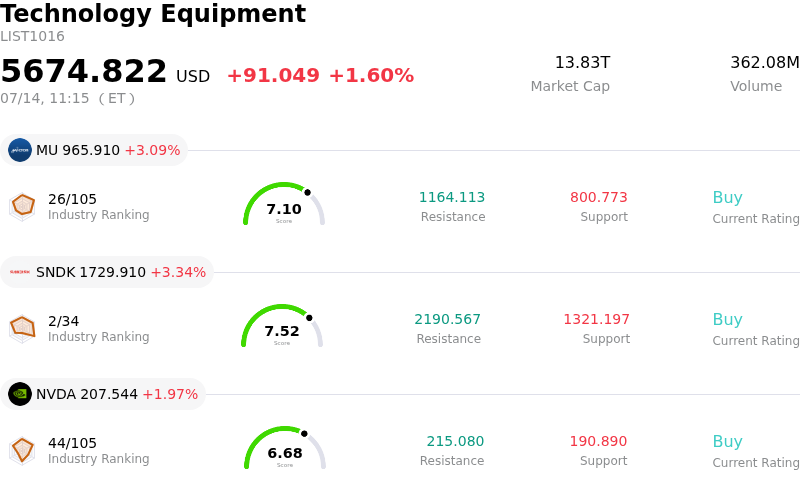

KLA Corp (KLAC) moved up by 3.65%. The Technology Equipment sector is up by 1.60%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 2.93%; SanDisk Corporation (SNDK) up 3.34%; NVIDIA Corp (NVDA) up 1.97%.

What is driving KLA Corp (KLAC)’s stock price up today?

KLA Corporation is currently benefiting from a broader sectoral shift as the semiconductor industry transitions into the next generation of advanced logic and memory nodes. The surge in demand for high-precision metrology and inspection tools, where the company maintains a dominant position, continues to drive institutional confidence. Investors are increasingly viewing the firm as a defensive yet high-growth play within the technology hardware space, particularly as leading foundries accelerate their transitions to sub-2nm processes. This technological migration significantly increases the complexity of chip manufacturing, making the company’s yield management solutions essential for maintaining economic viability in global fab operations.

The intraday volatility observed in the stock reflects a tug-of-war between macroeconomic sensitivities and company-specific fundamentals. Recent data suggests that global capital expenditure in the semiconductor equipment sector is decoupling from general industrial cycles, driven instead by the structural necessity of artificial intelligence infrastructure. Analyst sentiment has turned increasingly positive in the lead-up to the upcoming quarterly earnings season, with several major brokerage firms revising their price targets upward. These revisions are largely predicated on the expectation of robust gross margins and a strong backlog of orders from international clients who are racing to achieve domestic chip sovereignty.

Furthermore, broader market dynamics, including the periodic rebalancing of major semiconductor-focused exchange-traded funds, have likely contributed to the upward pressure on the share price. Large-scale institutional portfolio adjustments often precede significant industry inflection points, and the company's inclusion in high-conviction lists for the fiscal year has bolstered its liquidity and buy-side support. While the macro environment remains clouded by fluctuating interest rate expectations and geopolitical considerations regarding trade restrictions, the firm’s unique technological moat provides a layer of insulation that few peers in the equipment space can match.

Despite the positive trajectory, the inherent risks associated with supply chain concentration and potential shifts in export control policies continue to linger in the background. However, the current market sentiment suggests that the growth opportunities in advanced packaging and optical inspection outweigh these operational hurdles. As the market prepares for the next cycle of financial disclosures, the company remains a central figure in the narrative of semiconductor manufacturing excellence, attracting capital from investors seeking exposure to the mission-critical layers of the global technology stack.

Technical Analysis of KLA Corp (KLAC)

Technically, KLA Corp (KLAC) shows a MACD (12,26,9) value of 97.357, indicating a neutral signal. The RSI at 23.115 suggests sell condition and the Williams %R at 88.199 suggests oversold condition. Please monitor closely.

Media Coverage of KLA Corp (KLAC)

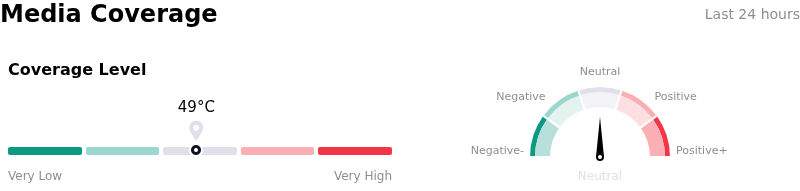

In terms of media coverage, KLA Corp (KLAC) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of KLA Corp (KLAC)

KLA Corp (KLAC) is in the Technology Equipment industry. Its latest annual revenue is $12.16B, ranking 15 in the industry. The net profit is $4.06B, ranking 11 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $225.27, a high of $317.00, and a low of $138.80.

More details about KLA Corp (KLAC)

Company Specific Risks:

- Geopolitical Export Constraints: Heightened concerns regarding potential new U.S. Department of Commerce restrictions on semiconductor manufacturing equipment exports to China pose a significant threat to KLA’s revenue stability, as the region has historically represented over 40% of the company's total shipments.

- Negative Sector Read-Through: Sustained volatility following ASML’s recent downward revision of its 2025 outlook has intensified institutional fears that the broader Wafer Fab Equipment (WFE) recovery is stalling, specifically impacting demand for KLA’s metrology and inspection tools in the non-AI logic and memory segments.

- Pre-Earnings De-risking: Ahead of the scheduled October 30 earnings release, KLA is experiencing intraday pressure as investors rotate out of high-multiple semiconductor stocks, fearing that any conservative guidance regarding 2025 capacity expansion could trigger a sharp valuation de-rating.

- Utilization and Lead-Time Uncertainty: Current market analysis suggests that while AI demand remains robust, a slower-than-expected recovery in traditional PC and smartphone markets is leading to lower fab utilization rates, potentially causing customers to defer high-margin service contracts and equipment upgrades.

Find out more

Comments