It will be the busiest week of second-quarter earnings season, with a third of S&P 500 companies scheduled to report. Economic-data highlights will include the latest U.S. jobs data and purchasing managers’ indexes.

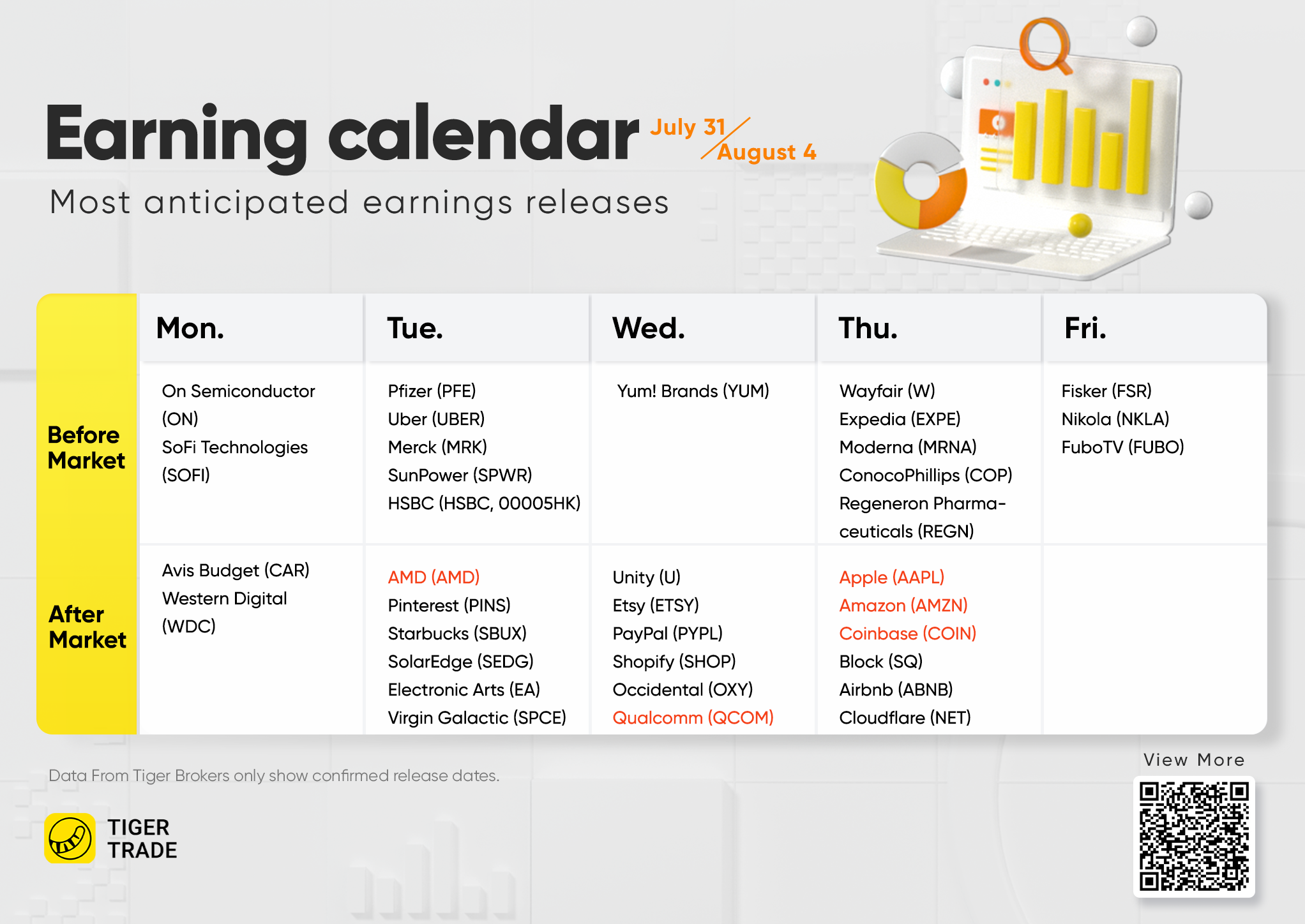

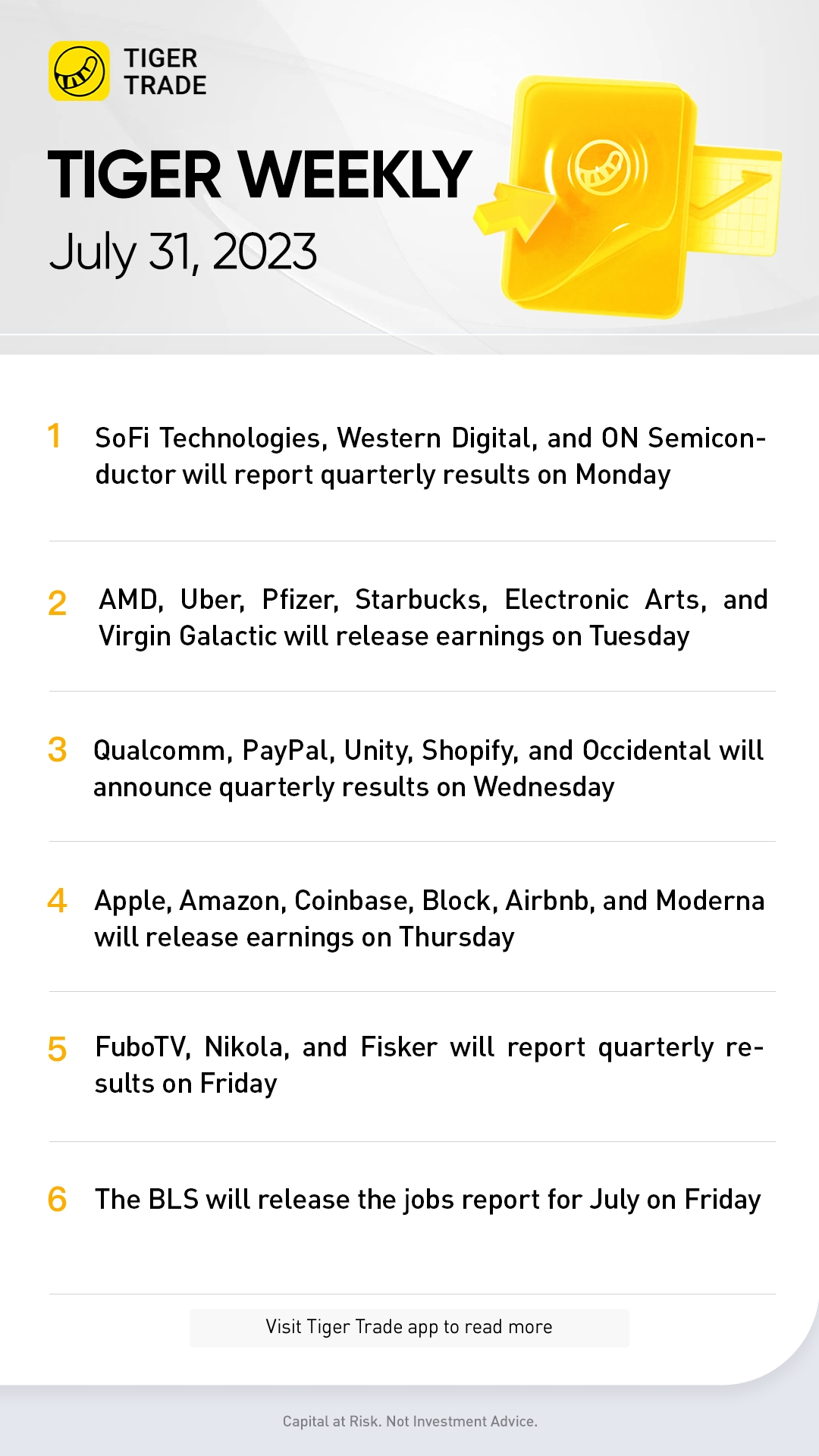

SoFi Technologies reports on Monday, followed by Advanced Micro Devices, Uber Technologies, Pfizer, Merck, Starbucks, and Pinterest on Tuesday.

Wednesday’s earnings highlights will include CVS Health, PayPal Holdings, Qualcomm, Shopify, and Simon Property Group. Apple, Amazon. com, Coinbase, and Airbnb release results on Thursday, then FuboTV, Nikola, and Fisker close the week on Friday.

The Bureau of Labor Statistics releases the Job Openings and Labor Turnover Survey on Tuesday. Economists are forecasting a slight decline in job openings from the prior month.

Then there’s Jobs Friday. Economists are expecting to see a gain of 200,000 nonfarm payrolls in July, following a rise of 209,000 in June. The unemployment rate is expected to remain at a historically low 3.6%.

Finally, the Institute for Supply Management releases its manufacturing purchasing managers index for July on Tuesday, followed by the services equivalent on Thursday.

Monday 7/31

SoFi Technologies, Western Digital, Arista Networks, AvalonBay Communities, ON Semiconductor, and Republic Services report quarterly results.

The Institute for Supply Management releases its Chicago Business Barometer for July. Consensus estimate is for a 42.5 reading, one point more than in June. The index has posted 10 consecutive monthly readings below the expansionary level of 50, yet the economy continues to grow at a decent clip, posting a 2.4% seasonally adjusted annual growth rate for the second quarter.

Tuesday 8/1

Advanced Micro Devices, Altria Group, BP, Caterpillar, Ecolab, Devon Energy, Eaton, Electronic Arts, Marriott International, Merck, Pfizer, Pioneer Natural Resources, Rockwell Automation, Starbucks, and Uber Technologies release earnings.

The Bureau of Labor Statistics releases the Job Openings and Labor Turnover Survey. Economists forecast 9.7 million job openings on the last business day for June, slightly less than in May. This past week, Fed Chairman Jerome Powell reiterated that “labor demand still substantially exceeds the supply of available workers.”

The ISM releases its Manufacturing purchasing managers index for July. The consensus call is for a 47 reading, slightly higher than in June. The index has been below 50 for eight consecutive months.

Wednesday 8/2

Albemarle, Clorox, CVS Health, DuPont, Emerson Electric, Equinix, Humana, Kraft Heinz, McKesson, Occidental Petroleum, PayPal Holdings, Phillips 66, Qualcomm, Shopify, and Simon Property Group announce quarterly results.

ADP releases its National Employment Report for July. Economists forecast an increase of 183,000 private-sector jobs, after a gain of 497,000 in June. The median change in annual pay was up 6.4% in June according to ADP.

Thursday 8/3

Apple, Amazon.com, Coinbase, Block Inc., Airbnb, Amgen, Becton Dickinson, Booking Holdings, Cigna Group, ConocoPhillips, Expedia Group, Gilead Sciences, Intercontinental Exchange, Kellogg, Moderna, Motorola Solutions, Regeneron Pharmaceuticals, SouthernCo. , and Stryker hold conference calls to discuss earnings.

The ISM releases its Services PMI for July. Consensus estimate is for a 53.1 reading, slightly less than the June data. The services sector continues to show strength, especially when compared to the manufacturing sector.

Friday 8/4

FuboTV, Nikola, and Fisker report quarterly results.

The BLS releases the jobs report for July. The economy is expected to add 200,000 nonfarm payrolls following a 209,000 gain in June. The unemployment rate is seen remaining unchanged at a historically low 3.6%. The labor market remains tight and jobs growth has mostly surprised to the upside in the past year.

Comments