Investors got their Goldilocks jobs report on Friday morning, with a growing-but-slowing labor market, a tick-up in participation, and a deceleration in the pace of wage gains.

It was the kind of release that makes an oft-wished-for soft landing seem almost possible.

If job growth can continue without fueling a wage-price spiral, then perhaps it won't take a recession to break the back of inflation, especially as increases in commodities and goods prices continue to reverse. The Federal Reserve could declare victory in its inflation fight and ease off its monetary policy tightening sooner rather than later in 2023, setting off rallies across asset classes.

So goes the bullish thinking.

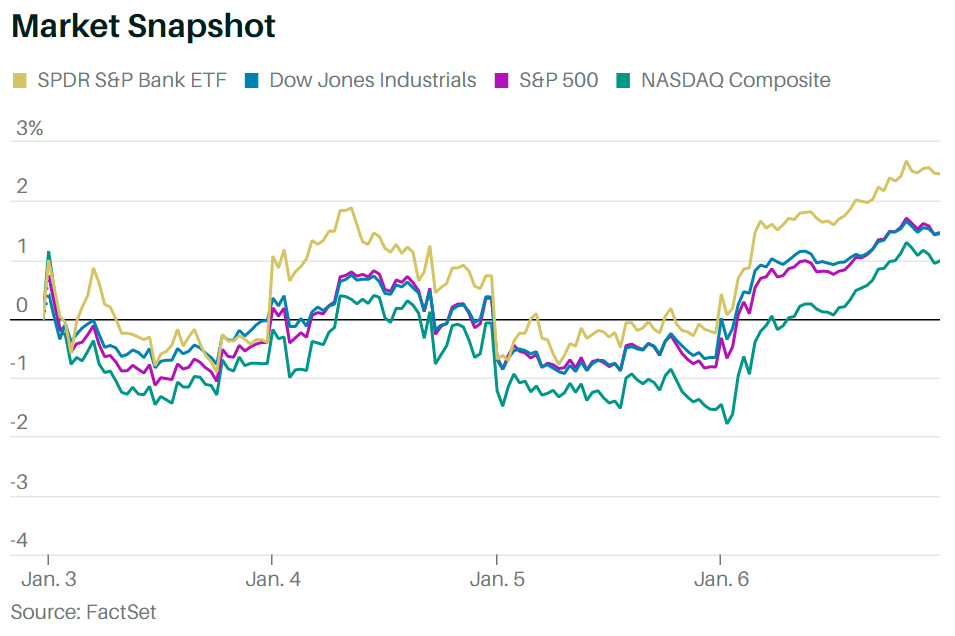

That narrative was on display this past Friday when stock indexes surged to end a choppy holiday-shortened week higher. The S&P 500 finished the week up 1.45%, the Dow Jones Industrial Average added 1.46%, and the Nasdaq Composite ticked up 0.98%.

If all that sounds familiar, it should. The Fed has stated that it plans to increase interest rates in early 2023, then hold there for some time. Federal-funds futures pricing, however, implies a peak in rates by the spring, then cuts in the back half of 2023. It's another sign that investors expect the Fed to change its tune. They hope Friday's jobs report sent the Fed a message -- its job is almost done.

One data point, however, won't be enough to change the Fed's mind. The market will be looking to December's consumer price index this coming Thursday as its next macro bogey -- one that will provide additional fodder for the Fed's next policy meeting in February. The rate of inflation is expected to fall to 6.5% year over year from 7.1% in November.

But it's not just about the economic data. This coming Friday brings the start of fourth-quarter earnings season, with some major companies -- JPMorgan Chase (ticker: JPM), Bank of America (BAC), UnitedHealth Group (UNH), and Delta Air Lines (DAL) among them -- kicking off the festivities. The vast majority of the S&P 500 will report over the following month and a half.

Few are expecting a good fourth quarter. In aggregate, S&P 500 companies are expected to report their first losing quarter since 2020. Earnings per share are forecast to decline by 2.2% year over year, to $53.87, after roughly 4.4% growth in the third quarter and 8.4% in the second quarter, per IBES data from Refinitiv. The consensus fourth-quarter outlook became much gloomier as 2022 proceeded -- at the start of last year, analysts had penciled in 14.1% year-over-year earnings growth for the period.

Analysts' current estimate would bring 2022 S&P 500 EPS to $219.80, which would be up 5.6% for the year. It's likely to end up a bit better than that, as most companies tend to beat consensus estimates. Revenue, though, is forecast to rise 4.1% year over year in the fourth quarter, to $3.7 trillion, and 11.2% for all of 2022, to $13.8 trillion. The fact that sales are rising but earnings are falling is a sign that corporate profit margins appear to have peaked for this cycle.

The earnings slump won't hit all companies equally. The energy and industrial sectors are expected to be outliers, delivering EPS growth of 65% and 43%, respectively, from a year earlier. Those are among the cyclically sensitive companies that suffered the most during the Covid-19 recession and are still enjoying the rebound.

On the opposite end of the spectrum are materials, where earnings are forecast to drop by 22% as prices of many industrial inputs have returned to earth; communication services, down 21% due to an expected drop in advertising spending and continued streaming losses at many media companies; and consumer discretionary, down 15% on potentially weaker spending in 2023. Tech, which makes up close to a quarter of the S&P 500's EPS, is expected to show a 9% decline in earnings in the fourth quarter as wage costs balloon at many software companies, enterprise demand slows, and semiconductors remain in a downturn. Expectations are so low that the fourth-quarter results could be strong relative to forecasts.

But those beats might not matter if companies can't provide at least a decent outlook for 2023.

The bottom-up consensus -- gleaned by summing the average earnings estimates from all individual stock and sector analysts for each of the companies in the S&P 500 -- is for EPS to grow by 4.4% to $229.52 in 2023, according to Refinitiv, up from about $220 in 2022. Conversely, the top-down view of Wall Street strategists surveyed by Barron's in December calls for a 2.7% decline in S&P 500 profits in 2023 to an average of $214 per share.

The difference is in the profit margins. Strategists see them getting squeezed by rising wages and higher interest costs, even as the prices they charge customers moderate. That's largely in line with the Fed's view that some elements of inflation are sticky and will take time -- and economic pain -- to bring down. If that scenario plays out, the shift lower in earnings expectations would make the market appear pricier even as the Fed continues to increase interest rates.

Needless to say, that's not a winning combination for stocks -- no matter what the jobs report said.

Comments