Chip maker’s AI momentum will depend on staying far enough ahead of competitors to keep pricing strong

Nvidia’s next trillion dollars is proving easier than the first. That doesn’t exactly put the ascendant chip maker on Easy Street.

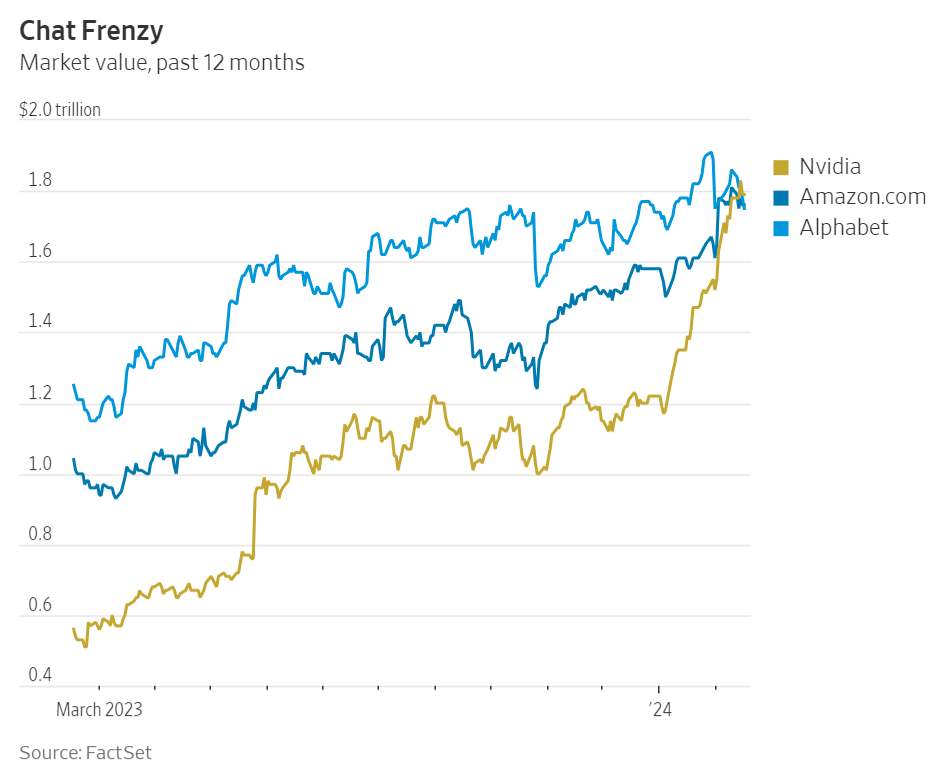

It became the first semiconductor company worth $1 trillion about eight months ago—not long after its 30th birthday. The stock’s momentum has continued; Nvidia is now worth just under $1.8 trillion and is the third most valuable U.S. company, after Microsoft and Apple.

It surpassed the market values of both Amazon.com and Google parent Alphabet last week, businesses with far more revenue that share two notable things in common—a vital need for Nvidia’s chips to power their growing ambitions in artificial intelligence and capital budgets of tens of billions of dollars annually to put toward the effort.

Just how many billions will become abundantly clear Wednesday, when Nvidia reports its fiscal fourth-quarter results. Based on the company’s forecast for the final quarter of the year, those results will show nearly $59 billion in revenue for the fiscal year ended in January—more than double what Nvidia generated in the previous year. None of Nvidia’s megacap tech peers—Apple, Microsoft, Amazon and the parent companies of Google and Facebook—ever expanded revenue that fast in a single year from a similar starting point, according to data from S&P Global Market Intelligence. Nvidia will become the world’s second-largest chip company based on annual revenue, surpassing Intel.

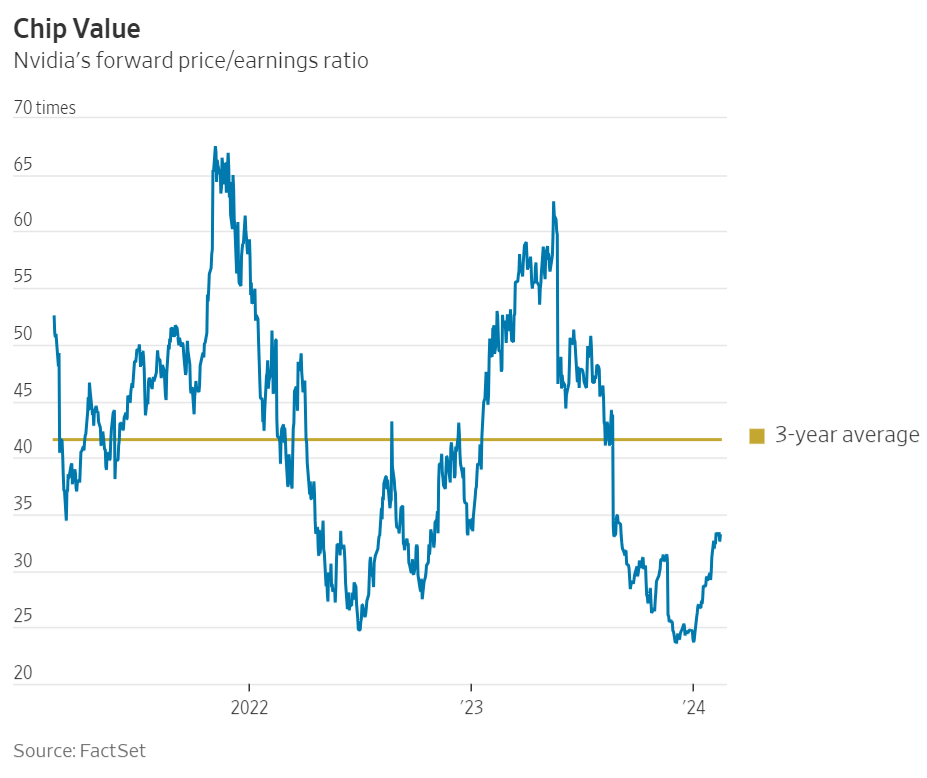

Such momentum explains why a chip company that drew most of its business from the niche market of gaming PCs less than five years ago is now approaching a market value of $2 trillion. Even in a market frothed by AI hype, that number isn’t as outlandish as it might seem. At that value, Nvidia’s stock would be trading around 38 times forward earnings—about 9% below its three-year average, according to data from FactSet. Seven of the 30 stocks on the PHLX Semiconductor Index currently carry higher multiples, including Advanced Micro Devices, which is challenging Nvidia for a piece of the lucrative market for AI chips in data centers.

Yet that meteoric rise—especially a jump of around 25% in the past month—naturally sets up risk heading into this week’s quarterly report. The current earnings season has already been rough on tech companies that posted less than perfect results following big run-ups. In a report Friday, Vivek Arya of BofA said he wouldn’t be surprised to see a “notable but brief pullback” on Nvidia’s shares following earnings, given the “mix of fear and greed and indiscriminate investor chase for all things AI” that has fed the stock’s sharp rise.

Even if Nvidia delivers a strong and well-received report, there is also the question of how long the boom can last. Investors are keenly focused on the question of how this year and next will shape up for AI chip demand, but Nvidia projects only one quarter at a time during its earnings reports. Wall Street is currently expecting the company to forecast revenue of $21.6 billion for the April quarter—a tripling compared with the same period last year.

Investors will still be listening closely for clues to longer-term trends. Analysts currently project revenue just under $92 billion for the current fiscal year ending in January 2025, a 56% jump from the just-ended fiscal year. More important clues might come next month during Nvidia’s GTC conference, its flagship event for AI developers. It could feature new details on the company’s next big AI system, called B100, which analysts expect to be launched later this year. In a report earlier this month, Morgan Stanley analyst Joseph Moore called the B100 “a strong advancement of state of the art” based on some early leaks about the system.

New products will be vital for Nvidia to address the growing competition and to maintain the earnings power that has kept its stock relatively cheap despite its huge run. BofA’s Arya thinks Nvidia will be able to price its coming B100 products at least 10% to 30% higher than the company’s current, highly popular H100 system.

“In our view, we are at-worst in middle innings of that upfront 3yr spending cycle, with demand likely stretching out to at-least mid-late CY25,” Arya wrote.

Tim Arcuri of UBS sees Nvidia’s per-share earnings hitting around $28 this year on the strength of its current chips that remain in tight supply plus new products like the B100. That is more than double what Wall Street estimates it earned during the just-ended year, but Arcuri wrote in a Feb. 12 note that demand keeps soaking up Nvidia’s chips even as production lead times “have come in substantially” over the past few months. He also boosted his price target on the stock to $850, which would put Nvidia’s market capitalization above $2 trillion.

The third-biggest tech stock has a big year ahead of it.

Comments