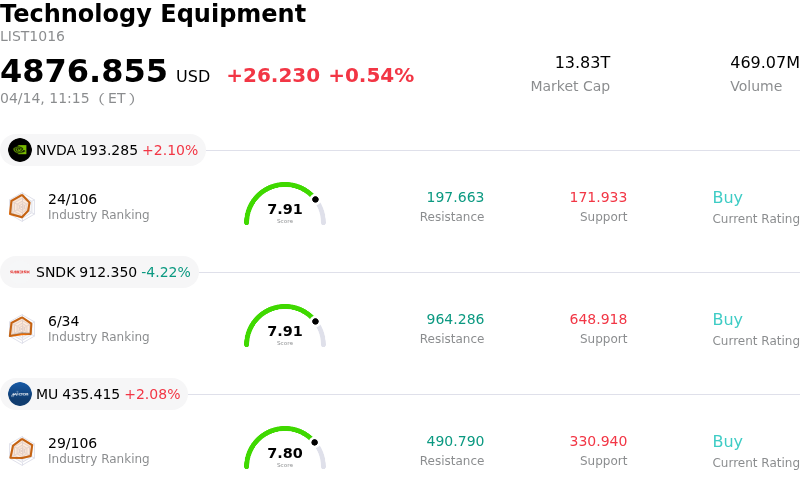

Intel Corp (INTC) moved down by 3.07%. The Technology Equipment sector is up by 0.54%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 2.10%; SanDisk Corporation (SNDK) down 4.22%; Micron Technology Inc (MU) up 2.08%.

What is driving Intel Corp (INTC)’s stock price down today?

Intel (INTC) experienced a notable decline in its share price today, following a period of significant upward momentum. This downward movement appears to be a reaction to a combination of factors, including the stock's recent rapid appreciation, cautious analyst sentiment regarding its valuation, and upcoming earnings expectations.

Over the past nine trading sessions, Intel's shares had surged, adding over $100 billion to its market capitalization and making it one of the top-performing stocks in the S&P 500 Index. This rally was fueled by strategic announcements, such as the company's decision to repurchase its 49% equity interest in a semiconductor plant in Ireland for $14.2 billion, and partnerships, including one with Elon Musk's Terafab project and Google's commitment to use future Xeon processors. Strong demand for server CPUs and a resilient personal computer market also contributed to this positive sentiment. Intel is also seen as a key beneficiary of the US CHIPS Act, supporting its onshore manufacturing efforts.

However, despite this recent surge, a significant portion of Wall Street analysts remain cautious. Only a limited number of analysts currently hold "buy" ratings on Intel's stock, and its overall recommendation score is among the lowest in the chipmaking sector. The stock's valuation has reached historic levels, trading at over 90 times forward earnings, which is considerably higher than the semiconductor industry average. Analysts suggest that this high valuation is already pricing in a substantial recovery and leaves little room for disappointment.

Intel is set to report its first-quarter 2026 financial results on April 23, and current guidance indicates modest revenue and near-breakeven earnings per share. While some analysts have recently increased their price targets for Intel, the consensus price target remains lower than the current trading price, implying a potential downside. The market is demanding strong execution from Intel to justify its current valuation, and upcoming earnings will be a critical test of whether the company can validate the optimistic narrative that has driven its recent rally.

Furthermore, broader macroeconomic concerns, such as global markets falling due to surging oil prices on Iran tensions, could contribute to a more cautious market sentiment, impacting even stocks that have recently performed well. The semiconductor industry as a whole is experiencing "memflation," with memory prices expected to increase sharply, potentially impacting demand outside the AI segment and posing challenges for suppliers. While strong AI chip demand is driving overall semiconductor revenue growth, geopolitical risks, including the Middle East conflict, are a concern for global chip supply chains.The decline in Intel's (INTC) share price today appears to be a market correction following a significant rally, driven by cautious analyst sentiment and concerns about the company's elevated valuation. Over the past nine trading sessions, Intel's stock had experienced a substantial increase, adding over $100 billion to its market capitalization. This surge was primarily attributed to strategic moves like the $14.2 billion repurchase of its 49% equity interest in an Irish semiconductor manufacturing facility and new partnerships, including collaborations with Elon Musk's Terafab project and Google for future Xeon processors. The company has also benefited from robust demand for server CPUs and a resilient personal computer market, alongside its strategic position as a beneficiary of the US CHIPS Act.

Despite these positive developments, a considerable portion of Wall Street analysts maintain a cautious outlook. Only a minority of analysts have issued "buy" ratings for Intel, and its overall recommendation score is among the lowest in the semiconductor industry. This circumspection stems from the stock's current valuation, which is trading at over 90 times forward earnings, a record high that significantly surpasses the industry average. Analysts suggest that this high valuation already incorporates a substantial recovery, leaving minimal room for any negative surprises.

Intel is scheduled to report its first-quarter 2026 financial results on April 23. The company's current guidance forecasts modest revenue and near-breakeven earnings per share, which some analysts believe provides limited leeway for disappointment. While some firms have recently raised their price targets for Intel, the overall consensus price target remains below the current trading level, implying a potential downside. The market is now closely scrutinizing Intel's ability to execute its turnaround strategy and deliver results that can justify its premium valuation.

Broader market conditions, such as global market declines influenced by geopolitical tensions and surging oil prices, may also contribute to a more risk-averse environment for investors. Within the semiconductor industry, "memflation" – a sharp increase in memory prices – is also a factor, potentially impacting demand in non-AI segments and presenting cost challenges for manufacturers. Although AI chip demand continues to drive overall semiconductor revenue growth, geopolitical risks, particularly those affecting global supply chains, remain a concern.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of [2.00], indicating a buy signal. The RSI at 77.84 suggests buy condition and the Williams %R at -1.88 suggests oversold condition. Please monitor closely.

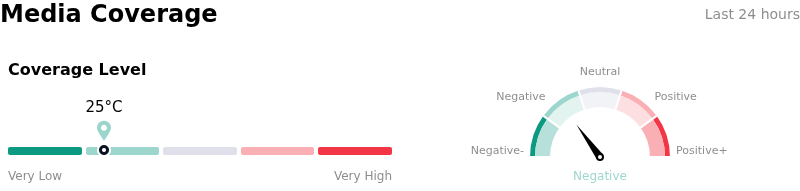

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 25, indicating a low level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 109 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $49.39, a high of $92.00, and a low of $20.40.

More details about Intel Corp (INTC)

Company Specific Risks:

- HSBC downgraded Intel stock to "Reduce" due to concerns that its recent rally is unsustainable and driven by one-off deals, with ongoing manufacturing execution failures in its foundry segment remaining a significant drag on financials.

- Intel's repurchase of Apollo's 49% stake in Fab 34 for $14.2 billion, partly financed by a $6.5 billion bridge loan, introduces refinancing risk and increased leverage, impacting the company's cash position.

- The upcoming departure of Intel's Executive Vice President and Chief Legal Officer, April Miller Boise, effective June 1, 2026, as disclosed in a recent 8-K filing, may create uncertainty in the company's legal strategy and compliance functions.

- An ongoing lawsuit, unsealed March 11, 2026, alleges Intel's sale of a 10% stake to the U.S. government was "extortionary" and illegal, seeking to void the transaction and posing a significant legal and financial risk.

Find out more

Comments