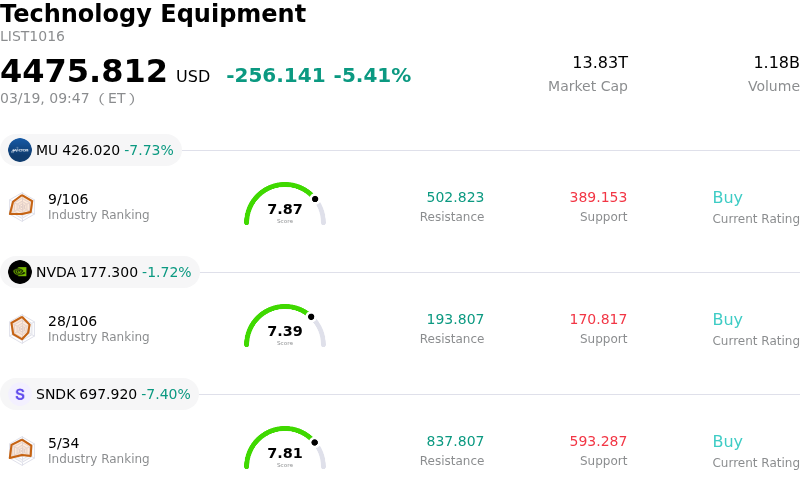

Micron Technology Inc (MU) opened down by 7.73%. The Technology Equipment sector is down by 5.41%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 7.73%; NVIDIA Corp (NVDA) down 1.72%; SanDisk Corporation (SNDK) down 7.40%.

What is driving Micron Technology Inc (MU)’s stock price down today?

Micron Technology's stock experienced a significant downward movement today, despite the company reporting record-breaking second-quarter financial results that exceeded analyst expectations for both revenue and earnings per share. This counter-intuitive reaction appears to be primarily driven by a combination of investor concerns over increased capital expenditure and broader geopolitical risks.

A key factor contributing to the negative market sentiment is Micron's announcement of substantially increased capital spending for fiscal year 2026, with projections now above $25 billion. While this investment is aimed at expanding manufacturing capacity to meet the robust demand for AI chips and High-Bandwidth Memory (HBM), some investors are wary. There is concern that such aggressive spending could lead to a potential "supply glut" in the future if demand growth falters, potentially impacting pricing and profit margins, a historical risk in the cyclical semiconductor industry. This elevated spending also raises questions about short-term cash flow, despite the company forecasting significantly higher free cash flow in the upcoming quarter.

Adding to the pressure, news of an attack on energy infrastructure in the Middle East during the earnings call introduced macroeconomic uncertainty. The memory chip sector is highly dependent on liquefied natural gas (LNG) from the region to power its Asian manufacturing facilities, leading to concerns about potential energy supply disruptions and increased operational costs.

Despite the stock's substantial appreciation over the past year, indicating strong market confidence leading into the earnings report, the negative reaction to these new developments suggests a degree of profit-taking. Although the company has secured a five-year strategic customer agreement and is seeing strong demand for its HBM products, with HBM4 already in high-volume production, the cautious outlook regarding future expenditure and external geopolitical events has overshadowed the otherwise strong financial performance and optimistic guidance for the upcoming quarter.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of [9.03], indicating a buy signal. The RSI at 64.25 suggests neutral condition and the Williams %R at -8.45 suggests oversold condition. Please monitor closely.

Media Coverage of Micron Technology Inc (MU)

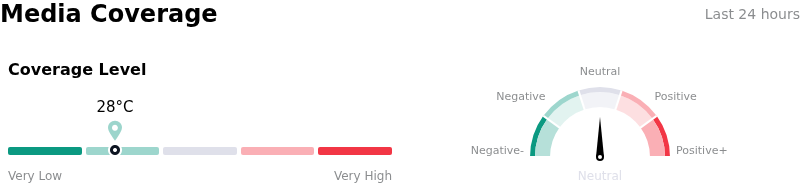

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 28, indicating a low level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $415.07, a high of $650.00, and a low of $86.28.

More details about Micron Technology Inc (MU)

Company Specific Risks:

- Micron's aggressive capital expenditure plans, exceeding $25 billion for FY2026 and further increasing in FY2027 for new fabrication plants, are generating investor concerns about potential long-term oversupply in the memory market and future pressure on gross margins, despite current robust demand.

- The company faces a legal challenge to its planned $100 billion megafab campus in New York, targeting the project's environmental review process, which could lead to construction delays and create uncertainty around its long-range manufacturing expansion and capital deployment.

- Concerns exist regarding Micron's competitive standing in the high-bandwidth memory (HBM) market, specifically being reportedly excluded from Nvidia's flagship Vera Rubin HBM4 program and instead supplying lower-tier accelerators, with a key competitor holding a primary supplier position for Nvidia.

Find out more

Comments