HSBC's rating adjustment to Apple has released a strong bullish signal at a time when the market is divided over the growth prospects of the tech giants, highlighting Wall Street's repricing of Apple's AI strategy and hardware replacement cycle.

HSBC officially upgraded its rating on Apple stock to Buy from Hold today and gave it a $366 price target. This action not only broke the previous concerns of some major banks about the weak sales of Apple's hardware, but also injected new catalyst expectations into the market.

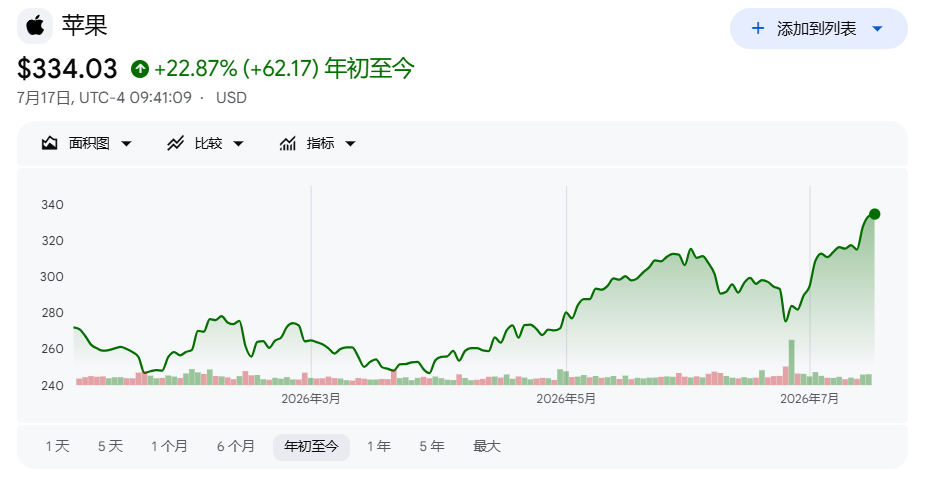

On Friday,Apple shares rose slightly, surpassing Nvidia as the world's most valuable company.

The upgrade and high target price setting directly reflect HSBC's optimistic judgment on Apple's fundamentals improvement. Against the background of the gradual integration of AI functions into the iOS ecosystem, Apple is trying to reshape its growth curve through software and hardware synergy, and this transformation is profoundly affecting investors' asset allocation logic.

The potential upside of Apple's stock price is further quantified with the $366 target price thrown. However, at a time when Wall Street as a whole remains cautious in the valuation of large technology stocks, whether HSBC's optimistic expectations can be transformed into actual market consensus still needs to be continuously verified by follow-up fundamental data.

The logic behind the rating upgrade: AI strategy and service business are two-wheel drive

This time, HSBC directly jumped its rating from "hold" to "buy", and its core logic probably points to Apple's AI strategy and continuously expanding service business. With the gradual push of AI functions such as Apple Intelligence, the market is generally expected to trigger a new round of iPhone replacement super cycle. HSBC obviously believes that AI is not only an innovation at the software level, but also a key engine driving the recovery of hardware sales.

In addition, the continued growth of the services business provides Apple with a high margin profit moat. In the stage when hardware sales are facing macro headwinds, the steady performance of service revenue such as App Store, Apple Music and iCloud effectively smoothed the overall profit fluctuation of the company. HSBC's rating adjustment is the recognition of this two-wheel drive model of "hardware cycle recovery + service profit support".

The game between upside and market expectation

The $366 price target is in a relatively upbeat range in Wall Street's pricing of Apple. Compared to the current share price, this price target implies significant upside, which directly enhances the stock's attractiveness to institutional funds.

From a valuation perspective, the $366 price target implies higher market expectations for Apple's earnings per share (EPS) growth in the coming quarters.

This not only requires the iPhone to achieve a substantial rebound in sales in the new cycle, but also requires the monetization rate of service business to further improve. For investors, this target price is not only HSBC's endorsement of Apple's long-term value, but also an important psychological resistance and traction for the upward breakthrough of the stock price in the short term.

Wall Street Divide: Institutional Rating Movements and Apple's Future Test

HSBC's bullishness is not the only voice on Wall Street. Recently, many financial institutions have shown obvious differences in Apple's rating trends.

Similar to HSBC, some institutions are optimistic about the iPhone replacement cycle empowered by AI, thus upgrading their ratings or maintaining "buy"; However, some institutions choose to maintain "hold" or even lower their target prices because they are worried about the intensifying market competition in specific regions and the declining margin of hardware innovation.

This disagreement is essentially a game of the realization speed of Apple's AI strategy. Although HSBC gave an optimistic expectation of $366, Apple still needs to prove in its subsequent financial performance that AI functions have indeed been transformed into real hardware sales and service revenue.

Under the intertwined influence of the macro interest rate environment and consumer willingness to spend, whether Apple can deliver on Wall Street's optimistic expectations will be the key test to determine whether its share price can truly touch $366.

Comments