Luis Alvarez

Introduction

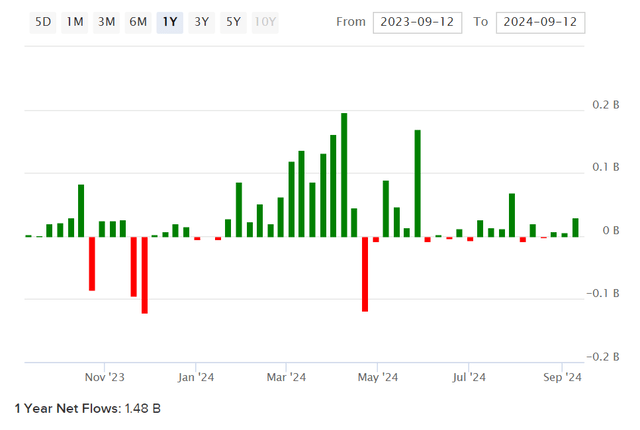

Global X U.S. Infrastructure Development ETF (BATS:PAVE) is an exchange-traded fund which invests in companies involved in the production of raw materials, heavy equipment, engineering, and construction, whereas those companies will likely benefit from increased industrial and infrastructural activity in the United States. The expense ratio is 0.47%, while assets under management were $7.88 billion as of September 13, 2024, per data from Global X ETFs (the ETF manager for PAVE). This follows positive net fund flows of about $1.48 billion over the past year.

ETFDB.com

PAVE is a somewhat young ETF; it was set up in 2017. Still, the fund is quite large already, and has gained in popularity, which we could possibly take as a signal that participants are betting on increased infrastructure spending. Obviously 2024 is an election year, and it won't be until early November 2024 until we know whether the next executive branch will be run by the Democratic or Republican Party.

Context

We do know, however, that the Infrastructure Investment and Jobs Act, or IIJA, of 2021, will spur construction activity through 2026 (aimed at expanding public roads, EV infrastructure, broadband, and water systems), while the CHIPS Act boosting semiconductor manufacturing spend (particularly in 2024/25, with plant construction projects starts). The Inflation Reduction Act (or IRA) has also helped generate around $88 billion of investment under close to 200 new clean technology manufacturing facilities, which are anticipated to produce over 75,000 new jobs.

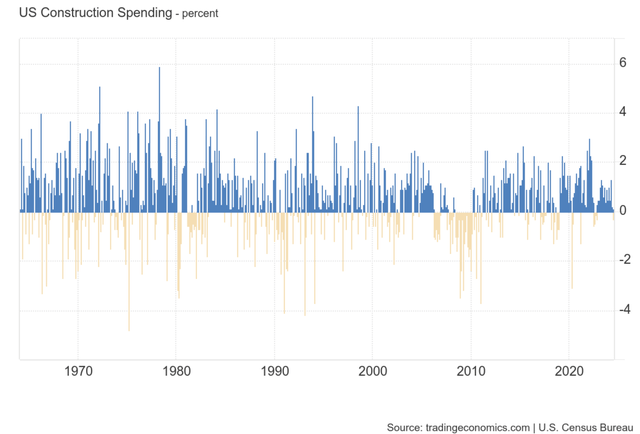

Meanwhile, a simple view of month-over-month construction spending in the United States, as shown below, is proof enough that even if there are down-cycles and recessions that lead to a reduction in construction spend (2008/09 being a more extreme past situation), one can probably expect a reasonably strong long-term growth rate of at least 2% (if not higher).

TradingEconomics.com

Even without ambitious government spending, the U.S. of course needs to maintain its present infrastructure, and so the sector as a whole (at least at an aggregate level) is somewhat of a cash cow. Only some cyclicality and uncertainty as to government policy has led the ETF to behave with an elevated beta of about 1.30x.

Current Earnings Expectations

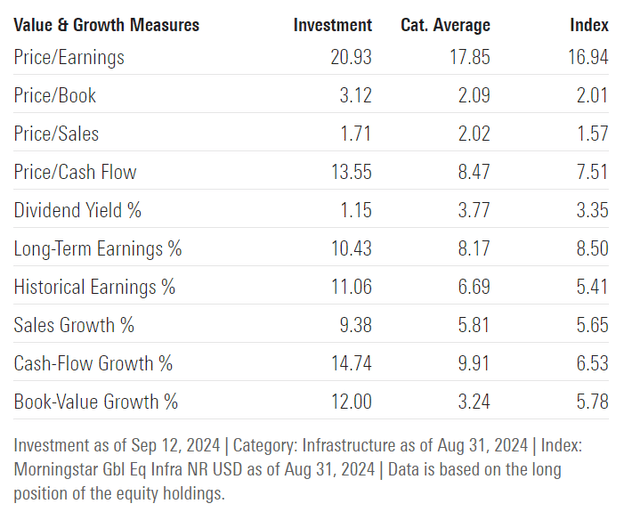

The PAVE ETF is, as reported by Morningstar, expected to generate a three- to five-year average earnings growth rate of 10.43%. Bear in mind historically over 11% has been achievable over the past five years, meanwhile Morningstar's projection of price/earnings (of 20.93x) can be used as a denominator on price/book (of 3.12x) to find a forward return on equity of 14.90% (projected), which is moderately high.

Morningstar.com

A risk to this kind of outlook would be a contraction in spend post election, though this is unlikely considering that the Federal Reserve is now signalling for lower rates (rates are currently in restrictive territory in the U.S.), which is likely to send longer-term yields lower as the economy continues to cool. Since bonds are likely to rise modestly from hereonin, and as the U.S. moves into the next business cycle, the next five years or so is likely to tilt in favor of increased infrastructure spend, albeit perhaps not aggressively. The backdrop, in my view, is cautiously positive, with no obvious reasons for a significant contraction in supply-side spend. That is not to say that increased taxation may be required, no matter the party in office. Increased protectionism would also be unsurprising, but this could in fact benefit U.S.-listed names in PAVE.

Overview of Holdings

PAVE has 99 holdings, as of September 12, 2024. The 30-day SEC yield (an approximate dividend yield rate) was 0.64%. There is low concentration across the portfolio, with the top holding representing 3.3% of the fund. The top 10 exposures seem representative of the broader portfolio's theme; they include industrial companies, infrastructural companies, and utility sector entities, providing services and solutions in areas like equipment manufacturing, energy, construction, aerospace, and materials.

GlobalXETFs.com

These are the kinds of companies that are almost certainly going to "be here tomorrow", the only question is whether, within the bounds of reasonable expectations, the valuation makes sense. Further, does the valuation compensate for risk, including somewhat elevated beta?

Valuation

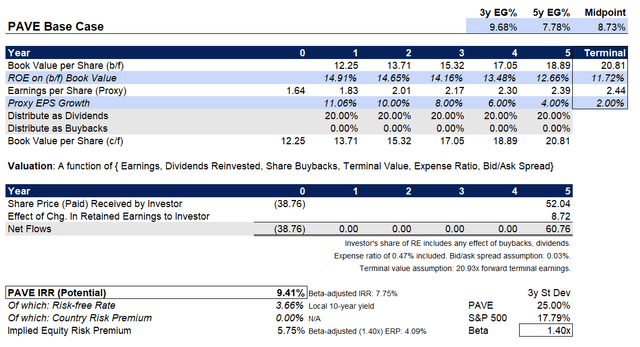

Based on the Morningstar data above, to be used as a starting point, I will assume that the portfolio's underlying return on equity matures to a lower rate of sub-12% by year six, which translates into a sub-consensus three- to five-year earnings growth rate of 7.8-9.7% (below Morningstar's reported 10.43%). This is perhaps a little conservative, but working with this assumption, and holding the dividend rate at about 20% of earnings, and assuming those dividends are reinvested over five years, the implied IRR is 9.41% (see below).

Author's Calculations

This suggests that PAVE offers a reasonably good annual return. However, note my own calculation of beta on a three-year basis is slightly higher than Yahoo! Finance's (I use the most recent data on a monthly basis, over three years). So, the underlying equity risk premium, adjusted for beta, is 4.09%. This is between the 3.2-5.5% sweet spot I think about for mature equities (including U.S. equities), once volatility/risk is adequately adjusted for. To me, then, PAVE offers decent value, but I have covered other ETFs recently with similar headline IRRs and lower nominal betas, so I see little reason to be especially bullish on PAVE at this juncture, especially given the uncertainty of the election.

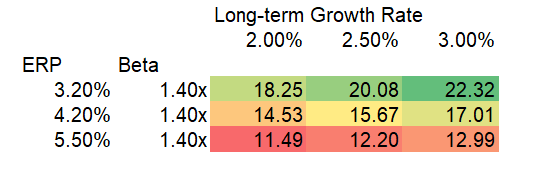

Also, another risk is the price/earnings ratio. I do not see PAVE having any kind of super-long-term, sustainable advantage as to earnings growth, since PAVE's portfolio is going to struggle to out-strip the growth of infrastructural trends. Therefore, in five years' time, you might think with a 10-year of say 3% and a terminal growth rate of 2%, the existing portfolio at a 1.4x beta might attract a price/earnings ratio of 12-18x or so. This is simply based on an approximation along the lines of '1 divided by the sum of 3% plus the risk-adjusted equity risk premium minus the long-term growth rate of 2%).

Author's Calculations

The current forward price/earnings multiple of about 20.93x is therefore not particularly conservative, if we were to hold that into our final year in our projections. Doing so would essentially assume either a reduction in long-term volatility (or beta), which is possible, but otherwise a low non-beta-adjusted equity risk premium, and a steady (likely above-inflation) growth rate into perpetuity. If we instead chose a price/earnings ratio of 18x in year five, before we exit the investment, the PAVE headline IRR would fall from 9.41% to just 6.71%, with a beta-adjusted ERP of only 2.17%, which would signal over-valuation at present.

I would not take a bearish view on PAVE, as the portfolio may well consider to grow and not mature for more than five years. However, as I would prefer to take a more conservative view of things, I see risks to the valuation in the longer run, and therefore it is not a long-term hold for me. There is certainly a possibility of a kick higher in the short term once election uncertainty resolves, but otherwise, I think there are likely better opportunities available at present.

Comments