit Tesla too hard, says New Street Research analyst Pierre Ferragu, who projects almost $11 billion in Tesla’s 2023 free cash flow while assuming its vehicle prices drop 8% over 2022.

Tesla isn’t stopping there. It plans to launch its much-delayed Cybertruck in 2023, and could also announce a badly needed lower-cost car at its investor day scheduled for March 1.

And like it or not, Tesla is more than just a car company. Its “self-driving” software, though still far from living up to its name, continues to improve, and drivers have shown a willingness to pay $15,000 for its top driver-assistance software. That’s a product—and revenue line—no other auto maker has.

It also has a $12 billion nonautomotive business based on renewable-power generation and battery-storage technologies, which is only getting bigger. Tesla quietly opened a “megapack” facility in Lathrop, Calif., in 2022. It’s designed to produce up to 40 gigawatt hours of utility-scale battery storage a year, something Future Fund Active exchange-traded fund co-founder Gary Black sees generating up to $3 billion in incremental operating profit a year.

Nor is the EV business as bad as it seems. In China, EV sales grew about 90% in 2022, accounting for 25% to 30% of all new car sales. In the U.S., battery-powered EV sales increased 70% through the first three quarters of last year, and Canaccord analyst George Gianarikas expects tax credits to help spur sales growth in 2023.

Tesla, of course, still has many issues. Since Musk’s acquisition of Twitter in late October, the company has taken a reputational hit, with more people now having an unfavorable view of Tesla’s brand than a positive one, according to a December YouGov poll. It appears to have taken an operational hit as well, with two-thirds of respondents in a Morgan Stanley poll saying they believe that Musk’s behavior at Twitter is hurting Tesla’s fundamentals.

Nowhere was that more clear than in Tesla’s fourth-quarter deliveries, released on Jan. 2. It delivered 405,278 vehicles, well below analyst projections for about 420,000. Tesla’s stock dropped 12% on Jan. 3, its worst start to a year ever, and Musk got most of the blame, though there were a lot of headwinds, from lockdowns in China and inflation pressuring potential car buyers. “He is viewed right now, fairly or unfairly, as asleep at the wheel,” says Wedbush analyst Dan Ives. “It’s not a good look from the Street’s view.”

Musk has also been selling stock in a haphazard manner far from the organized 10b5-1 trading plans most CEOs use. The selling doesn’t need to stop, but even longtime shareholders are losing patience with Musk’s do-it-yourself approach. “I am confused why [the board] allowed Elon to crash Tesla stock price,” says Leo Koguan, chairman of SHI International and Tesla’s third-largest individual shareholder. “Why not use block sales?” Tesla’s board didn’t respond to a request for comment.

Worse still, a recession has become the base case for many economists heading into 2023. Recessions typically mean new-car sales drop by around a third, though sales in the U.S. are already 20% below prepandemic levels due to persistent parts shortages. A slowdown, though, would also give Tesla time to develop a badly needed lower-cost model, especially if other auto makers decided to spend less aggressively on EVs. “A recession could slow Tesla in 2023, but the company is by far best positioned to fly through tough times,” Ferragu writes. “Recent concerns are overblown.”

Even if they aren’t, Tesla stock appears cheaper than it has ever been. Shares trade for just 21 times 12-month forward earnings, making it less expensive than PepsiCo (PEP), Visa (V), and Walmart (WMT). Other methodologies also point to Tesla trading at what looks like a reasonable valuation. Sacconaghi, who is a bear, has a discounted cash-flow-based valuation of $120 a share, and admits he is “torn” on the stock at current levels. Spak’s multiple-based valuation puts Tesla’s value at $186, up 65% from Friday’s close, while Ferragu, who has a Buy rating on Tesla stock, has a $320 price target, up 183%. “We see room for the stock to nearly triple if 2023 plays out our way,” Ferragu says.

Nothing would do more to help Tesla stock find a bottom than for Musk to swat away his Twitter distraction, a process that seems to have already started. The social-media company is making a concerted effort to woo advertisers that had been abandoning the platform. It planned to have its representatives meet with clients and ad agencies at this year’s CES tech show. Now Twitter needs to find someone who can run the company on a daily basis and let Musk focus on other things.

“Elon needs to hire a new CEO at Twitter to get the Twitter noise out of Tesla’s stock price,” says Future Fund’s Black. “It will show investors he is 100% focused on Tesla, with all its opportunities and risks, on its path to a $3 trillion valuation.”

That valuation might seem far-fetched, but it doesn’t need to reach those levels to make it a good investment. Tesla is a volatile stock, and it could even fall from here in the short term. But looking out a year or two, Tesla is unlikely to be trading below or even near $100.

Get it while it’s cold.

Comments