Kathrin Ziegler/DigitalVision via Getty Images

Introduction

YieldMax ETFs and I have a complicated relationship. It's mostly sour and entirely one-sided (they've never responded to anything I've written, but I'd love to chat!), but I recently gave their fund-of-funds ETF, YMAX, a positive rating.

This was the first positive rating they've earned from me, as the other four ETFs I reviewed earned sell ratings. Their Tesla covered call ETF was my first sell rating on Seeking Alpha. I will say, if you listened to me, it paid off. TSLY has not performed well at all since I posted the article.

Seeking Alpha

So when I came across the YieldMax Ultra Option Income Strategy ETF (NYSEARCA:ULTY), I was interested to see what set it apart from the single-stock themed funds. And what makes it "ultra"?

ULTY Overview

The YieldMax Ultra Option Income Strategy ETF is an actively managed ETF that employs covered-call strategies (that is, buying stock and then selling calls for income at the cost of price upside) on a number of individual names. They are chosen by the manager, and the methodology is opaque. So far, it's not necessarily impressed me.

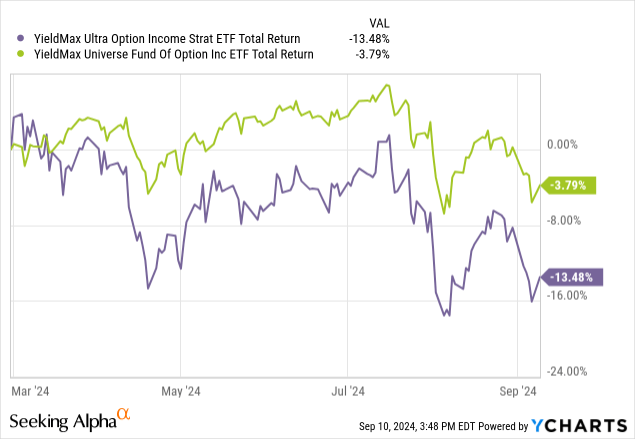

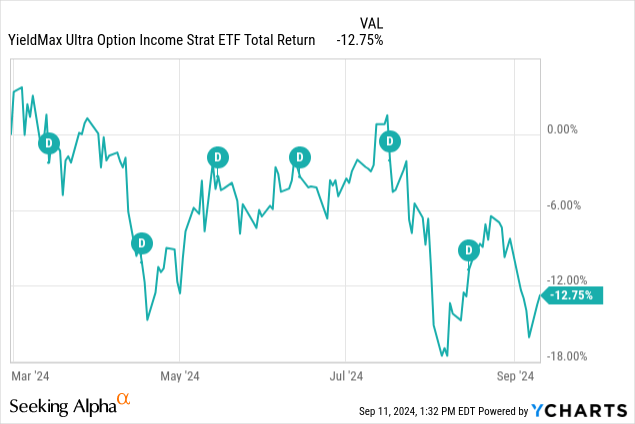

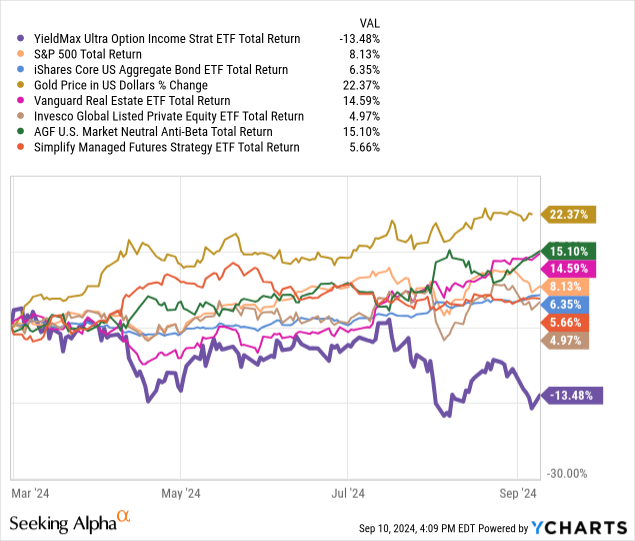

Compared to the fund-of-funds approach YMAX takes, ULTY showcases much more volatility and drawdown potential.

Against the backdrop of its sister fund, ULTY's performance looks bad, but not that bad.

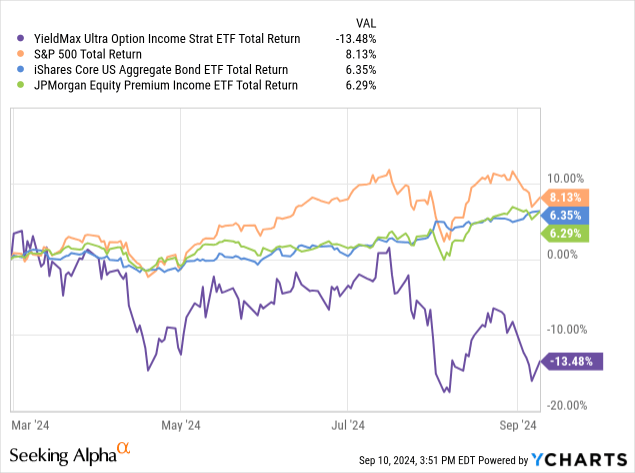

Compared to alternative investments shareholders could've made, it's horrific.

This underperformance is indicative of poor management. That is the only variable outside of the other funds. ULTY's downtrend is far outside the bounds of standard deviations for its strategy. Even a passive strategy with no manager strike picking or intraday trading is doing better than ULTY.

The Fund's Yield is "Ultra"

This is a term used by ETFs, usually to denote leverage. While ULTY itself is not a leveraged fund, it does hold some leverage (more on that in the next section). My understanding is that the "ultra" tag here is supposed to be in reference to the yield.

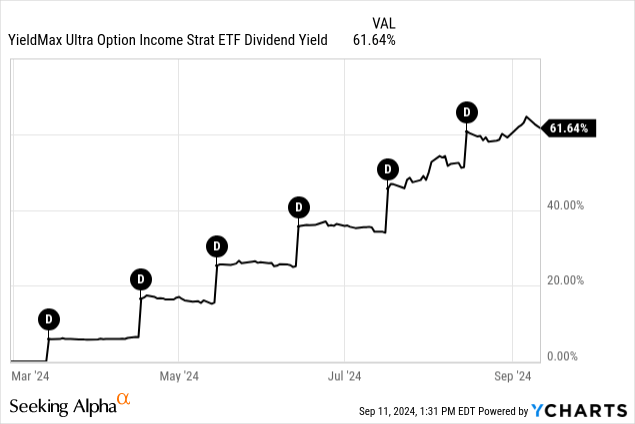

Note: The "D" symbols in the charts below represent distributions to shareholders.

In this instance, I will say that they are justified in using the term "ultra." 61% is a face-melting yield. The distributions have not made up for the NAV destruction, unfortunately, as shown by ULTY's negative lifetime total return.

Holdings

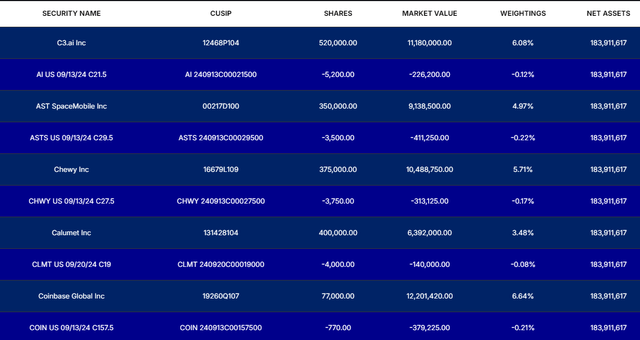

Here is the list of the largest long stock holdings and options as of the time of writing (9/11/24 @ 2pm EST). I want to timestamp that because ULTY trades intraday and could have exited any of these positions by the time this is published.

YieldMax ETFs

I am not a fan of any of the companies in its top holdings. They are largely unprofitable and overvalued. They were likely not chosen because of any fundamental reason, however. Instead, they were likely chosen because they had the best risk/reward ratio for selling covered calls.

That is not a stock picking methodology that I want informing my portfolio.

Garbage In, Garbage Out

This is a phrase that comes from computer science (correct me in the comments if that's wrong) where if you feed a computer bad data, it doesn't matter how good your program is, you will get bad results.

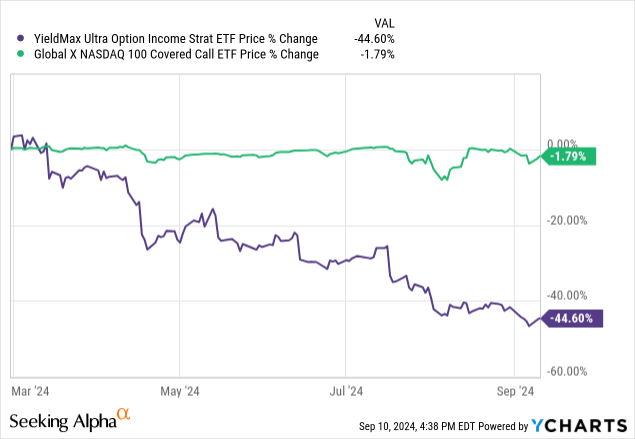

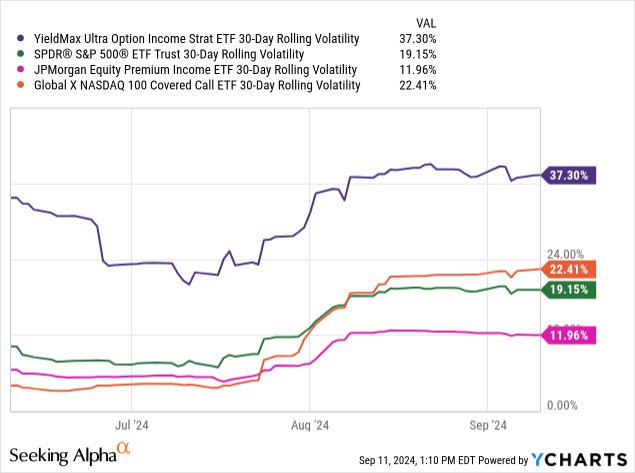

This is true for ULTY. By selecting the most volatile companies, which are largely those with no margin of safety, ULTY exposes itself to far more market risk than one might expect.

Lo and behold, it is far more volatility than competitors JEPI and QYLD.

Management's Playground

One of the major problems of the fund is that it is essentially an open canvas for the manager to make whatever trades they deem fit to make. There are no rules. Instead, management has full discretion on stock picking and strike picking, with no transparent game plan or strategy.

I'm not saying that YieldMax doesn't have a strategy they use. I'm saying that it is a secret, which makes it impossible for me to evaluate it.

As per the prospectus, the managers are free to trade any stock and selling at any strike they wish in order to achieve maximum income. This means that there is no set methodology, managers are free to trade intraday, meaning it's impossible to follow the funds in real time since holdings are only updated EoD, and the fund even gets to decide whether they have synthetic or real exposure.

The managers are able to decide which is more beneficial for the given situation, having to balance the Vega risk present in synthetic long positions with capital efficiency and liquidity.

The Fund holds a mix of direct long holdings of Underlying Securities and options contracts on Underlying Securities (considered indirect or synthetic long holdings of the Underlying Securities) to gain exposure to the share price performance of the Underlying Securities. The allocation between direct and indirect long holdings varies based on strategic decisions and market conditions as assessed by ZEGA. As the options contracts it holds are traded, exercised or expire, it may enter into new options contracts, a practice referred to as “rolling.” The Fund’s practice of rolling options may result in high portfolio turnover.

Losing Money For No Reason

If you want to lose money trading options, history tells us that ULTY may be just as bad as DIY traders. It managed to not only underperform basically all asset classes since its release, which is honestly very impressive.

If anyone can figure out how ULTY has lost so much compared to basically everything else, let me know in the comments section. It's hard for me to believe that this is all just bad timing and intraday losses and bad stock picks.

First Theory: Vega Risk

I have been droning on and on about Vega risk in YieldMax funds for some time now, since October last year. It's worse in the single-stock funds, since they are almost entirely synthetic long positions. ULTY does have some long stock positions, which may help it reduce volatility moving forward.

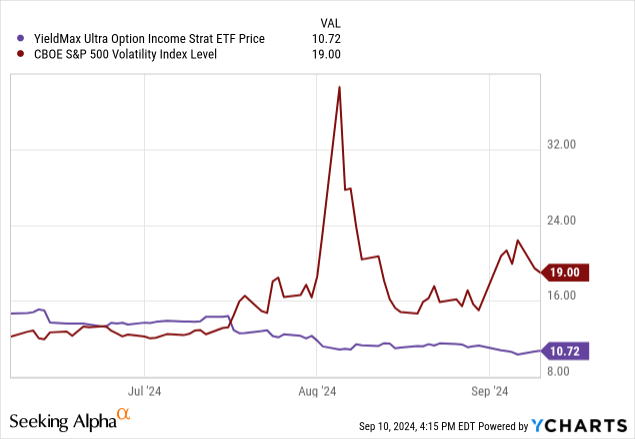

The drawdown that happened in August adversely affected markets generally, but the extreme nature of ULTY's drawdown has me believing that it suffered from too much Vega exposure as volatility suddenly ramped up.

The initial VIX jump in late July started the downtrend. I'm sure trying to manage the risk by trading without hedges has only made ULTY lock in and realize losses, causing its continued downfall even as the assets recovered.

Second Theory: Concentration Risk

As mentioned before, ULTY holds a few stocks in very high concentrations, 6%+ of AUM, which introduces significant market risk. Instead of spreading the options out so that no stock is more than 2% of the fund, as I might recommend for a covered call strategy designed to minimize risk and maximize reward, they are concentrated in a few choice names.

In total, ULTY owns only 13 stocks and 3 ETFs.

Stocks: AI, ASTS, CHWY, CLMY, COIN, ENPH, IOT, MSTR, NVDA, PLTR, RDFN, SAVA, UPST

ETFs: LABU, QQQ, TNA

Note that LABU and TNA are both 3x leveraged funds.

As far as I am aware, the leveraged positions shouldn't apply any additional leverage to the options. Instead, they just add illiquidity to the equation since these ETFs are traded far more thinly than the indices they replicate and leverage. This means that the manager is trying to juice up returns by including these leveraged positions, since they don't affect options pricing.

That is a very bad sign. In day trading circles, this might be called "revenge trading." This is when traders take on extra, unnecessary risk trying to make up for losses. ULTY has a lot of losses to make up for, and I wonder if adding in ETFs that are worse for options trading was done for a similar reason.

Conclusion

It's easy to say, "it performed poorly, and it will do so again," but that's how I feel about ULTY. It's risk profile is massive. Here are some of the major considerations investors need to make:

- Concentration in stocks that may be undesirable underlying holdings

- Opaque management makes forecasting performance impossible

- Elevated Vega risk via volatility exposure with no hedge

For these reasons, I have to give a sell rating to ULTY. I do not believe it has any place in an income portfolio or in a short volatility strategy. I recommend a 0% allocation to all investors.

Instead, I am still recommending short volatility exposure through Simplify's Volatility Premium ETF (SVOL). It does a fantastic job capturing that volatility, hedging it, and has matched the S&P 500 in performance since its launch. If you are interested in ULTY, you'll really like SVOL.

Thanks for reading.

Comments