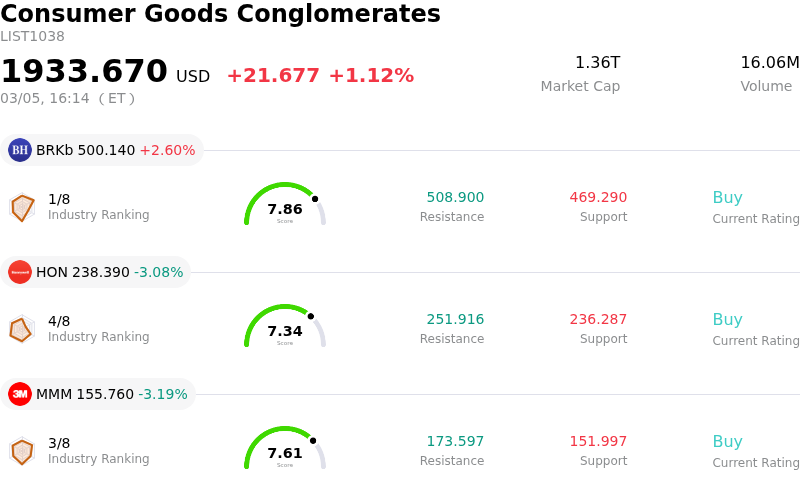

Honeywell International Inc (HON) closed down by 3.08%. The Consumer Goods Conglomerates sector is up by 1.12%. The company underperformed the industry. Top 3 stocks by trading volume in the sector: Berkshire Hathaway Inc (BRKb) up 2.60%; Honeywell International Inc (HON) down 3.08%; 3M Co (MMM) down 3.19%.

What is driving Honeywell International Inc (HON)’s stock price down today?

Honeywell (HON) experienced notable intraday volatility, leading to a share price decline. This movement follows recent strategic announcements and some analyst adjustments.

On March 3, 2026, Honeywell announced the filing of its Form 10 registration statement with the U.S. Securities and Exchange Commission for the planned spin-off of Honeywell Aerospace. This new entity is expected to trade on Nasdaq under the ticker HONA and is targeted for an independent public debut in Q3 2026. The Form 10 details pro forma 2025 net sales of $17.4 billion, net income of $1.5 billion, and Adjusted EBIT of $4.3 billion for the aerospace segment. An Investor Day for the new aerospace and defense company is scheduled for June 3, 2026. While the spin-off aims to enhance strategic focus and unlock shareholder value, it also introduces a period of uncertainty and re-evaluation for investors as the company's structure changes. Honeywell Aerospace has historically contributed approximately 35% of Honeywell's total annual revenue.

In terms of analyst sentiment, multiple firms have recently updated their ratings and price targets for HON. On March 4, 2026, Jefferies maintained a 'Hold' rating but raised its price target to $245.00 from $240.00. Barclays also maintained an 'Overweight' rating, increasing its price target to $275 from $259 on March 4, 2026. Wolfe Research upgraded Honeywell to 'Outperform' with a $293.00 price target on February 27, 2026, citing the completion of the company's portfolio separation work. Despite these positive adjustments and a consensus 'Buy' rating from analysts, the market may be reacting to potential shifts in the company's risk profile, cash generation, or capital allocation as the portfolio transformation progresses.

Fourth-quarter 2025 earnings reported on January 29, 2026, showed adjusted EPS of $2.59, exceeding expectations, though revenue of $9.76 billion, up 6.4% year-over-year, missed estimates slightly. The company also issued a 2026 outlook, anticipating adjusted EPS between $10.35 and $10.65, slightly above consensus. The market's reaction to the spin-off news and ongoing strategic changes appears to be a dominant factor, influencing investor sentiment and contributing to the stock's current price fluctuations.

Technical Analysis of Honeywell International Inc (HON)

Technically, Honeywell International Inc (HON) shows a MACD (12,26,9) value of [6.95], indicating a neutral signal. The RSI at 65.86 suggests neutral condition and the Williams %R at -23.97 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Honeywell International Inc (HON)

Honeywell International Inc (HON) is in the Consumer Goods Conglomerates industry. Its latest annual revenue is $37.44B, ranking 3 in the industry. The net profit is $5.14B, ranking 3 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $248.00, a high of $293.00, and a low of $201.25.

More details about Honeywell International Inc (HON)

Company Specific Risks:

- Honeywell reported additional impairment charges totaling $471 million within its Productivity Solutions and Services and Warehouse and Workflow Solutions businesses, leading to a revision of its 2025 earnings.

- The planned spinoff of Honeywell Aerospace involves significant incremental costs of $202 million, encompassing a $150 million trademark license agreement and $33 million for transition services.

- The company faces regulatory challenges and potential compliance costs related to Minnesota's new ban on "forever chemicals" (PFAS), which could impact over 2,000 parts in its aerospace and defense facilities and pharmaceutical packaging materials.

- Analysts note that Honeywell's debt is not adequately covered by operating cash flow, posing a financial risk as the company executes ongoing portfolio changes and restructuring.

Find out more

Comments