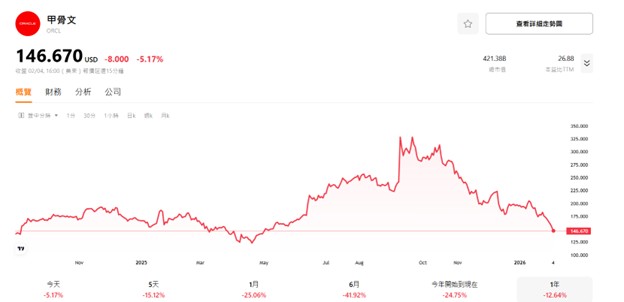

Oracle Corporation's stock has experienced a dramatic decline, falling more than 50% from its peak in September 2025.

Source: TradingKey

This sharp drop erased roughly $463 billion in market value from the record high reached after the optimistic earnings report in September that highlighted surging demand for its cloud services tied to artificial intelligence. The slide reflects growing investor concerns over the sustainability of Oracle's aggressive push into AI infrastructure, particularly amid mounting financial pressures that have transformed the company from a reliable cash generator into one grappling with significant balance sheet strain.

Financial Strains

The core issues stem from Oracle's deteriorating cash position and elevated debt load. In the most recent period, the company's free cash flow turned deeply negative, reaching approximately -$13.1 billion on a trailing basis, a stark reversal from the positive $9.5 billion recorded a year earlier. This shift has been driven by massive capital expenditures required to build out data centers and secure computing capacity for AI workloads.

A very related problem is Oracle's total debt, which has ballooned to around $108 billion, resulting in a high debt-to-equity ratio of 3.28x. Such leverage levels are unusual for a mature technology firm and have raised alarms about long-term financial stability.

Market signals underscore these worries. Oracle's credit default swap (CDS) spreads have widened to historically elevated levels, surpassing previous highs and implying a significantly increased perceived risk of default. Investors are evidently willing to pay substantial premiums for protection against the possibility that Oracle might struggle to meet its obligations, reflecting broader skepticism about the company's ability to navigate its current trajectory without severe consequences.

Source: Bloomberg

In response to these liquidity challenges, Oracle has taken desperate measures to shore up its finances. The company recently announced plans to raise between $45 billion and $50 billion in 2026 through a mix of debt and equity financing to support further cloud infrastructure expansion. A significant portion of this is expected to come from equity issuances, including common stock sales and convertible securities, which will dilute existing shareholders and potentially pressure the stock further. Rumors have also circulated about substantial cost-cutting initiatives, including potential headcount reductions of 30,000 to 40,000 employees - representing roughly 20% of the workforce—as well as discussions around divesting assets such as Cerner, the healthcare unit acquired for $28 billion four years ago. These steps highlight the urgency Oracle faces in generating cash amid its capital-intensive commitments.

The Stargate Curse

Ironically, many of these difficulties trace back to what initially appeared to be a transformative opportunity: the landmark agreement with OpenAI as part of the Stargate project. This deal, valued at approximately $300 billion over five years, positions Oracle to provide vast computing power to support OpenAI's AI ambitions, starting in 2027 and involving the development of gigawatts of data center capacity.

Source: Fiscal.ai

Stargate, a broader initiative involving OpenAI, Oracle, and partners like SoftBank, aims to build national-scale AI infrastructure in the U.S., with investments potentially reaching hundreds of billions. Yet this very success has created what can be termed the "Stargate Paradox." To capture the promised revenue, Oracle must invest enormously upfront in physical infrastructure, pushing its balance sheet to the brink. The company is constructing what could become some of the world's most valuable AI computing assets, but the fixed costs, debt financing, and execution risks threaten its very survival. Investors appear unconvinced that Oracle can manage this pressure without eroding shareholder value or inviting credit downgrades.

OpenAI IPO as a Panacea

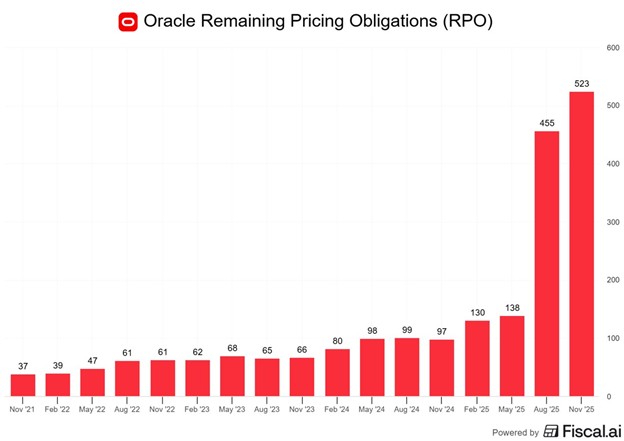

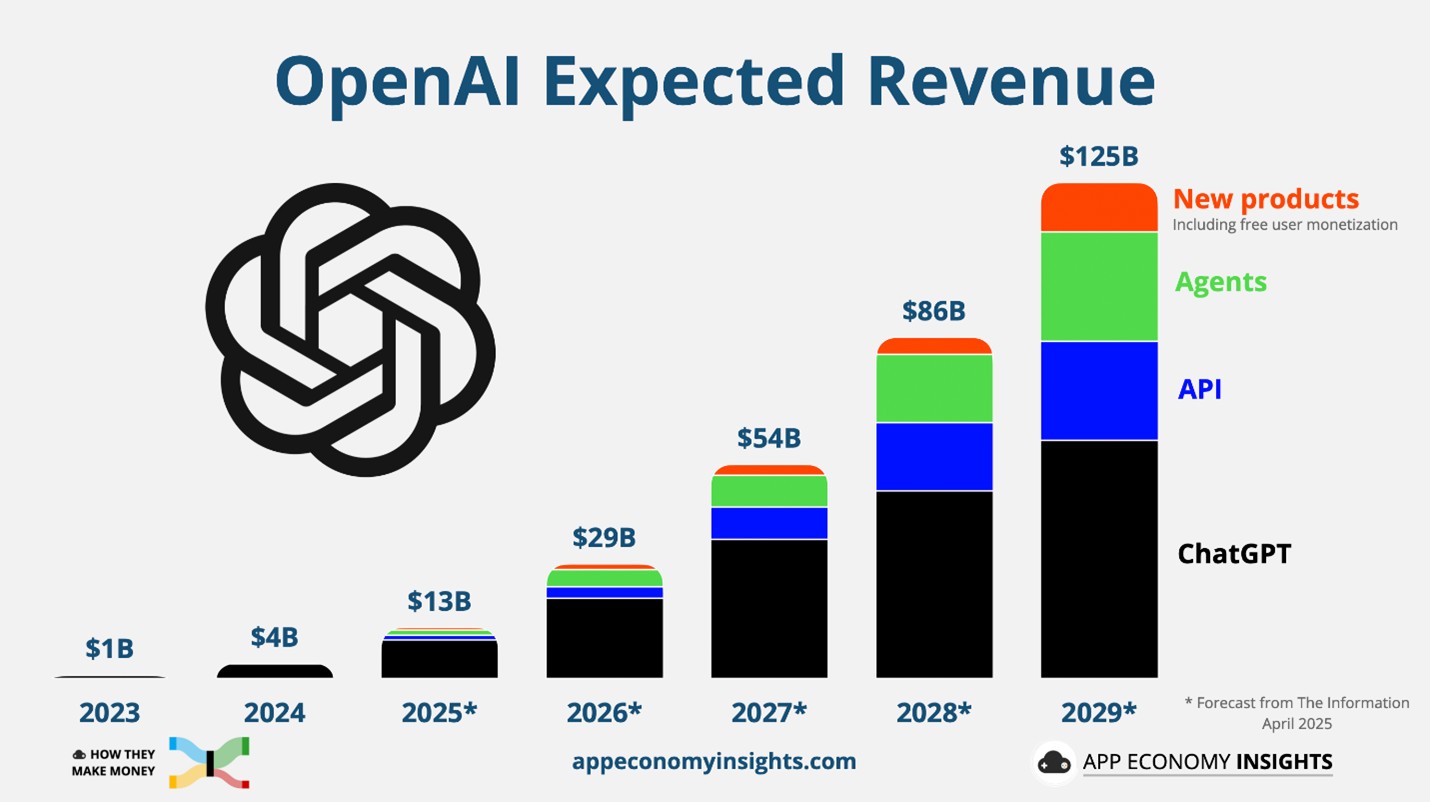

Oracle's long-term viability increasingly hinges on OpenAI's ability to fulfill its commitments. The $300 billion in remaining performance obligations represents future payments from OpenAI for the computing capacity Oracle is delivering. However, OpenAI continues to operate at a loss, (despite the top-line moving up exponentially) burning substantial cash on research, development, and infrastructure. The primary path for OpenAI to generate the funds needed to pay Oracle involves going public, with an IPO anticipated potentially by the end of 2026 or in 2027. Estimates suggest this listing could raise $60 billion to $100 billion or more, depending on the valuation achieved—current private valuations have ranged from $500 billion to over $800 billion in funding discussions. Proceeds from such an offering could directly flow to Oracle, providing critical liquidity to service debt, fund ongoing builds, and stabilize operations.

Source: App Economy Insights

But It’s not all Positive

Nevertheless, this dependency introduces substantial risks and potential side effects. If the market assigns OpenAI a lower valuation than expected—say $500 billion instead of $1 trillion—the IPO proceeds would fall short, limiting the cash available for Oracle and jeopardizing revenue recognition. Moreover, the public listing process would require OpenAI to disclose detailed financials, including revenue projections, expense breakdowns, customer dependencies, and industry outlooks. Any hint during earnings calls or filings that growth might slow, costs could overrun, or demand could soften, could trigger sharp declines in both OpenAI's stock and Oracle's shares, given the intertwined fortunes.

Unequal Relationship

But there is something more than just high debt and bad balance sheet. The public rarely talks about the relationship between the two companies themselves. In fact, investors are also uneasy because Oracle is in a more unfavorable situation compared to OpenAI.

OpenAI initially relied on Microsoft's Azure for cloud services but outgrew that capacity, turning to Oracle out of necessity rather than preference for superior technology. From OpenAI's viewpoint, Oracle functions primarily as a commoditized supplier of compute power with limited differentiation. In the Stargate framework, Oracle serves as the "builder" of infrastructure, while OpenAI retains ownership, decision-making authority, and the intellectual property value of its models. OpenAI could switch providers, partner with others, or even use IPO proceeds to construct its own facilities, reducing long-term reliance on Oracle. This leaves Oracle exposed to the possibility that its massive investments yield underutilized capacity in future years.

Concentration risk further amplifies concerns. Unlike hyperscalers such as Amazon (with e-commerce), Microsoft (with software), or Google (with advertising), which boast diversified revenue streams and develop their own AI products, Oracle is heavily betting on a single major client in this AI buildout.

A very strong proof for the weaker standing of Oracle compared to the other hyperscalers is the fact that according to some analysts, OpenAI reportedly bargained for a price of roughly $10 per GPU-hour, significantly lower than the $14–$18 standard charged by AWS or Azure.

The table below summarizes the asymmetry:

Feature | OpenAI (The Client) | Oracle (The Builder) |

Asset | Intellectual Property (Models) | Physical Infrastructure (Data Centers) |

Cost Type | Research & Development (Flexible) | Capital Expenditure (Fixed/Debt-heavy) |

Dependency | Can switch providers or build own | Stuck with the debt regardless of usage |

Market Role | The "Brain" | The "Utility" |

Summary

Oracle's plunge reflects a high-stakes gamble on AI infrastructure that has strained its finances and exposed vulnerabilities. While the Stargate deal and OpenAI partnership offer enormous upside if executed successfully, the paradox persists: the path to becoming a key AI enabler risk undermining the company's stability.

Oracle's survival may depend on OpenAI's successful transition to profitability and public markets, but lingering uncertainties around valuation, disclosures, and strategic dependencies leave investors wary.

The coming months, particularly around any OpenAI IPO developments, will prove pivotal in determining whether Oracle can convert its bold vision into sustainable value or face prolonged challenges.

Find out more

Comments