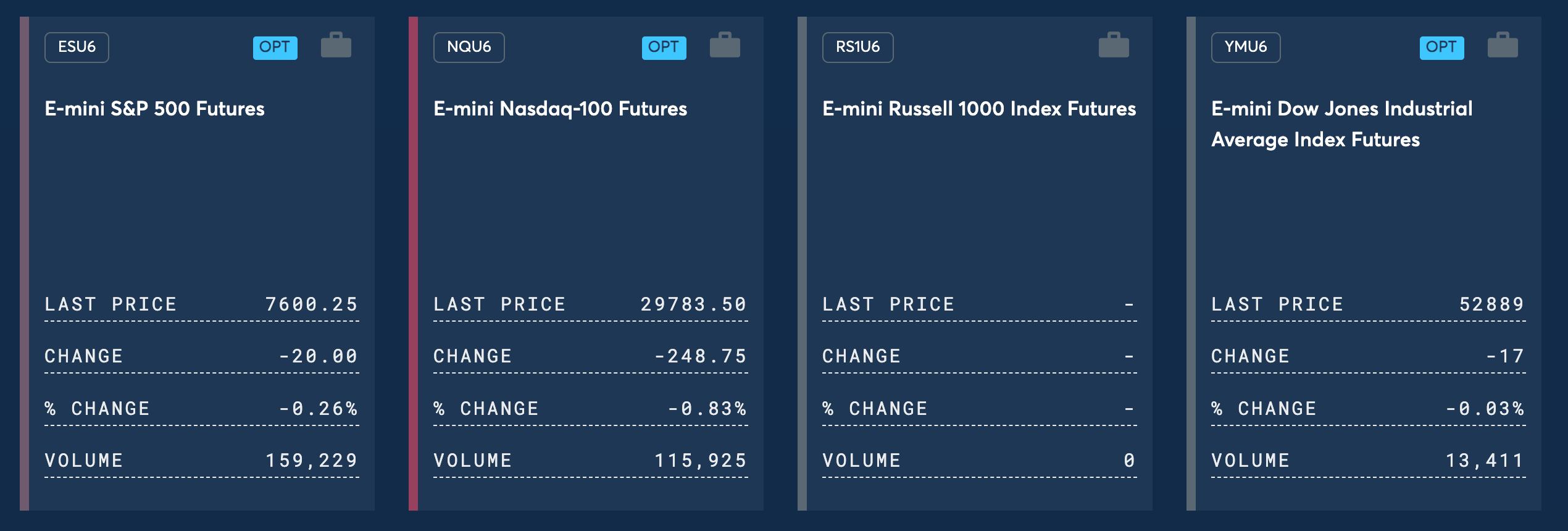

TradingKey - On July 13 Eastern Time, before the US market open, the three major stock index futures fell collectively. As of press time, Nasdaq 100 Index futures fell 0.83%, S&P 500 Index futures fell 0.26%, and Dow Jones futures fell 0.03%.

[Source: CME Group]

In commodities, international oil prices rose over 3%, with WTI crude oil futures trading at $73.83/barrel and Brent crude oil futures at $78.53/barrel. Gold and silver prices continued to slide. As of press time, spot gold ( XAUUSD) was trading around $4,062/ounce; spot silver ( XAGUSD) was trading around $58.7/ounce.

In the crypto market, as of press time, Bitcoin (BTC) was trading around $62,960, and Ethereum (ETH) was trading around $1,783. The US dollar index was at 100.9.

Market Moves

The memory chip sector plunged collectively premarket, driven by the spillover of negative sentiment from SK Hynix's slump in South Korea. As of press time, SK Hynix ( SKHY) fell over 8% premarket, SanDisk ( SNDK ), Micron Technology ( MU ), Western Digital ( WDC) fell over 4%, and Seagate Technology ( STX) fell nearly 4%. SK Hynix's stock plummeted over 15% in the South Korean market today, transmitting panic across markets to the US-listed memory sector.

AI tech stocks were under pressure across the board premarket. Nvidia ( NVDA) fell nearly 1.24%, Broadcom ( AVGO) fell 1.37%, AMD ( AMD ), Intel ( INTC) fell over 2%.

Megacap tech stocks diverged, with Microsoft ( MSFT) up 0.38%, Apple ( AAPL) flat, Meta ( META ), SpaceX ( SPCX ), Tesla ( TSLA) falling about 0.8%.

Market News

TSMC ( TSM )'s wave of price hikes has spread to mature nodes, raising quotes across the board. According to media reports, TSMC has notified customers that it will raise wafer quotes across the board, with the expected increase falling within the single-digit percentage range. Previously, TSMC mainly adjusted prices for advanced nodes; expanding the hikes to mature nodes this time indicates that foundry capacity tightness has spilled over from advanced nodes to the entire product line.

TSMC's June revenue surged 67.9% year-on-year, with Q2 results beating expectations again. TSMC today announced June revenue of NT$442.68 billion, up 67.9% year-on-year and 12.8% month-on-month. Q2 revenue exceeded NT$1.2 trillion, far surpassing the upper limit of the company's previous guidance, raising market expectations for a further upward revision of full-year guidance at the July 16 earnings call.

Meta adds $40 billion to Louisiana data center investment. Meta announced today that it will increase its investment in the Hyperion AI data center located in Richland Parish, Louisiana, from the previous $10 billion to $50 billion, with the planned total installed capacity raised to 5 GW. The data center will deploy the industry's most cutting-edge computing clusters, becoming one of Meta's largest AI training and inference bases globally. According to the officially disclosed infrastructure plan, the project is expected to first reach 2 GW of computing capacity and begin operations before 2030, with the remaining capacity gradually expanded in phases to reach the final 5 GW.

Samsung prepares to manufacture Tesla's AI5 chips. According to media reports, Samsung Electronics plans to manufacture next-generation AI5 chips for Tesla, to be used in the AI inference training platforms of Tesla's Dojo supercomputer and Optimus robot. Previously, Tesla's AI4 chips were manufactured by Samsung's 4nm production line, and the AI5 chips will adopt Samsung's 2nm process.

Warsh heads to Capitol Hill for the first time this week, while inflation data is released over the same period. Federal Reserve Chairman Warsh will testify before the House Financial Services Committee at 10:00 a.m. Eastern Time on July 14, and will move to the Senate Banking Committee on Wednesday. This marks Warsh's first semi-annual congressional monetary policy testimony since taking office. The U.S. Department of Labor will release June CPI data on Tuesday and June PPI data on Wednesday. The market expects the year-on-year increase in the June CPI to ease to 3.8% from 4.4%.

Key Events Preview

Eastern Time | Event |

July 14, 10:00 | Fed Chairman Warsh testifies before the House Financial Services Committee |

July 14 | JPMorgan Chase ( JPM ), Goldman Sachs ( GS ), Bank of America ( BAC ), Citigroup ( C ), Wells Fargo ( WFC) report Q2 earnings |

July 14, 8:30 | U.S. June CPI data (expected +3.8% YoY, previous +4.4%) |

July 15 | Fed Chairman Warsh testifies before the Senate Banking Committee |

July 15 | Morgan Stanley ( MS ), BlackRock ( BLK) report Q2 earnings; Johnson & Johnson ( JNJ ), United Airlines ( UAL) report earnings |

July 15 | ASML reports Q2 earnings; U.S. June PPI data |

July 16 | TSMC earnings call; Netflix ( NFLX) reports Q2 earnings; U.S. June retail sales data |

The panic selling in the memory chip sector during pre-market trading today is, in essence, cross-market contagion of market sentiment from South Korea to U.S. equities, compounded by the structural factor of leveraged ETFs magnifying volatility. However, at the same time, TSMC's across-the-board price hikes, its explosive June revenue surge, and Meta's additional data center investments all point to the continued accelerating expansion of demand for AI computing infrastructure. Samsung's entry into manufacturing Tesla's AI5 chips means TSMC's monopoly in advanced processes is facing a substantial challenge. Short-term emotional venting and long-term industrial logic are engaged in a fierce tug-of-war. This week's CPI data and Warsh's testimony will provide a macroeconomic anchor for the market. Before these two events land, the market is highly likely to maintain a cautious and volatile pattern.

Find out more

Comments