Richard Drury

The Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund (ETW) is a closed-end fund, or CEF, that investors can purchase as a method of earning a very high level of income from the assets in their portfolios. They can do so without needing to sacrifice the upside potential of an equity investment. This fund is quite similar to the Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV), which we discussed a few days ago. However, this fund is arguably a bit better at protecting the purchasing power of its investors’ wealth against the erosion caused by inflation. This is mostly because this fund can include foreign assets, which can actually benefit from a decline in the U.S. dollar against foreign currencies. This would have been helpful over the past year, as the U.S. Dollar Index (DXY), which measures the value of American currency units against a basket of foreign currencies, has declined by 3.04% over the past year:

Seeking Alpha

A domestic-only fund would not be able to take advantage of this, but a fund that invests its assets globally could exploit it as well. It could simply buy foreign assets that should see their returns boosted by a decline of the U.S. dollar against their home currency. Unfortunately, this fund has not been taking advantage of this opportunity to the extent that it could, and it has underperformed its domestic-only sister fund (ETV) over the past year:

Seeking Alpha

Nonetheless, there could still be a good case made for investing in foreign assets right now, and indeed many investors are actively seeking to diversify their assets globally. As such, it could be worthwhile to take a closer look at the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund today.

As is the case with most closed-end funds, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund boasts a very high yield today. At the time of writing, the fund yields 9.79%, which is a bit higher than its domestic-only version. The fund’s current yield also compares quite well with its peers, as clearly shown here:

Fund Name | Morningstar Classification | Current Yield |

Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund | Equity-Covered-Call Funds | 9.79% |

BlackRock Enhanced Capital and Income Fund (CII) | Equity-Covered-Call Funds | 6.30% |

Columbia Seligman Premium Technology Growth Fund (STK) | Equity-Covered-Call Funds | 5.98% |

First Trust Enhanced Equity Income Fund (FFA) | Equity-Covered-Call Funds | 7.17% |

Madison Covered Call and Equity Strategy Fund (MCN) | Equity-Covered-Call Funds | 9.81% |

Voya Global Advantage & Premium Opportunity Fund (IGA) | Equity-Covered-Call Funds | 10.97% |

As we can clearly see, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund has a yield that is slightly above the peer median of 8.45%. This is a pretty good place to be, as it provides strong confirmation from the market that the distribution is likely to be sustainable. Naturally, though, we still want to take a look at the fund’s finances to ensure that this is indeed the case. The fact that the fund’s yield is slightly below that of two of its peers might be a turn-off to some income-hungry investors, however.

As regular readers might remember, we previously discussed the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund in late June of this year. The global equity markets since that time have been fairly strong. This is partly due to a few central banks around the world instituting monetary easing programs in response to a weakening economy in those respective nations. In addition, there is an enormous amount of exuberance surrounding the development and deployment of generative artificial intelligence. These positive factors have, however, been tempered over the past week or so as recent economic data in the United States suggests that the economy might be in a recession or very close to it. As such, we can probably expect the fund’s performance to have been mixed since our last discussion.

This assumption is correct, as shares of the fund are down 1.57% since our last discussion:

Seeking Alpha

This is disappointing, but we can see that the S&P 500 Index (SP500) was down over the same period. Thus, it is difficult to get too upset here, as the fund did not underperform large-cap common stocks by very much. We do note though, that the fund’s share price was actually up through the end of August, so all the disappointment was caused by recession fears arising this month. September is historically the worst month for the S&P 500 Index and the market does decline more often than not during this month, so the poor performance so far this month is not unprecedented or unexpected.

It is worth noting though that investors in this fund actually did better than the price chart suggests. As I stated in my previous article on this fund:

A simple look at a closed-end fund’s price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

In the case of this fund, the distributions were able to fully offset all the share price weakness since our previous discussion. We can see that in this alternative chart that includes the impact of the distributions on the total return:

Seeking Alpha

Admittedly, this performance is nothing to write home about, as the fund was relatively flat over the past two-and-a-half months or so. Indeed, investors in this fund would have actually been better off in an ordinary money market fund. However, the fund did manage to outperform the market, and we can all respect that.

As roughly two-and-a-half months have passed since our last discussion, it would be logical to assume that a great many things have changed on a macroeconomic and fund-specific level. In particular, the fund released an updated financial report that we will want to pay close attention to when trying to determine how sustainable the distribution is likely to be. In addition, the United States is showing signs that the economy may be about to enter the recession that many have been predicting for a while now. This is something that could have a major impact on the performance of this fund in the near term. The remainder of this article will focus specifically on these changes and factors.

About The Fund

According to the fund’s website, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund has the primary objective of providing its investors with a very high level of current income and current gains. The current gains objective makes sense considering that this is an equity fund and capital gains are the primary way through which these securities deliver their investment return. However, equities are not generally good income vehicles, which we can clearly see by looking at the current yield of the various equity indices:

Index | TTM Yield |

Dow Jones Industrial Average (DJI) | 2.12% |

Dow Jones Transportation Average | 2.00% |

Dow Jones Utility Average Index | 3.12% |

Russell 2000 (IWM) | 1.51% |

NASDAQ-100 Index (QQQ) | 0.84% |

S&P 500 Index | 1.34% |

(Figures are from the Wall Street Journal.)

Some global indices do a bit better, but the major ones also have fairly low yields:

Index | TTM Yield |

MSCI World Index (URTH) | 1.54% |

MSCI All-Countries World Index (ACWI) | 1.69% |

MSCI All-Countries World ex-U.S. Index (ACWX) | 2.79% |

That the MSCI All Countries World ex-U.S. Index has a substantially higher yield than other global indices shows the yields of the markets of many individual countries outside the U.S. are higher than the domestic stock indices. For example, Singapore’s (EWS) common stock country index yields 4.30% right now. However, even those specialty and individual country indices have much lower yields than ordinary money market funds or most fixed-income assets. After all, the ten-year U.S. Treasury note yields 3.715% today, which is sufficient to beat domestic utilities in terms of yield.

The largest positions in the portfolio of the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund generally have lower yields than the common equity indices. Here are the largest positions in the fund:

Eaton Vance

Here are the yields of these companies:

Company Name | Current Yield |

Apple Inc. (AAPL) | 0.45% |

NVIDIA Corp. (NVDA) | 0.04% |

Microsoft Corp. (MSFT) | 0.75% |

Amazon.com (AMZN) | 0.00% |

ASML Holding (ASML) | 0.88% |

Meta Platforms (META) | 0.40% |

Nestlé SA (OTCPK:NSRGY) | 3.15% |

LVMH Moët Hennessy Louis Vuitton (OTCPK:LVMHF) | 1.75% |

Alphabet Inc. (GOOGL) (GOOG) | 0.53% |

Allianz (OTCPK:ALIZF) | 4.75% |

The current yields of Nestlé and Allianz are not too bad, but the remainder of the companies here all disappoint in terms of yield. Thus, the fund certainly is not attempting to generate much current income through dividends.

As is the case with most Eaton Vance funds, the website does not provide any insight into or information about the fund’s strategy. To get this information, we have to delve through the fund’s literature. Here is what the prospectus states about the fund’s strategy:

Under normal market conditions, the Fund’s investment program consists primarily of (1) owning a diversified portfolio of common stocks, a segment of which holds stocks of U.S. issuers and a segment of which holds stocks of non-U.S. issuers, and (2) selling on a continuous basis call options on broad-based domestic stock indices on at least 80% of the value of the U.S. Segment and call options on broad-based foreign country and/or regional stock indices on at least 80% of the value of the International Segment.

Under normal market conditions, the Fund invests at least 80% of its total assets in a diversified portfolio of common stocks of domestic and foreign issuers. The U.S. Segment is expected to represent approximately 50% to 60% of the value of the Fund’s stock portfolio and the International Segment is expected to represent approximately 40% to 50% of the Fund's stock portfolio. These percentages may vary significantly over time depending upon the Adviser’s evaluation of market circumstances and other factors. Under normal market conditions, the Fund invests a substantial portion of its total assets in the securities of non-U.S. issuers, including American Depositary Receipts, Global Depositary Receipts, and European Depositary Receipts. An issuer will be considered to be located outside of the United States if it is domiciled in, derives a significant portion of its revenue from, or its primary trading venue is outside the U.S. Securities of an issuer domiciled outside of the United States may trade in the form of depositary receipts. The Fund may invest up to 15% of its total assets in securities in emerging markets issuers.

For the U.S. Segment, the Fund intends to write index call options on the Standard & Poor’s 500 Index and the NASDAQ-100 Index. For the International Segment, the Fund intends to write index call options on broad-based foreign country and/or regional stock indices that the Adviser believes are collectively representative of the International Segment. Over time, the indices on which the Fund writes call options may vary as a result of changes in the availability and liquidity of various listed index options, the Adviser’s evaluation of equity market conditions and other factors. Due to tax considerations, the Fund intends to limit the overlap between its stock portfolio holdings and each index on which it has outstanding options positions to less than 70% of it is on an ongoing basis.

This strategy is very similar to, if not identical to, that of the Eaton Vance Tax-Managed Buy-Write Opportunities Fund that we discussed a few days ago. The difference is that this one has lower exposure to the United States and more exposure to foreign markets. It also will have a wider variety of indices upon which it can write call options. The fund’s largest positions list includes companies from the United States, the Netherlands (ASML Holding), Switzerland (Nestlé), France (LVMH Moët Hennessy Louis Vuitton), and Germany (Allianz). This suggests that the fund might be writing options against the S&P 500 Index, NASDAQ-100 Index, FTSE 100, the DAX, the FR40, the SMI, and possibly the NL25. After all, the fund’s description does state that it might write index options against regional indices like the FTSE 100 and single-country indices like the others. We do see some of these indices represented in the fund’s short options positions. The fund’s semi-annual report provides the following two charts of its short options positions as of June 30, 2024:

Fund Semi-Annual Report

Fund Semi-Annual Report

We see the NASDAQ-100, the S&P 500 Index, the FTSE 100, and the SMI Index as expected. We also see that the fund has written options against the Nikkei 225 Index, which might be surprising. After all, there were no Japanese countries listed among the fund’s largest positions. Nevertheless, the Nikkei 225 short options position is the largest individual short options position (collectively the American index options have a higher value) in the fund’s portfolio. It would be rather foolish for the fund to have this position if it did not own any Japanese stocks.

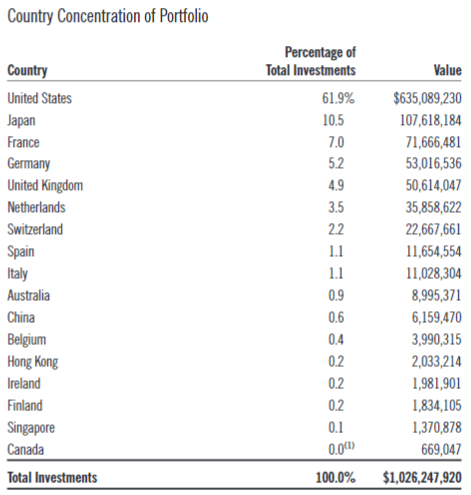

Fortunately, Japanese equities comprised the second-largest country position in the fund’s portfolio as of June 30, 2024:

Fund Semi-Annual Report

This is very surprising considering that there are no Japanese companies listed in the largest positions list. It can easily be explained if we simply consider that the fund is holding small positions in several Japanese companies. While the fund does not break down its holdings by country in its schedule of investments, a brief look at the fund’s holdings reveals SoftBank (OTCPK:SFTBY), Mitsubishi Corp. (OTCPK:MSBHF), Sumitomo Corp. (OTCPK:SSUMF), Tokyo Electron (OTCPK:TOELF), Kawasaki Heavy Industries (OTCPK:KWHIY), and other Japanese companies. Thus, the fund does have assets in every country whose market it has outstanding short options positions against. The key to the fund’s strategy is that it needs its holdings in each country to outperform the country index that it is writing options against to avoid losses. As I explained in my recent article on the Eaton Vance Tax-Managed Buy-Write Opportunities Fund:

This is necessary because the fund’s strategy of writing index options has one fundamental flaw from a risk-management perspective. This is that the fund is technically writing naked options, so if one of these indices increases very rapidly then the fund could potentially face unlimited losses. The fund will usually try to buy back the option in such a situation, but there is no guarantee that it will be able to. As long as the stocks in the portfolio appreciate more rapidly than the indices, though, then the realized and unrealized gains from the stocks should be able to offset any losses from the options strategy.

This is one of the reasons why this fund, and most of Eaton Vance’s other option-income closed-end funds, have high exposure to the “Magnificent 7” technology stocks. As I explained in my previous article on this fund, these stocks have been responsible for most of the S&P 500 Index’s total returns over the past two years. Thus, if the fund was holding anything else to represent the American markets, then it would have taken losses from the option-writing strategy.

In the introduction, I mentioned that this fund has an advantage over its sister fund in that it can earn gains from currency appreciation. In the fund’s largest positions list, we see companies whose native currencies are the U.S. dollar, the euro, and the Swiss franc. This has benefited the fund over the past year. As we can see here, the Swiss franc has appreciated 4.88% against the U.S. dollar over the past twelve months:

XE

The euro has appreciated 3.01% against the U.S. dollar over the same period:

XE

In both of these charts, a downward move means that the U.S. dollar weakened against the foreign currency and an upward move means that the U.S. dollar strengthened. As we can see, the overall trend has been for a declining U.S. dollar.

Even if the stocks that the fund holds from these countries do not change in price at all on their native exchanges, they will have appreciated a few hundred basis points in U.S. dollar terms. This provides this fund with a source of capital gains that its domestic peers do not have. In theory, it also might improve its ability to protect investors against inflation when compared to the Eaton Vance Tax-Managed Buy-Write Opportunities Fund because inflation, by definition, is a decline in the value of the currency. It is, admittedly, questionable whether foreign currencies can protect against inflation in the same way that gold can. This is because the European Union, Japan, and most other developed-market nations have the same structural problems that are driving the long-term decline of the U.S. dollar. However, the fact that the fund can benefit from currency fluctuations is still better than not having this ability, as is the case with its domestic-only peer.

Distribution Analysis

The primary objective of the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund is to provide its investors with a very high level of current income and current gains. It provides this by paying out a monthly distribution to its shareholders that serves as income for the investors. In the case of this fund, the monthly distribution is $0.0664 per share ($0.7968 per share annually). This gives the fund a reasonably attractive 9.79% yield at the current share price.

Unfortunately, this fund has not been especially consistent regarding its distribution over the years. We can see this lack of consistency here:

CEF Connect

As I stated in my previous article:

This is not something that will appeal to those investors who are seeking to earn a safe and consistent level of income that they can use to pay their bills or finance their lifestyles. This is particularly true today as inflation has steadily reduced the purchasing power of the fund’s distributions over the past two years, yet the fund has actually reduced its distribution.

We do, however, notice that this fund increased its distribution in April of 2024. However, the raised distribution of $0.0664 per share is still lower than the $0.0727 monthly distribution that the fund was paying out prior to the November 2022 cut. Thus, the previous paragraph’s comments about the fund’s distributions suffering from declining purchasing power remain valid. This is disappointing for those investors who are buried under the weight of inflation.

The most recent financial report for the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund is the semi-annual report for the six-month period that ended on June 30, 2024. A link to this report was provided earlier in this article. As this is a newer report than the one that we had available to us the last time that we discussed this fund, we should take a look at it to see how sustainable the fund’s distribution is.

For the six-month period that ended on June 30, 2024, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund received $13,070,708 in dividends and surprisingly no interest. The fund did have $3,937,354 of income from other sources though, but it does not specify exactly where this came from. In any case, this gives the fund a total investment income of $17,008,062 for the six-month period. The fund paid its expenses out of this amount, which left it with $11,452,688 available for shareholders. That was, unsurprisingly, insufficient to cover the $40,967,652 that the fund paid out in distributions over the period.

Fortunately, the fund was able to make up the difference through capital gains. For the six-month period, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund reported net realized gains totaling $18,462,102 along with $39,413,284 of net unrealized gains. Overall, the fund’s net assets increased by $28,360,422 after accounting for all inflows and outflows during the period.

We can clearly see that this fund had no trouble covering its distributions during the period, which explains why it increased the payout about halfway through the six-month period. This is generally a good sign, but we do notice that the fund was only able to fully cover its distributions due to a high level of net unrealized gains. If the recent market weakness continues (due to a recession, perhaps) then the fund’s distribution coverage may not be as good as it seems. Investors would be wise to watch the fund’s net asset value over the remainder of this year.

Valuation

Shares of the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund are currently trading at a 10.05% discount on net asset value. This is not as good as the 11.62% discount that this fund’s shares have had on average over the past month, so it might be possible to get a better entry price by waiting for a short while. However, a double-digit discount typically represents a decent entry point for any fund, so the current price is probably fine for purchasing shares.

Conclusion

In conclusion, the Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund provides its investors with a high level of current income as well as exposure to foreign markets. The fact that this fund has exposure to foreign markets and foreign currencies might allow it to protect against inflation a bit better than its sister fund, the Eaton Vance Tax-Managed Buy-Write Opportunities Fund.

There are signs that the United States may be about to head into a recession, and that might drive stock prices down. If that proves to be the case, this fund’s option-writing strategy should help cushion the blow somewhat. The fund also managed to cover its distribution fully during the first half of the year, and trades at an enormous discount to net asset value. Overall, this fund continues to look like a decent option-income fund.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments