travelpixpro

Thesis

The Nasdaq 100 Enhanced Options Income ETF (NASDAQ:QQQY) is a fairly new exchange-traded fund, having IPO-ed in September 2023. The name is part of a growing suite of products that aims to extract dividends from widely used indices via option structures:

QQQY aims to achieve consistent monthly yield distributions for investors coupled with equity market exposure to the Nasdaq-100. QQQY is an actively managed exchange-traded fund ("ETF") that seeks enhanced income, constructed of treasuries and Nasdaq-100 index options. The strategy's objective is to generate outsized monthly distributions by selling option premium on a daily basis. The fund uses daily options to realize rapid time decay by selling in the money puts.

Unlike other Nasdaq funds which use covered calls, QQQY uses cash covered puts as a strategy. The name is reminiscent of the S&P 500 WisdomTree PutWrite Strategy Fund ETF (PUTW) fund, which we covered here.

In today's article we are going to have an in-depth look at QQQY's build, its distribution and analytics, and articulate why we do not believe this is a robust name to use in monetizing the Nasdaq index.

What does QQQY actually do? Writing put options

Unlike covered call funds, QQQY does not purchase the Nasdaq index outright, but writes cash covered puts:

Holdings (Fund Website)

In the above table that presents the fund holdings as of September 11, 2024, we can see that the ETF parks its cash in treasury notes, all while writing cash covered puts on the Nasdaq. In this case, the fund wrote a put on the Nasdaq Index with a September 11, 2024, expiration date and a strike of 18,910. If the index is above that level on the close of business, the fund pockets the premium; otherwise it records a loss.

In a range bound or upward sloping market, the fund will realize gains via the premiums netted on the written put options. Conversely, in a down market, the ETF will realize losses as puts expire with the market lower than the strike level. Even in a down market, though, the fund will have a slight buffer to an outright position via the option premium embedded in the strategy.

In essence, just like PUTW, QQQY engages in a systematic put writing strategy on the Nasdaq Index.

Strategy total returns versus outright positioning

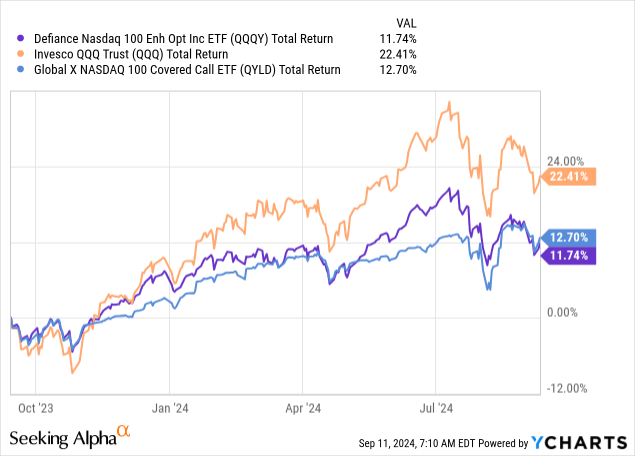

The ETF has a limited history, and we cannot show readers the fund's performance during a down market, but we can look at what the name has done in the past year since it was issued:

We are using a total return feature for our analysis since QQQY has a very high distribution rate (distribution which is going to be discussed in the next section). We are comparing the ETF to the Invesco QQQ Trust (QQQ) and the Global X Nasdaq 100 Covered Call ETF (QYLD).

QQQY has performed fairly in line with QYLD in the past year, having a total return of roughly 12% in that time-frame. The name exhibits a higher volatility when compared to QYLD, and was able to monetize a higher percentage of the upside in June-July 2024.

As with any option strategy, QQQY cannot replicate the entire upside exhibited by the Nasdaq, given its structure. The fund can only make the option premium it underwrites via the cash covered puts, thus rapid moves up by the Index are not mirrored. The ETF will thrive in a slowly up-sloping market, where the Index makes slow gains, thus allowing the fund to write a high number of puts and monetize them.

Unsupported distribution

What we do not like about this fund is its unsupported distribution that uses a marketing gimmick to garner attention:

Distribution Rate (Fund Website)

When a retail investor looks at the fund's website (or any third-party data provider for that matter), they will see an eye watering 105% distribution rate. That figure is not real, and most certainly does not tally up with the 12% total return recorded by the fund in the past year.

How can an ETF have a 105% distribution rate then if it does not make that money? The answer is 'return of capital' or 'ROC'. ROC is a very well-known concept in the CEF world, where funds use it to bridge cash mismatches or periods of time when underlying assets' returns do not match what it aims to disburse to investors. ETFs can have ROC as well:

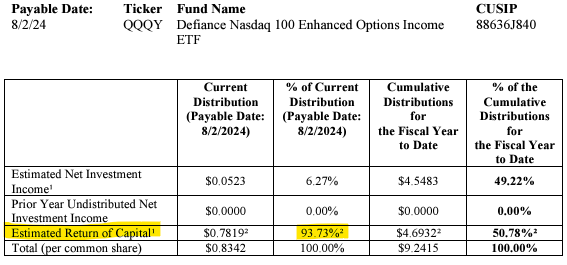

Section 19a (Fund Website)

If we look at the fund's 19a Notice for August 2024, we will notice that 93% of the distribution for that payment date is made up of return of capital. ROC simply means you are getting your money back. It is not an actual yield generated by the fund.

The ETF makes money in two ways only:

- interest from the U.S. Treasuries held

- put options premiums

When these two sources of income do not generate enough gains for a month, the fund simply uses investors' capital to make up the rest of the distribution payment. The net results of this tactic is an ever decreasing price for the fund.

We do not like this gimmick, and would much rather see the fund distribute what it makes, rather than target a high distribution rate to attract new capital into the name based on unsupported distribution rates.

What is next for this name?

Given its over-distribution feature, expect the price to keep moving lower, while the fund will have a high monthly distribution rate. The name will have a downside very similar to the Nasdaq, hence a hard landing scenario would see the name record significant losses. As an example, the Nasdaq was down -32% in 2022. If that scenario repeated itself, expect QQQY to be down in a similar fashion, but with a 5% to 7% buffer to account for the netted option premium. Thus, expect a rough -25% to -27% performance.

Conversely, in an up market the fund will record roughly half of the gains posted by the Index, very much determined by the speed of the up-move and the volatility associated with the macro scenario.

Conclusion

QQQY is an exchange-traded fund. The name aims to generate a high monthly income figure via writing puts on the Nasdaq index. While this systematic put writing strategy is valiant, its application in this case is not. QQQY uses a very high ROC figure to generate a high monthly distribution rate, a distribution which is not supported. The net result is an ever decreasing share price, and a 1-year total return which is only 12% versus a stated distribution rate of 105%. The fund has a similar performance to a covered call writing fund, with a similar downside to the index but a capped upside (roughly half of the index performance in the past year).

While we like the concept of a systematic put writing strategy on the Nasdaq, we do not like the implementation, and we would much rather see the fund decrease its distribution rate to eliminate all ROC, and only pay what it makes. Until the structuring of the name changes to adjust the distribution rate, we are assigning this fund a 'Sell' rating.

Comments