Smaller, speculative companies are in the midst of a furious autumn stock-market rally, but they still have an interest-rate problem.

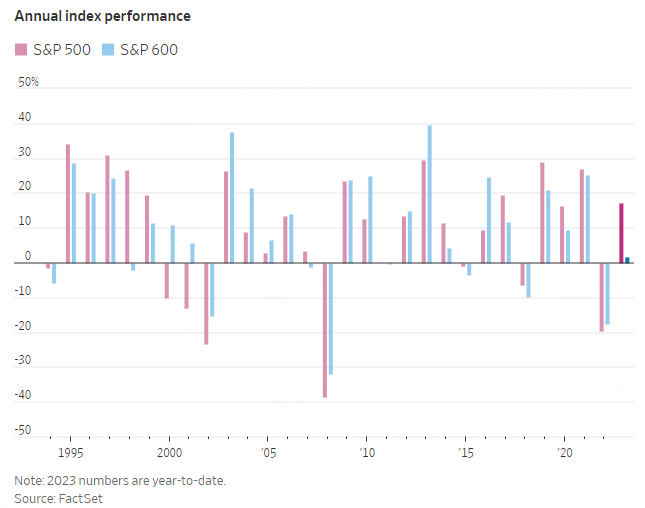

The S&P 600, an index of small companies with an average market value of $1.8 billion, has climbed 10% from its recent low on Oct. 27, slightly outpacing the S&P 500. Yet for 2023, it is on pace to trail its large-cap counterpart by the widest margin in a calendar year since 1998. The S&P 600 is up 1.7%, while the S&P 500 has climbed 17%.

The Federal Reserve's interest rate campaign has hurt small-caps more than their larger peers because small companies tend to issue more floating-rate debt. Their loan payments fluctuate with benchmark interest rates, so higher interest expenses are denting their bottom lines. Bigger companies are generally more insulated, after many rushed to lock in low fixed rates in 2020 and 2021.

About 40% of the companies in the S&P 600 have outstanding floating-rate debt with shorter maturities, compared with roughly 10% of companies in the S&P 500, according to the J.P. Morgan Equity Macro Research team.

Even if the central bank is done raising interest rates, small-caps likely won't see any relief from higher interest expenses until rates start falling. After that, there will be a lag because most of the floating-rate loans issued by public companies reset quarterly and are backward looking.

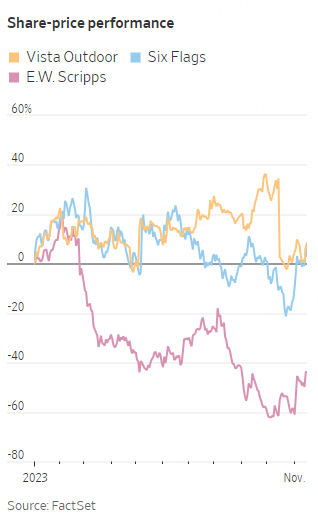

Television broadcaster E.W. Scripps, theme-park operator Six Flags Entertainment and Vista Outdoor, a sports and outdoor equipment maker, are among the companies whose interest expenses have surged even as their debt levels have decreased.

"It's really those smaller companies that lean on financing to help them run the business that the longer interest rates stay higher, the more stress it creates," said Anthony Saglimbene, chief market strategist at Ameriprise Financial.

Scripps said its interest expense jumped more than 35% in the third quarter from a year earlier due to higher rates on its variable debt borrowings, while long-term debt edged down. The company's $57 million in interest expense just exceeded its operating income, pushing Scripps to a net loss for the period. The stock is down 42% this year.

Six Flags' interest expense rose 12% in the third quarter from a year ago, even after paying down some of its floating rate debt, which totals nearly $500 million. Earlier this month, Six Flags unveiled plans to combine with fellow theme park operator Cedar Fair, sparking a rally in its stock. Shares are up 3.4% in 2023.

At Vista Outdoor, interest expense rose about 20% in the latest quarter despite long-term debt levels dropping about 30%. The company is selling off part of its business and intends to use the proceeds to pay down debt. Shares are up 7.3% this year.

Erik Knutzen, multiasset class chief investment officer at Neuberger Berman, said he is looking to pare back exposure to some small-caps with high financial and operational leverage, pointing to their widespread unprofitability and reputation for junk-rated debt.

"Bigger companies with more cash, better financial positions and in less operationally levered businesses -- more moats around their businesses -- will do better in that environment, that we expect," Knutzen said.

About 21% of the companies in the S&P 600 don't make money compared with 8% in the S&P 500, according to the J.P. Morgan analysts.

Much of the recent rally in small-caps and other stocks has been driven by bets that the Fed is done raising interest rates. Tuesday's cooler-than-expected inflation report for October reinforced those wagers. Traders in the derivatives market are now predicting rates will be nearly a full percentage point lower by the end of next year.

"If interest rates have peaked and start to head lower, then that could be supportive," said Mona Mahajan, senior investment strategist at Edward Jones.

For two years, investors have been hopeful that the Fed could successfully pull off a soft landing by cooling the economy without pushing it into a prolonged recession. If that mission is complete, then small-caps could be poised to keep rallying because their performance is closely tied to the health of the economy and they generate the majority of their sales domestically.

And small-caps still look cheap historically, even after their recent rally. The S&P 600 is trading at 13.7 times its projected earnings over the next 12 months, up from 11.2 times near the end of October, which marked one of its lowest levels of the year. Its five-year average is 14.5. The S&P 500, in comparison, carries a multiple of 17.

Comments