Track Market Trends

TradingKey - On July 8, Eastern Time, US stock markets diverged. The escalation of the US-Iran conflict pushed energy prices higher once again, fueling market concerns over sticky inflation and the Federal Reserve's policy path. Consequently, the Dow Jones Industrial Average and the S&P 500 Index closed lower under pressure. However, technology stocks and select semiconductor equities rebounded after consecutive pullbacks, supporting a modest gain in the Nasdaq Composite Index.

At the close, the Dow Jones Industrial Average fell 1.09% to 52,353.24; the S&P 500 Index declined 0.28% to 7,482.71; and the Nasdaq Composite Index rose 0.20% to 25,870.65.

In terms of sectors and individual stocks, semiconductors and technology shares outperformed the broader market. Broadcom ( AVGO) gained 4.83%, primarily boosted by Apple ( AAPL) expanding its procurement agreement for US-made chips; Nvidia ( NVDA) rose 3.65%, continuing to find support from robust demand for AI computing power; Micron Technology ( MU) edged up 1.1%, AMD ( AMD) rose slightly by 0.20%, and Apple gained 0.88%.

In commodity markets, crude oil prices surged. Following a new round of US military strikes on Iran, Trump declared that the temporary US-Iran ceasefire arrangement had ended, reigniting security risks for shipping in the Strait of Hormuz. Brent crude jumped 3.69% to close at $79.49 per barrel; WTI ( USOIL) crude rose approximately 3.57%, breaking above $75 during intraday trading to close at $74.77 per barrel.

For precious metals, spot gold ( XAUUSD) fell 0.69% to $4,077.67. Although geopolitical risks typically boost safe-haven demand, the recent spike in oil prices has heightened inflation worries. This prompted the market to re-bet that the Federal Reserve might maintain a tighter policy stance, leading to a stronger US dollar and higher Treasury yields, which put downward pressure on the non-yielding asset,yielding asset gold.

Market News

FOMC minutes show mounting concerns over inflation. Minutes from the Federal Reserve's June meeting showed that officials' concerns over spreading price pressures have heightened, with some members suggesting that further interest rate hikes may still be necessary in the future if inflation remains persistently high. The meeting left interest rates unchanged in the 3.50% to 3.75% range, but the minutes revealed limited tolerance for inflation at the policy level. The Fed under Walsh also continued to de-emphasize forward guidance on interest rates, meaning market reactions to upcoming employment, inflation, and energy price data could become more volatile.

Apple reaches over $30 billion chip supply agreement with Broadcom. Apple announced it will purchase over $30 billion worth of U.S.-made chips from Broadcom under a multi-year agreement. The deal, which covers radio frequency chips related to wireless connectivity, extends through 2031. As part of the arrangement, Broadcom will invest $1.5 billion to expand production at its Fort Collins facility in Colorado. The transaction not only aligns with U.S. policy promoting domestic semiconductor manufacturing, but also eases market concerns that Apple's accelerated chip self-reliance would undermine Broadcom's supplier status.

Escalating U.S.-Iran conflict once again rattles energy markets. Following a new round of U.S. military strikes on Iran, Trump stated that the previous temporary truce between the U.S. and Iran has ended. The U.S. military said the operation was linked to Iran's recent attacks on commercial vessels in the Strait of Hormuz. Because the Strait of Hormuz handles a massive portion of global crude oil and liquefied natural gas shipments, the market fears that if both sides continue to escalate, shipping insurance costs, transit risks for tankers, and energy supply uncertainties will all rise.

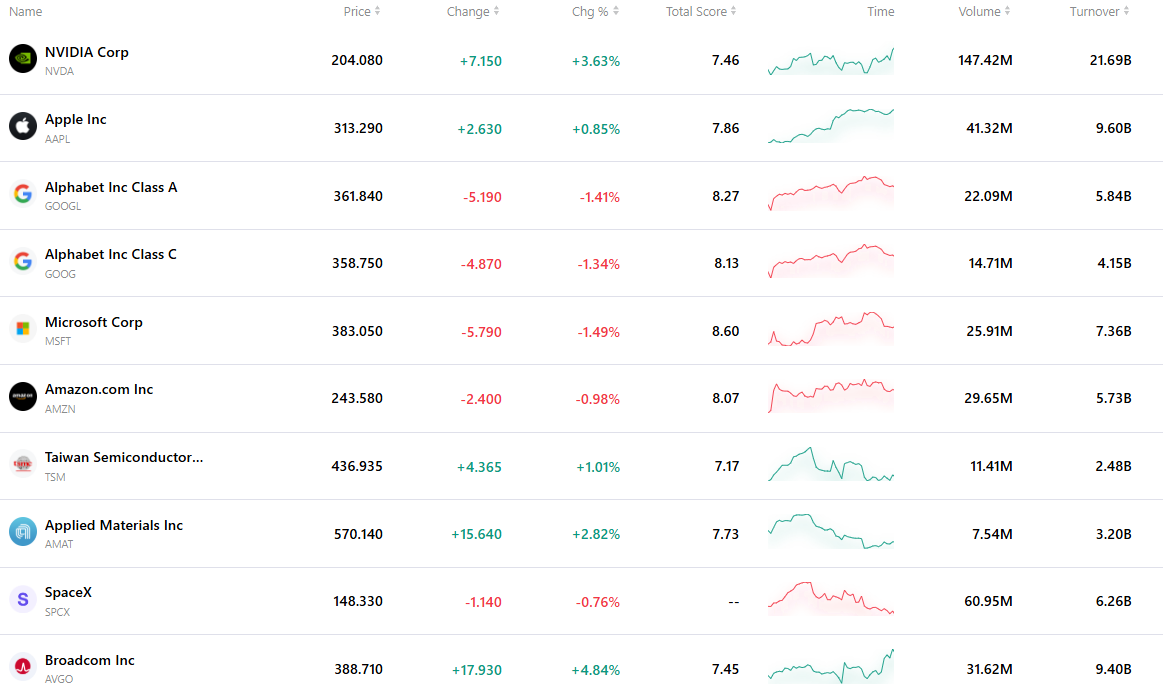

Top 10 Most Active Stocks

The table below lists the ten most actively traded stocks in the latest market. Supported by massive trading volume and excellent liquidity, these assets have become key benchmarks for tracking global market dynamics.

Find out more

Comments