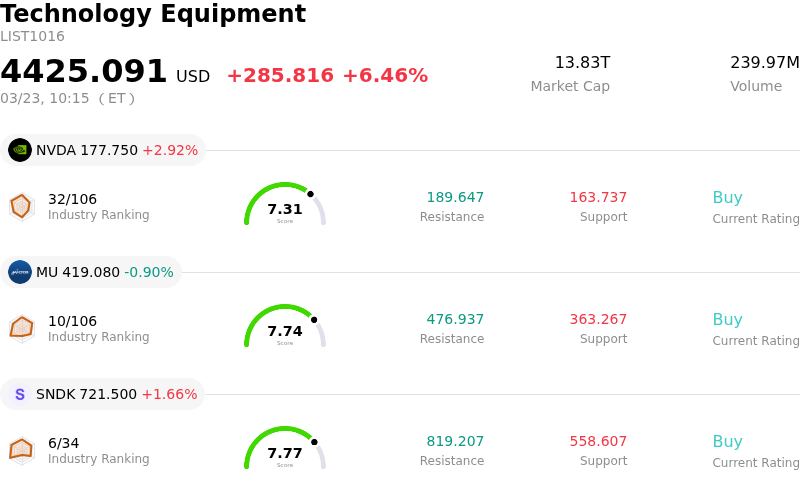

Taiwan Semiconductor Manufacturing Co Ltd (TSM) moved up by 3.21%. The Technology Equipment sector is up by 6.46%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 2.92%; Micron Technology Inc (MU) down 0.90%; SanDisk Corporation (SNDK) up 1.66%.

What is driving Taiwan Semiconductor Manufacturing Co Ltd (TSM)’s stock price up today?

Taiwan Semiconductor Manufacturing Company (TSM) experienced an upward movement today, primarily driven by continued strong demand for its advanced semiconductor technologies, particularly in the artificial intelligence sector, alongside positive analyst sentiment. Recent upgrades from various investment firms have contributed to this positive momentum.

Wall Street Zen, for instance, upgraded TSM from a "hold" to a "buy" rating in a report issued on Sunday, March 22, contributing to an overall consensus "Buy" rating among analysts. This follows Bank of America Securities reiterating a "Buy" rating on March 19, citing resilient growth and earnings power fueled by high-performance computing and AI chip demand. These analyst endorsements often reflect confidence in the company's market position and future growth prospects. Independence Wealth Advisors LLC also disclosed acquiring a new stake in TSM, indicating institutional confidence in the stock.

The core driver for TSM remains the explosive demand for AI chips and the company's crucial role as the world's largest contract chipmaker. Reports indicate that demand for TSMC's advanced-node capacity, such as 3nm and 2nm, significantly exceeds supply, with capacity fully booked until 2028 and potentially beyond. This is further underscored by news suggesting that a major AI chip customer may need to redesign its next-generation platform due to limited TSMC production capacity.

TSMC's financial outlook remains robust, with strong quarterly results and positive revenue guidance. The company reported record February revenue and anticipates sequential revenue growth for the first quarter of 2026, largely due to demand from high-performance computing customers. The forecast for full-year 2026 earnings per American Depositary Share has been raised, reflecting an accelerated compound annual growth rate for AI-related revenue and an overall strong revenue growth expectation. Furthermore, planned price increases for 2026 are expected to further bolster profit margins. The broader semiconductor industry itself is projected for substantial growth in 2026, reaching significant milestones in sales, primarily propelled by AI infrastructure.

Technical Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Technically, Taiwan Semiconductor Manufacturing Co Ltd (TSM) shows a MACD (12,26,9) value of [-1.00], indicating a sell signal. The RSI at 39.08 suggests neutral condition and the Williams %R at -88.72 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Taiwan Semiconductor Manufacturing Co Ltd (TSM) is in the Technology Equipment industry. Its latest annual revenue is $122.22B, ranking 2 in the industry. The net profit is $55.12B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $410.08, a high of $520.00, and a low of $205.00.

More details about Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Company Specific Risks:

- Geopolitical tensions in the Middle East, particularly the Iran War, threaten critical material supply chains for helium and energy (LNG), which could lead to production disruptions and increased operating costs for TSMC's manufacturing processes.

- Recent analyst downgrades, including Zacks Research lowering TSM from "strong-buy" to "hold" and Wall Street Zen reducing it from "buy" to "hold," reflect concerns over the company's valuation and potential for multiple compression.

- Increased competitive pressure from rivals like Samsung is evident with Tesla awarding its 2nm chip production to Samsung, indicating a potential loss of high-margin client business and diversification away from TSM.

- TSMC's substantial reliance on Taiwan's power grid, which is heavily dependent on liquefied natural gas imports, exposes the company to production volatility and higher energy costs if LNG supply issues persist.

Find out more

Comments