Previous Week’s Market Review & Analysis

TradingKey - Macroeconomic Landscape: The period from March 9-15, 2026, was dominated by escalating geopolitical tensions in the Middle East, primarily centered on the Iran conflict, which led to a significant surge in oil prices. West Texas Intermediate (WTI) crude oil jumped 36% for the week, pushing prices above $90 per barrel, with some reports noting even higher levels, and Brent oil also rising considerably. This rapid increase in energy costs fueled renewed inflation fears and raised concerns about global growth due to potential disruptions in the Strait of Hormuz. On the domestic front, the US labor market showed unexpected weakness as nonfarm payrolls fell by 92,000 in February, significantly missing consensus estimates. The unemployment rate subsequently rose to 4.4% in February from 4.3% in January. Despite job losses, average hourly earnings increased 0.4% in February, marking a 3.8% year-over-year rise, suggesting persistent wage growth. Inflation data for February indicated that the annual rate held steady at 2.4%, with core inflation remaining at 2.5%, though the monthly CPI rose 0.3%. Manufacturing Purchasing Managers' Index (PMI) was 51.6 in February, reflecting moderate expansion but softer momentum, while the Services PMI of 51.7, though lower than expected, still indicated growth. Ten-year Treasury yields rebounded to approximately 4.14%, indicating heightened inflation anxiety.

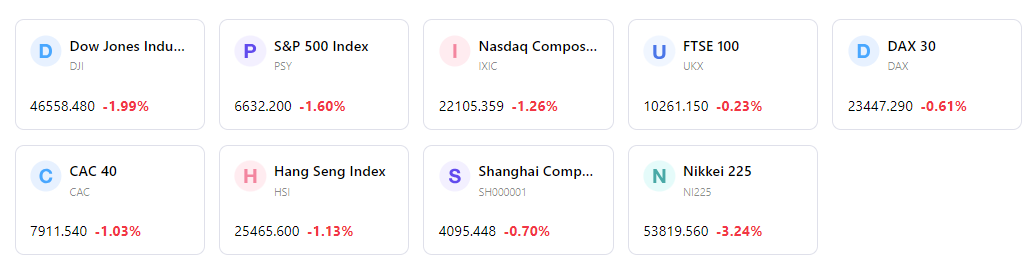

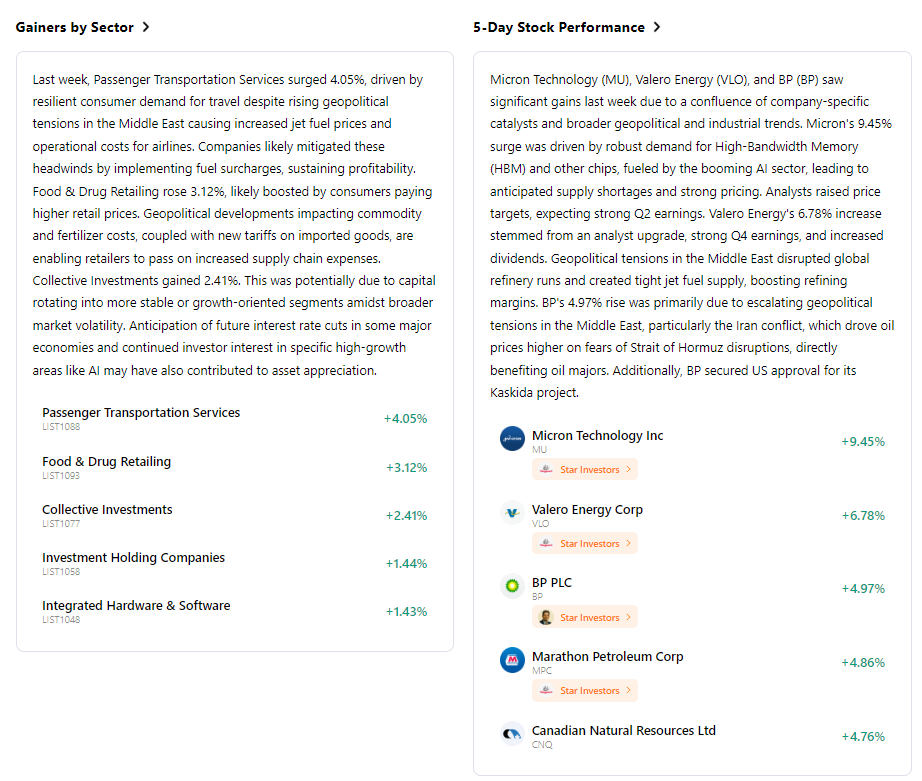

Market Performance Overview: US equities experienced a volatile week. While Monday, March 9, saw a rebound from initial declines with the S&P 500 rising 0.8%, the Dow 0.5%, and the Nasdaq 1.4%, market sentiment turned negative for the remainder of the week as geopolitical concerns intensified. The S&P 500 consequently declined to its lowest level since mid-December. The CBOE Volatility Index (VIX) surged to 29.49, reflecting heightened market uncertainty. Sector performance was mixed, with energy and defense stocks showing resilience amidst the geopolitical backdrop, while technology, industrials, and consumer discretionary sectors faced headwinds.

Key Events Analysis: The primary market mover was the escalation of the Middle East conflict, causing a significant spike in oil prices and leading to broad risk-off sentiment. The disappointing February jobs report further weighed on investor confidence, raising concerns about the health of the labor market. Federal Reserve communications during this period did not include new policy announcements, but the weaker economic data and rising inflation fears led to a reassessment of monetary policy expectations, with the probability of a June rate cut falling.

Flows & Sentiment: Market sentiment was distinctly negative and cautious, with a broad risk-off move. Volatility indicators like the VIX rose sharply. While cash allocations were reportedly low, a spike in the Geopolitical Risk Index to 600 suggested extreme conditions. Investors sought safety in commodity-linked sectors and large-cap technology names.

Overall Assessment: The week was characterized by significant market turbulence, largely driven by escalating geopolitical risks that triggered an oil price shock and compounded by a notably weak US jobs report. This confluence of events rekindled stagflation concerns, placing the Federal Reserve in a challenging position regarding future monetary policy. Despite some intra-week rebounds, the overarching theme was one of caution and uncertainty.

Next Week’s key market drivers & Investment Outlook

Upcoming Events: The upcoming week will feature several key economic data releases. On Tuesday, March 17, US Existing Home Sales for February are due. Wednesday, March 18, will bring the closely watched US Consumer Price Index (CPI) report for February. Thursday will see the release of US Producer Price Index (PPI) data, followed by US annual GDP for Q4 (secondary estimate), US core Personal Consumption Expenditures (PCE), and the University of Michigan's preliminary consumer sentiment index on Friday, March 20. Several companies, including Alimentation Couche Tard, Elbit Systems, and Tencent Music Entertainment Group, are scheduled to report earnings on Tuesday, March 17.

Market Logic Projection: Markets are anticipated to remain highly sensitive to developments in the Middle East, with oil prices and geopolitical headlines continuing to exert a strong influence. The interplay between persistent inflation concerns and a softening labor market will keep the Federal Reserve's stance on interest rates under intense scrutiny. Upcoming inflation data will be particularly critical in shaping market expectations for monetary policy.

Strategy & Allocation Recommendations: Investors are advised to maintain a prudent and patient approach amid ongoing uncertainty. Diversification remains crucial, and a strategic allocation to investments that can perform well in volatile environments is recommended. Sectors such as energy and defense may continue to benefit from geopolitical risk premiums, while vigilance regarding the impact of higher energy costs on consumer-driven sectors is warranted.

Risk Alerts: The foremost risk remains the potential for further escalation of the Middle East conflict, which could lead to sustained higher oil prices and a more pronounced impact on global economic stability and inflation. The renewed specter of stagflation, characterized by slowing growth and persistent inflation, poses a significant threat. Uncertainty surrounding the Federal Reserve's interest rate path, given conflicting signals from inflation and employment data, continues to be a key risk factor for market participants. Expect elevated market volatility to persist.

Markets Weekly

5-Day Index Performance

Find out more

Comments