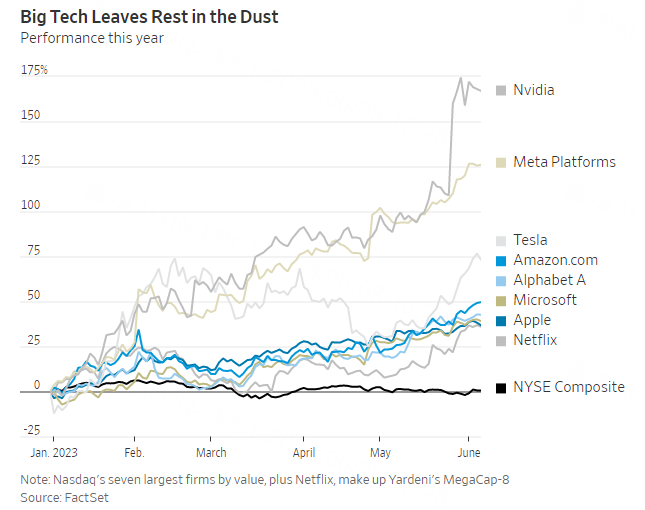

Investors need a new acronym. The FANGs and various remixes worked for a while, but 2023 has expanded the market leadership to seven, or perhaps eight, stocks that now dominate the market and seem to move to a different tune to the rest.

There's no word -- in English at least -- that neatly links Nvidia, Apple, Microsoft, Amazon, Meta (nee Facebook), Alphabet (Google), Tesla and the optional Netflix, and my creative efforts have come to naught. Wall Street's attempts haven't really caught on, although Ed Yardeni of Yardeni Research's "MegaCap-8" is simple and to the point.

But the renaissance of megacapitalization companies matters. These stocks account for the shift from a bear to a tentative new bull market. And their resurgence comes alongside significant shifts in market behavior, especially when it comes to interest rates. In particular, the megacap stocks no longer seem to care what the Federal Reserve does.

The question is whether the new market narrative can last. If it can, buy the <acronym to come> stocks. The alternative is that these companies got lucky by being at the intersection of several supportive stories, at least some of which may have run their course. I lean toward the second view, with these being the themes:

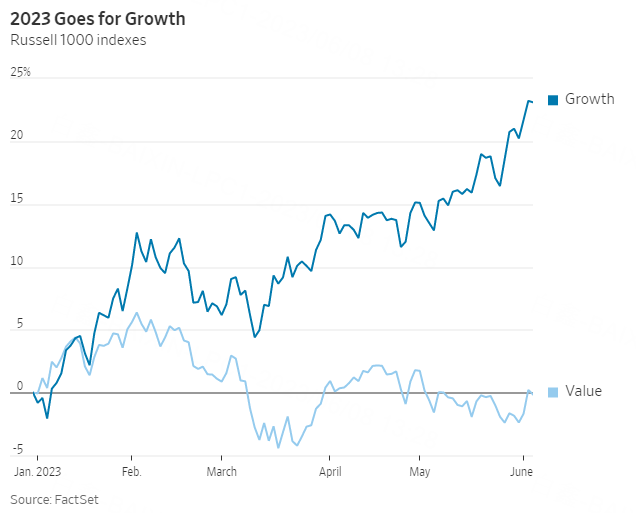

-- Quality. Most, though not all, of this year's big winners are hugely cash-generative firms with strong balance sheets, the definition of "quality" companies in Wall Street parlance. While the widely forecast recession hasn't yet arrived, the combination of recession danger and the bank runs that started in March make quality stocks attractive. -- Growth. Even if there's no recession, slower economic growth is inevitable. That makes stocks that grow whatever the broader economic trends -- as investors assume the big stocks do -- more attractive. -- Artificial intelligence. Nvidia is already a winner from the latest iteration of AI, and the others are all thought to be winners, either because they invest a lot in it or because their cloud services are used by it. I think too much is already priced in, but it's clearly helped this year. -- Interest rates may not have peaked, but they are almost certainly now close to the peak. Stocks that were last year crushed by rising rates and bond yields become less sensitive when the threat of big further Fed rises is removed.

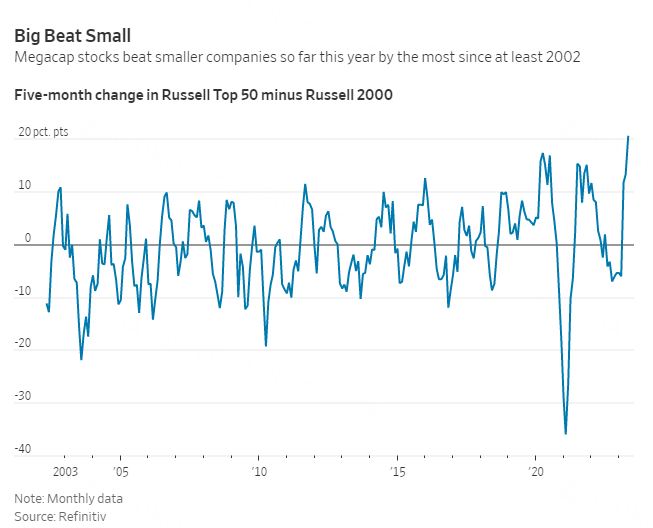

Taken together, these tailwinds have pushed the biggest stocks as measured by the Russell Top 50 Mega Cap index to beat the Russell 2000 index of smaller companies by more than 20 percentage points this year, better than any five-month period from the creation of the measure in 2002 up to the pandemic.

They've also left the rest of the market in the dust, as other stocks go sideways. And since March, when bank runs began, the link between higher interest rates and lower prices for growth stocks such as the MegaCap-8 that held for most of last year has evaporated, with yields becoming irrelevant. A plausible explanation is that with the Fed probably close to peak rates any further rises will be relatively small.

What can go wrong for buyers of what are undoubtedly some of the world's greatest companies? The usual mistake is to overpay; companies that everyone agrees are great are more likely to be overpriced than ones everyone agrees are rubbish. This is my objection to Nvidia, the most obvious winner from AI. It probably will be a big winner, but everyone already knows this.

The second mistake is that the companies might not be what you think. Meta has done well this year but its forecast sales per share are still lower than at the start of last year, not the usual hallmark of a growth company. Expectations for Tesla's earnings and sales have both fallen sharply this year, although that hasn't stopped its shares soaring to 54 times forecast earnings.

Alphabet and Meta both rely on online advertising, which has matured and so may be vulnerable to economic weakness. Amazon's online retailing is likewise susceptible. And the stickiness of Netflix's streaming subscribers is still untested in a normal recession, which won't bring the stuck-at-home subscriptions the company enjoyed in the lockdown. Are these companies really resistant to recession?

The third danger is that known risks aren't properly priced. In the case of Big Tech, the risk is of a new regulatory and antitrust onslaught, as they've lost their popularity with the public and politicians. This is unpredictable and hard to price, but potentially very significant -- as with the antitrust regulators in the U.S. and U.K. trying to stop Microsoft from buying videogame maker Activision Blizzard.

Comments