-

This company suffered during rising inflation a few years ago but took steps that could help it beat the next similar challenge.

-

Its 2024 revenue soared in the double digits, and net income almost doubled.

Growth stocks benefit the most when the economy is thriving and the general environment is positive for expansion and spending. But when uncertainty arises, they often are the first to suffer.

That's what's been happening recently. President Donald Trump's tariffs on imports have stirred up concerns about higher prices in the U.S. and how that could hurt corporate earnings and consumer spending. As a result, some investors have shifted out of growth stocks since any economic headwinds could weigh on these companies.

That's pushed the Nasdaq Composite (^IXIC 2.27%) into correction territory and left many of its star stocks trading at dirt cheap valuations, which is the silver lining in the current dark cloud. At times of market uncertainty, investors can get in on quality growth companies that are well-positioned to excel over the long term for a song.

Below, I'll check out one of these stocks, which is down 12% over the past three months, to buy right now.

Image source: Getty Images.

A company you may know well

You're likely very familiar with this company -- you may even be in contact with it on a daily basis for everything from groceries to entertainment. I'm talking about e-commerce giant Amazon (AMZN 3.58%). The company sells a vast selection of mass merchandise, offers members of its Prime subscription program entertainment packages including sports and movies, and offers essentials such as food, cleaning products, and other items you'll buy during any market environment.

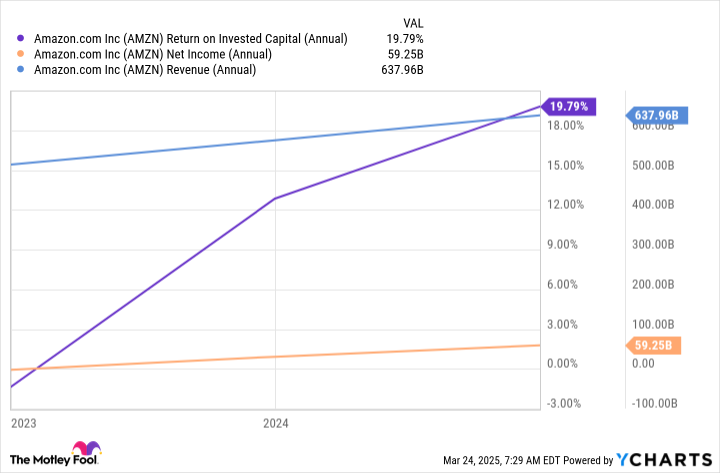

All of this has helped Amazon build a rock-solid earnings track record, generating billions of dollars quarter after quarter and delivering growing return on invested capital. This is an important metric because it shows that Amazon is benefiting from that spending because it's a big investor in its e-commerce and cloud computing businesses.

AMZN Return on Invested Capital (Annual) data by YCharts.

Today, Amazon's stock is unsurprisingly in the doldrums. Investors are concerned that any potential increase in prices due to the Trump administration's tariffs on goods from various countries could result in higher operating costs for Amazon. And on top of that, rising prices could leave consumers with less money to spend on discretionary items on the e-commerce site.

Addressing the cost structure

Here's why investors should consider setting those worries aside and buying Amazon on the dip. It's true that higher prices were painful for the e-commerce giant a few years ago as inflation surged, but Amazon did one key thing that should pump up its ability to handle any similar challenge moving forward: It overhauled its cost structure, a move that helped it recover from difficult times, and went from an annual loss in 2022 to net income in the following year.

This move also helped Amazon grow in recent times. For example, last year, revenue rose 11% to $638 billion, and net income almost doubled to $59 billion. If tariffs or other elements represent headwinds in the coming months, some of these efforts should significantly limit the impact. For example, Amazon is using artificial intelligence (AI) to streamline operations in fulfillment centers.

In addition, instead of shipping inventory from one part of the country to another, the company now placed inventory closer to its final destination. These decisions help decrease its cost to serve, meaning that even in a challenging environment, it will have more control over expenses.

A business that's proven its strength

It's important to remember that Amazon Web Services (AWS), the cloud computing unit, held up well during the period of higher inflation a few years ago. Customers may not have had as much to spend but stuck with AWS, and revenue growth continued quarter after quarter. In the coming quarters, as customers aim to build out their AI platforms, they may prioritize spending in this area, and that could work to AWS' advantage. The business sells a variety of AI products and services that have boosted revenue over the past couple of years. Just last year, AWS reached a $115 billion annual revenue run rate.

Considering all of this, Amazon stock currently looks very reasonably priced at 30x forward earnings estimates, down from more than 50x forward earnings a little over a year ago. That offers you a fantastic entry point.

Of course, any economic troubles could represent a headwind in the weeks or months to come, but thanks to Amazon's new cost structure and diversification across e-commerce and cloud, the impact on earnings should be limited. That's one positive point.

The second positive point is that these solid businesses, established over time, have what it takes to continue growing over the long run. That means current headwinds may be nothing more than a few bumps along the road.

Comments