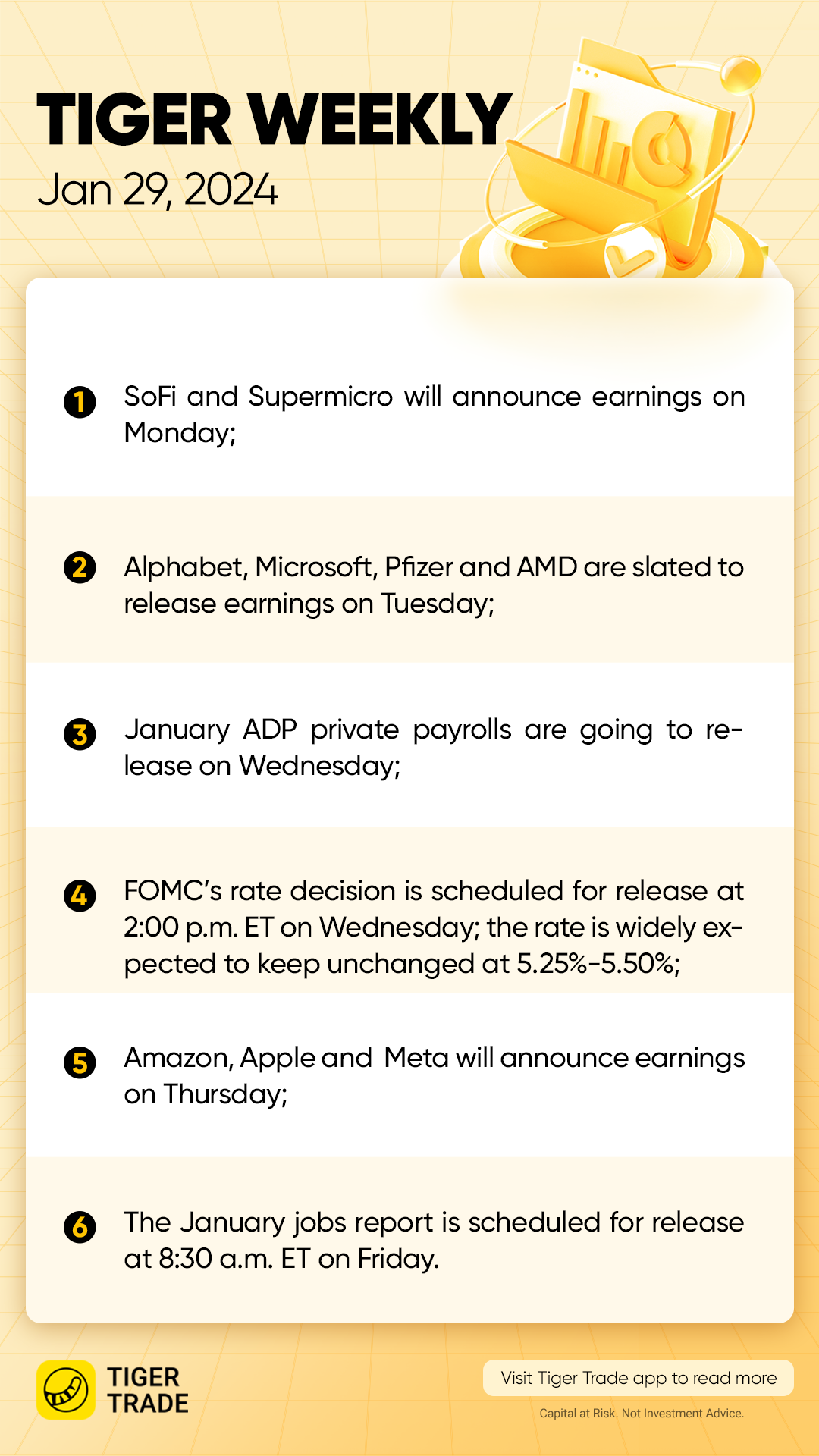

It will be a packed week on both the macro and micro fronts. There’s a Federal Reserve policy meeting, January jobs data, and earnings reports from around 100 S&P 500 firms to look forward to, including the biggest companies on the market.

The Federal Open Market Committee will announce a monetary policy decision on Wednesday afternoon, followed by a press conference with Fed Chairman Jerome Powell. Wall Street is forecasting no change in the federal-funds rate at this meeting, but it will be paying close attention to any clues about when the central bank might begin cutting interest rates in 2024.

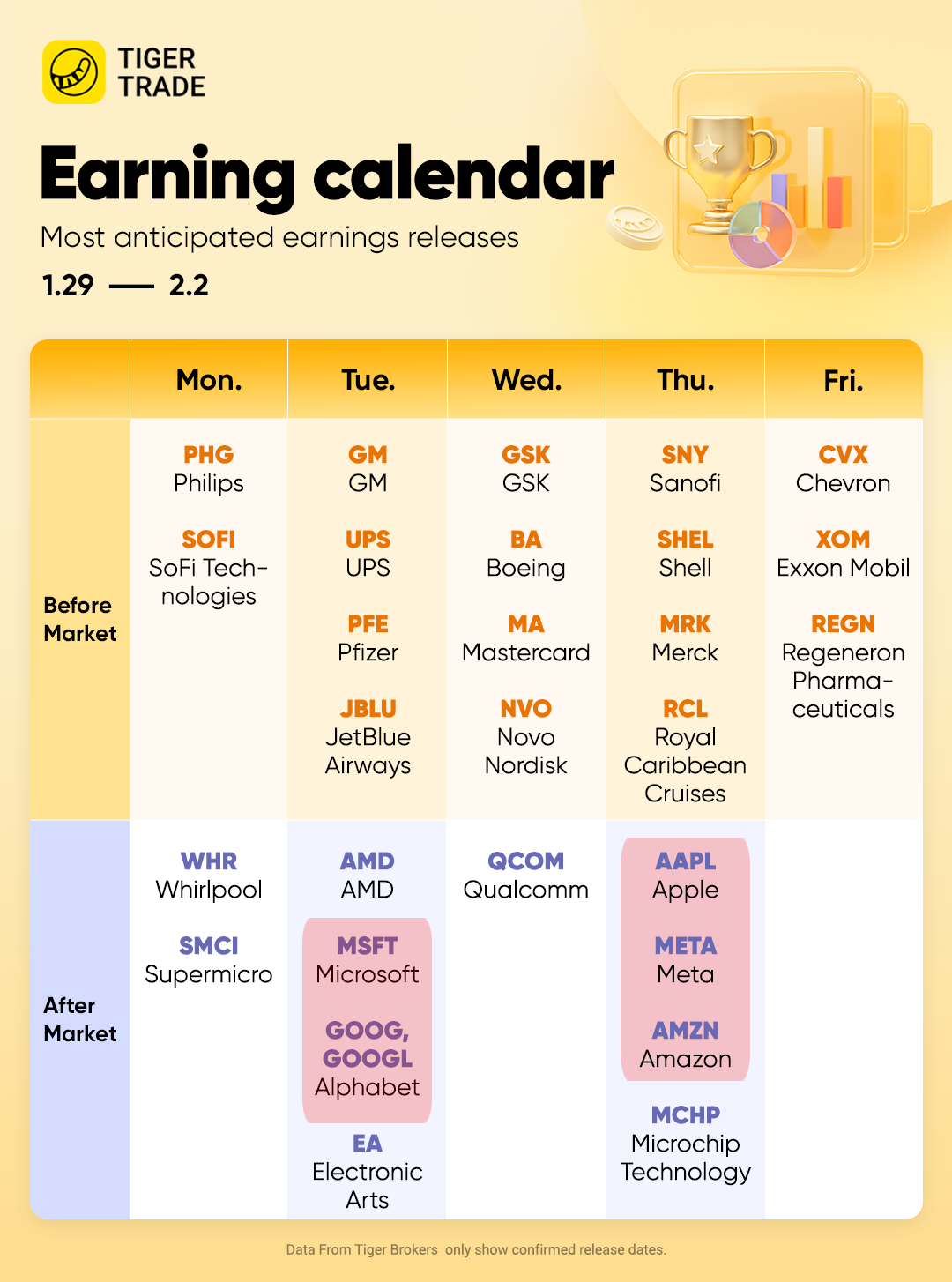

Fourth-quarter earnings reports this week will begin with Nucor on Monday, then Microsoft, Alphabet, Pfizer, General Motors, Starbucks, and Advanced Micro Devices on Tuesday.

On Wednesday, Qualcomm, Boeing, and Mastercard are scheduled to report, then Apple, Amazon. com, Meta Platforms, and Merck go on Thursday. Finally, Exxon Mobil, Chevron, and Bristol Myers Squibb release their results on Friday.

The economic data highlight of the week will be the January jobs report from the Bureau of Labor Statistics on Friday morning. Economists are expecting a gain of 175,000 nonfarm payrolls and an unemployment rate of 3.8%. On Tuesday, the BLS will report the Job Openings and Labor Turnover Survey. That’s expected to show 8.7 million job openings on the last business day of December.

Other data to watch this week includes the Conference Board’s Consumer Confidence Index for January and S&P CoreLogic’s Case-Shiller National Home Price index for November on Tuesday, plus the Institute for Supply Management’s Manufacturing Purchasing Managers’ Index for January on Thursday.

Monday 1/29

Alexandria Real Estate Equities, Franklin Resources, and Nucor release quarterly results.

Tuesday 1/30

Advanced Micro Devices, Alphabet, Danaher, Electronic Arts, General Motors, HCA Healthcare, Johnson Controls International, Marathon Petroleum, Match Group, Microsoft, Mondelez International, MSCI, Pfizer, Starbucks, Stryker, Sysco, and United Parcel Service report earnings.

The Bureau of Labor Statistics releases the Job Openings and Labor Turnover Survey. Economists forecast 8.7 million job openings on the last business day of December, slightly less than in November.

S&P CoreLogic releases its Case-Shiller National Home Price index for November. Home prices declined slightly year over year last April and May but price gains have accelerated since then culminating with a 4.8% increase in October. That trend is expected to continue with economists forecasting a 5.7% rise for the index.

The Conference Board releases its Consumer Confidence Index for January. Consensus estimate is for a 114 reading, about three points more than in December. Consumer sentiment as measured by the Conference Board and the University of Michigan has risen sharply in the past few months.

Wednesday 1/31

Automatic Data Processing, Boeing, Boston Scientific, Cencora, Corteva, GSK, Hess, Mastercard, MetLife, Nasdaq, Novartis, Novo Nordisk, Old Dominion Freight Line, Otis Worldwide, Phillips 66, Qualcomm, Rockwell Automation, Roper Technologies, and Thermo Fisher Scientific announce quarterly results.

The Federal Open Market Committee announces its monetary policy decision. The FOMC is widely expected to keep the federal-funds rate unchanged at 5.25%-5.50%. Wall Street will be listening intently to Powell’s postmeeting conference for signals about when the central bank might begin cutting interest rates. Despite strong GDP growth in 2023 and a tight labor market, traders are pricing in a 50% chance of a quarter-of-a-percentage point rate cut at the March FOMC meeting.

ADP releases its National Employment Report for January. Expectations are for the economy to add 145,000 private-sector jobs, 19,000 less than in December.

Thursday 2/1

Altria Group, Amazon, Apple, Atlassian, Becton Dickinson, Cardinal Health, Clorox, Eaton, Honeywell International, International Paper, Merck, Meta Platforms, Microchip Technology, Parker-Hannifin, Royal Caribbean Group, Sanofi, Shell, Tractor Supply, and Trane Technologies release earnings.

The Institute for Supply Management releases its Manufacturing Purchasing Managers’ Index for January. The consensus call is for a 47.3 reading, roughly even with the December data.

Friday 2/2

AbbVie, Aon, Bristol Myers Squibb, Cboe Global Markets, Charter Communications, Chevron, Cigna, Exxon Mobil, LyondellBasell Industries, Regeneron Pharmaceuticals, and W.W. Grainger hold conference calls to discuss quarterly results.

The Bureau of Labor Statistics releases the jobs report for January. Consensus estimate is for an increase of 175,000 in nonfarm payrolls, after a 216,000 gain in December. The unemployment rate is expected to tick up to 3.8% from 3.7%.

Comments