KeyCorp (NYSE:KEY) recently announced a $1 billion share buyback plan, reflecting its confidence in financial health and a strategy to enhance shareholder value. Despite this, the company's share price fell 14% over the past month. This decline was influenced by broader market volatility, as major indices like the Dow and S&P 500 faced sharp losses due to increased tariff threats, raising recession fears. The challenging macroeconomic backdrop may have overshadowed KeyCorp's buyback news, aligning its performance with wider market trends rather than firm-specific actions.

We've discovered 2 risks for KeyCorp that you should be aware of before investing here.

AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

KeyCorp's recent announcement of a $1 billion share buyback plan could potentially bolster investor confidence, aligning with its broader strategies of improving financial health. Over the past five years, KeyCorp's total return, including dividends, reached 43.61%, indicating strong performance despite short-term volatility. However, in the past year, the company underperformed the US Banks industry, suggesting it has faced significant challenges in a competitive landscape.

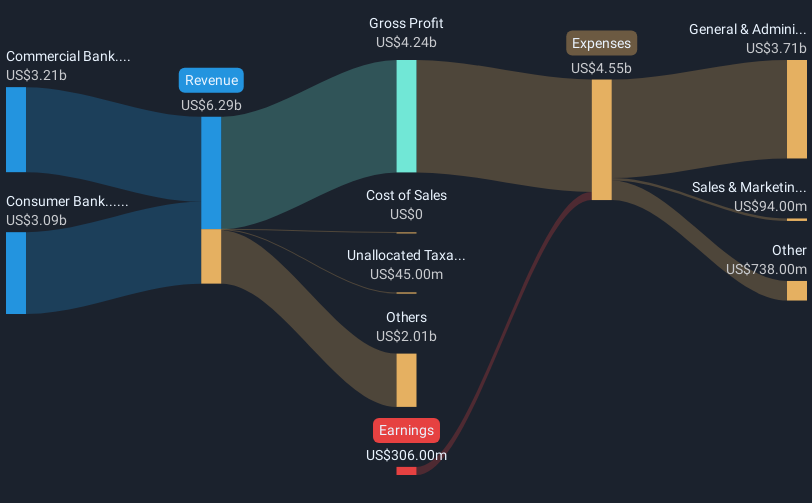

Despite the share buyback announcement, revenue growth and earnings forecasts remain critical. Analysts expect revenue to increase 10.5% annually over the next three years, potentially improved by strategic shifts in deposit cost management and an expansion in noninterest income streams like wealth management and commercial payments. Earnings are forecasted to rise to US$2.4 billion by October 2027, driven by shifts in net interest income dynamics.

In terms of valuation, the recent price movement has left KeyCorp's shares trading at a discount to the analysts' consensus price target of US$19.86. Although the current share price is US$17.49, which is 12% lower than the price target, the projected earnings growth could justify a shift towards this valuation. Still, the declining asset quality and other market risks may pose challenges to achieving these forecasts. Investors should therefore consider these factors when evaluating the company's future prospects.

Our expertly prepared valuation report KeyCorp implies its share price may be lower than expected.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KeyCorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Comments