Powell Industries, Inc. POWL shares have surged 89.9% in the past six months, outpacing the Industrial Products sector and the S&P 500, which have returned 5.5% and 8.2%, respectively. The company has also outshined the industry's decline of 1.7%, and its peers ESCO Technologies Inc. ESE and Schneider Electric S.E.'s SBGSY gains of 11.3% and 7.2%, respectively, over the same time frame.

POWL Outperforms Industry, Sector & S&P 500

Image Source: Zacks Investment Research

Closing at $261.34 in the last trading session, the stock is trading below its 52-week high of $364.98 but significantly higher than its 52-week low of $76.29. The electrical equipment manufacturer’s impressive performance can be largely attributed to its strong foothold and improving conditions in oil and gas and petrochemical markets.

A solid pipeline of projects within the LNG market and its growing presence across the data center and electric utility sectors, along with a solid backlog, are key catalysts behind the company’s growth. POWL’s efforts to expand its presence beyond the oil, gas and petrochemical markets have also enhanced its market share across the utility, commercial and other industrial markets.

Factors Driving the Stock

Powell is witnessing robust momentum in its oil and gas and petrochemical markets, which grew 23% and 112% year over year in the fourth-quarter fiscal 2024 (ended September 2024), respectively. Several favorable trends including growth in energy transition projects, such as biofuels, carbon capture and hydrogen, hold promise for the company’s long-term growth. Significant project awards supported by high investments in LNG, related gas processing and petrochemical processes have set POWL apart as a leading supplier of critical electrical infrastructure.

Increasing demand for electrical power from data centers is also creating a new opportunity for growth for this company. Powell is strengthening its participation across the electrical power value chain and benefiting from momentum in the data center and utility end markets. Notably, it witnessed strong bookings in the electric utility and commercial markets in the first nine months of fiscal 2024 in the United States.

Courtesy of solid bookings, the company’s backlog level increased to $1.3 billion (exiting the fiscal fourth quarter). Although new orders declined on a sequential basis, the metric totaled $267 million compared with $171 million in the year-ago quarter. Importantly, POWL’s new orders consisted of a healthy volume of small and medium-sized awards, which reflect its core competencies and well-balanced portfolio across diversified markets.

The company also plans to spend about $11 million as part of its facility expansion project at the Houston product factory. The expansionary efforts will help Powell execute its current backlog and enhance its customer offerings across data centers, hydrogen, carbon capture and other transitional energy markets.

Powell’s efforts to reward its shareholders also add to its appeal. In fiscal 2024, the company paid dividends of $12.7 million, increasing 2.4% year over year. In second-quarter fiscal 2024, it hiked its quarterly dividend by approximately 1%. The company’s strong liquidity position supports its shareholder-friendly activities. Exiting fiscal 2024, Powell had cash equivalents and short-term investments of $358.4 million compared with $279 million at the end of fiscal 2023 (ended September 2023).

Amid this, the Zacks Consensus Estimate for POWL’s fiscal 2025 (ending September 2025) revenues is pegged at $1.1 billion, indicating 9.3% year-over-year growth. The consensus estimate for first-quarter fiscal 2025 (ended December 2024, results awaited) revenues is $244.2 million, indicating year-over-year growth of 25.9%.

Better-Than-Industry Returns

POWL’s trailing 12-month return on equity (ROE) is indicative of its growth potential. ROE for the trailing 12 months is 35.68%, much higher than the industry’s 10.24%, reflecting the company’s efficient usage of shareholders’ funds.

Image Source: Zacks Investment Research

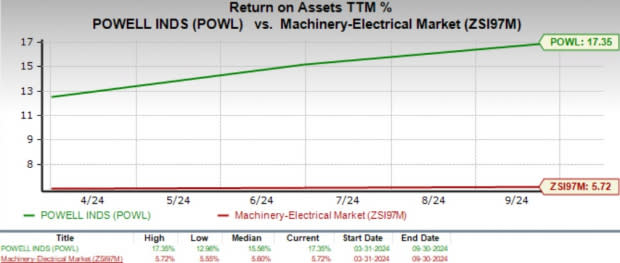

Return on Assets is 17.35%, ahead of the industry’s 5.72%, indicating that the company has been utilizing its assets efficiently to generate returns.

Image Source: Zacks Investment Research

POWL’s Valuation

With a forward 12-month price-to-earnings ratio of 18.62X, which is well below the industry average of 25.20X, POWL stock presents an attractive valuation for investors. However, the stock is trading higher than its peer, EnerSys ENS, which is trading at 10.03X.

Price to Earnings (Forward 12 Months)

Image Source: Zacks Investment Research

Northbound Earnings Estimates

Earnings estimates for fiscal 2025 have increased 10.1% to $13.70 per share over the past 60 days, while estimates for first-quarter fiscal 2025 have improved 5.1% to $2.83. The figures indicate year-over-year growth of 11.5% and 42.9% for fiscal 2025 and first-quarter fiscal 2025, respectively.

Find the latest earnings estimates and surprises on Zacks Earnings Calendar.

Image Source: Zacks Investment Research

Should You Buy POWL Now?

Solid momentum across its end markets, robust backlog level, portfolio diversification and capacity expansion efforts position Powell favorably for strong growth in the quarters ahead.

POWL is well-positioned to deliver sustained growth and shareholders’ value with a favorable valuation compared with the industry and strong earnings projections. We believe that the POWL stock is an ideal addition to investors' portfolios. The company currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ESCO Technologies Inc. (ESE) : Free Stock Analysis Report

Schneider Electric SE (SBGSY) : Free Stock Analysis Report

Enersys (ENS) : Free Stock Analysis Report

Powell Industries, Inc. (POWL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

Comments