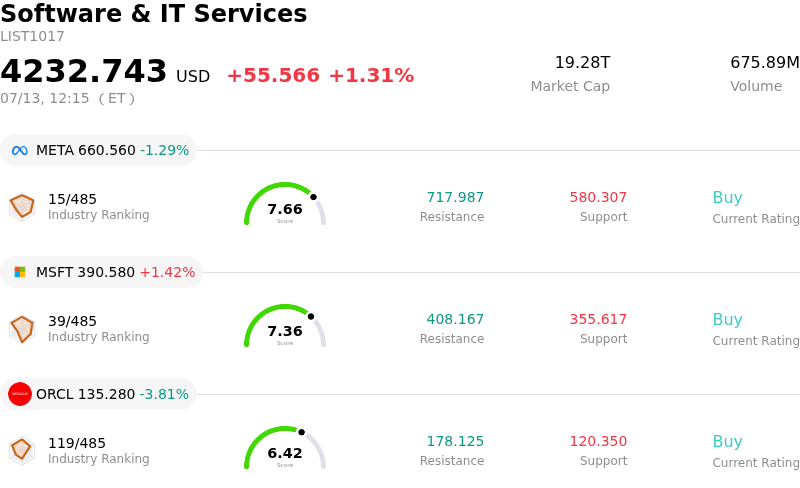

Applovin Corp (APP) moved down by 11.04%. The Software & IT Services sector is up by 1.31%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Meta Platforms Inc (META) down 1.29%; Microsoft Corp (MSFT) up 1.40%; Oracle Corp (ORCL) down 3.78%.

What is driving Applovin Corp (APP)’s stock price down today?

AppLovin experienced intense selling pressure during the current session, characterized by significant intraday volatility that has unsettled long-term holders. The sharp downward movement appears to be driven by a combination of sector-specific headwinds and a shift in institutional sentiment regarding the company software platform growth trajectory. Investors are reacting to emerging data suggesting a potential slowdown in the mobile advertising ecosystem, which directly impacts the high-margin segment of the business that has previously fueled the stocks premium valuation.

A primary catalyst for the decline stems from heightened competition within the ad-tech space, specifically as major platform operators introduce more sophisticated attribution tools that challenge existing independent networks. Reports of a shift in mobile operating system privacy protocols have resurfaced, creating uncertainty about the future efficiency of the company AI-driven recommendation engines. This regulatory and technical overhang is prompting a reassessment of long-term earnings guidance, as market participants weigh the costs of adapting to a more restrictive data environment against the company current operational scale.

From a technical perspective, the breach of key support levels triggered a wave of automated programmatic selling, exacerbating the intraday swings. Analysts have also noted a cooling of the recent enthusiasm surrounding the integration of generative artificial intelligence into creative asset production, with some large-scale funds trimming their exposure to rebalance portfolios into more defensive technology hardware. This rotation reflects a broader cautious stance on high-beta software names that have outperformed the broader market over the previous quarters.

Looking forward, the ability of the company to stabilize will depend on its next quarterly update and management commentary regarding the resilience of its software margins. Risk remains skewed to the downside in the near term as the market digests the implications of these competitive shifts. Investors should monitor upcoming industry-wide digital ad spend forecasts and any potential updates to regulatory investigations into the broader mobile app ecosystem, which could further influence market sentiment and volatility.

Technical Analysis of Applovin Corp (APP)

Technically, Applovin Corp (APP) shows a MACD (12,26,9) value of 4.264, indicating a buy signal. The RSI at 49.169 suggests neutral condition and the Williams %R at 43.975 suggests buy condition. Please monitor closely.

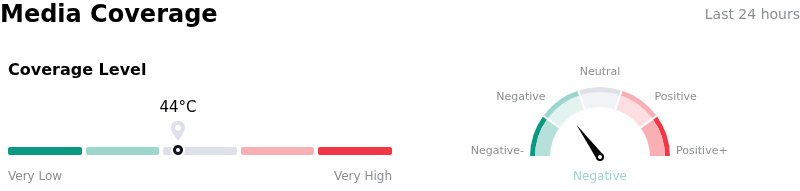

Media Coverage of Applovin Corp (APP)

In terms of media coverage, Applovin Corp (APP) shows a coverage score of 44, indicating a moderate level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Applovin Corp (APP)

Applovin Corp (APP) is in the Software & IT Services industry. Its latest annual revenue is $5.48B, ranking 56 in the industry. The net profit is $3.33B, ranking 18 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $654.04, a high of $860.00, and a low of $406.00.

More details about Applovin Corp (APP)

Company Specific Risks:

- Growth Sustainability and AXON 2.0 Plateau: Institutional analysts have raised concerns that the rapid growth driven by the AXON 2.0 AI engine may be reaching a point of diminishing returns, creating a "priced for perfection" scenario where any failure to exceed elevated Software Platform guidance triggers aggressive institutional selling.

- Regulatory and Privacy Headwinds: Ongoing shifts in OS-level privacy policies and the enforcement of the Digital Markets Act (DMA) in the EU continue to threaten the efficacy of AppLovin’s attribution modeling, potentially degrading ad-targeting precision and lowering return on ad spend (ROAS) for its core clients.

- Exposure to Hyper-Casual Market Decay: The company’s continued reliance on the hyper-casual gaming segment poses a structural risk, as this category faces persistent declines in user retention and monetization, which could drag on consolidated margins despite the success of the software-led business model.

- Competitive Margin Compression: Intensifying competition from integrated platforms like Unity and Google’s evolving AI ad-tech stack is forcing more aggressive pricing strategies in the mediation space, threatening to compress AppLovin’s take-rates and long-term operating profitability.

Find out more

Comments