Following an 18% decline for the S&P 500 index (with dividends reinvested) in 2022 and a volatile and disappointing pullback from this year's stock-market rebound that crested early in February, some investors may need to be reminded about how well patience can be rewarded.

And for those who want to have some exposure to individual stocks of companies that appear primed for rapid growth, the screen of the benchmark index below highlights 11 companies analysts expect to excel in three important areas. This can be a starting point for your own research.

First, take a look at this 10-year price chart for the SPDR S&P 500 ETF Trust $(SPY)$, which tracks the benchmark index :

That is a pretty good looking chart, but a close look shows many broad declines over the past 10 years through March 24. For the entire period, SPY's price increased 153%, while its total return, with dividends reinvested, was 205%.

So patience has been rewarded -- investors who were faithful and reinvested tripled their money.

For a long-term investor looking a build a retirement nest egg over decades before switching to an income strategy, pouring money steadily into a broad index fund with low expenses can pay off -- one of the benefits of staying that course is you pay lower prices during periods of weakness to enhance long-term returns.

But what about more aggressive investors looking profit by riding along with individual companies? There is plenty of coverage for day-traders, including those who periodically look to jump on trendy bets for meme stocks. But even investors looking to juice returns with individual growth stocks can focus on quality for a long-term approach.

The following screen began with the S&P 500 and then used consensus estimates among analysts polled by FactSet to narrow down the list as follows:

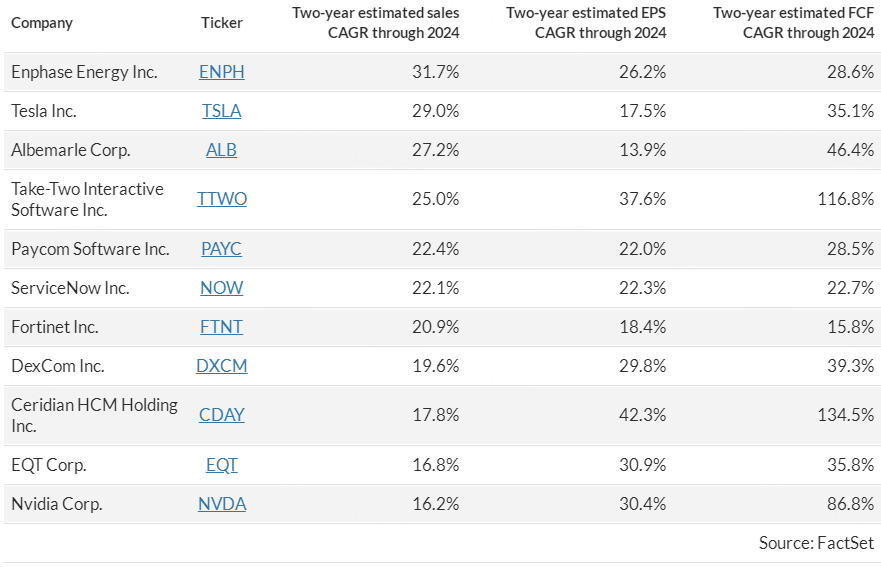

- We used calendar-year consensus estimates for 2022, 2023 and 2024 for a uniform set of data. About 20% of S&P 500 companies have fiscal years that don’t match the calendar, and some of these don’t even match calendar month-ends. So even the 2022 data are estimates; they are based on actual financial reports covering the period.

- Any company for which consensus estimates were unavailable or negative for earnings or free cash flow per share for any year was excluded. This brought the list down to 290 companies. Free cash flow is a company’s remaining cash flow after capital expenditures. It is money that can be used to expand, pay dividends, repurchase shares or other corporate activities that (hopefully) benefit shareholders.

- Then we narrowed further to companies for which the estimates predict compound annual growth rates (CAGR) of at least 15% for sales, 10% for earnings per share (EPS) and 10% for free cash flow per share (FCF) from 2022 through 2024. This brought the list down to 11 companies.

The focus on sales growth underlines that this is an initial screen for aggressive long-term investors. Those two terms might seem contradictory, but day-trading isn't the only approach to allocating some of your portfolio in a bold manner to take more risk in a push for growth.

Here's the list, sorted by expected sales CAGR from 2022 through 2024:

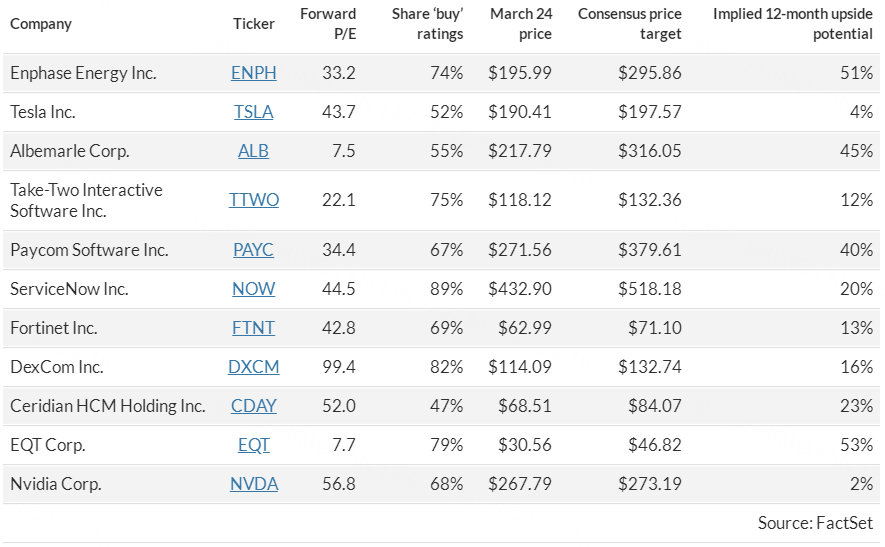

Most of these stocks appear expensive by traditional measures. Then again, the same could be said for Amazon.com Inc. $(AMZN)$, whose forward price-to-earnings ratio has averaged 69.6, while ranging from 45.7 to 148.7 over the past 10 years, as the stock has risen by 640%.

For the entire S&P 500, the weighted forward P/E ratio is now 17.6, down from 21.5 at the end of 2021, according to FactSet.

So here are forward P/E ratios for the 11 stocks that passed the screen, along with a summary of analysts' opinions:

If you see any companies of interest, you should do your own research to form your own opinion about a company’s viability over the next 10 years, at least, before making a commitment.

Comments