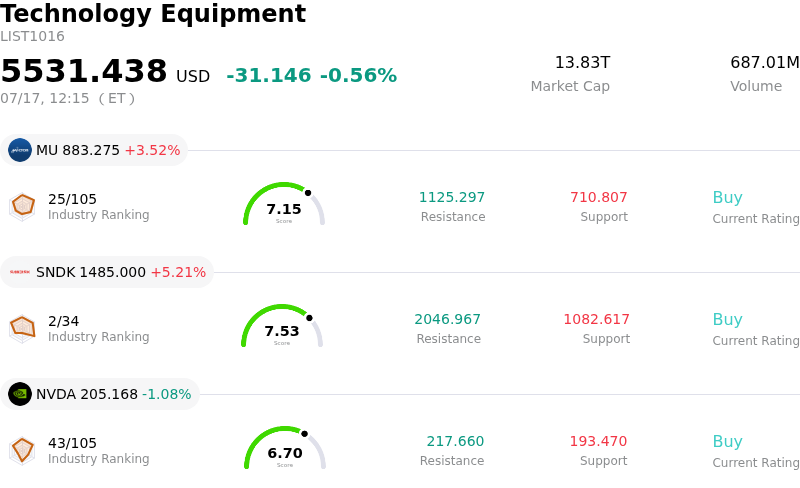

Micron Technology Inc (MU) moved up by 3.28%. The Technology Equipment sector is down by 0.56%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 3.28%; SanDisk Corporation (SNDK) up 5.24%; NVIDIA Corp (NVDA) down 1.08%.

What is driving Micron Technology Inc (MU)’s stock price up today?

Micron Technology experienced a notable upward trajectory during the session, fueled primarily by renewed optimism surrounding the high-bandwidth memory market. As the semiconductor industry navigates the middle of 2026, the transition toward advanced AI servers continues to drive an insatiable appetite for Microns HBM3E and next-generation HBM4 solutions. Investors are reacting to reports of tighter-than-expected supply constraints among competitors, which reinforces Microns pricing power and market share gains in the enterprise data center segment.

The positive sentiment was further amplified by a series of bullish notes from major sell-side institutions. Analysts have started revising their fiscal year estimates upward, citing improved yield rates on the companys 1-beta DRAM node. This technological edge is translating into higher gross margins, alleviating previous concerns regarding the capital expenditure intensity required to sustain AI-led growth. The anticipation of a robust earnings outlook has prompted institutional buyers to increase their weightings, contributing to the stocks strength despite broader market oscillations.

On the macroeconomic front, cooling inflationary data has provided a supportive backdrop for the broader technology sector. With the Federal Reserve signaling a more accommodative stance, the discount rate applied to growth-oriented tech stocks has shifted favorably. For a cyclical powerhouse like Micron, lower borrowing costs and a stabilized consumer electronics market, particularly in high-end smartphones and PCs integrated with on-device AI, offer a dual catalyst for revenue expansion beyond the core data center business.

Despite the intraday volatility, the underlying demand for memory remains structural rather than transitory. The significant movement observed today reflects a clearing of short-term hedges and a re-entry of long-term capital looking to capture the next leg of the semiconductor cycle. While geopolitical risks and currency fluctuations remain permanent fixtures of the risk landscape, the current fundamental momentum suggests that Micron is well-positioned to capitalize on the ongoing digital transformation, making it a focal point for portfolio rebalancing as the quarter progresses.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of -59.437, indicating a neutral signal. The RSI at 41.257 suggests neutral condition and the Williams %R at 96.457 suggests oversold condition. Please monitor closely.

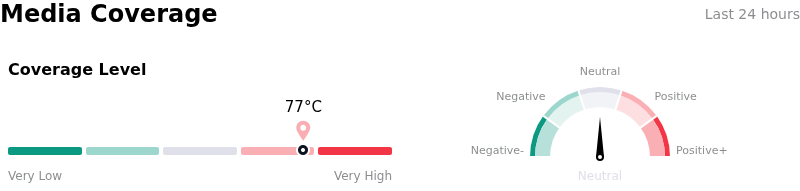

Media Coverage of Micron Technology Inc (MU)

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 77, indicating a high level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1462.09, a high of $2000.00, and a low of $190.00.

More details about Micron Technology Inc (MU)

Company Specific Risks:

- Intensified HBM Competition: Reports indicating that key competitors, particularly Samsung, are nearing qualification for their latest HBM3E chips for major AI accelerators threaten Micron’s current first-mover advantage and could lead to a significant loss of market share in the high-margin AI memory segment.

- Geopolitical Export Vulnerability: Ongoing trade tensions and the potential for stricter U.S. Department of Commerce export controls on high-end memory technology to China create substantial revenue risk, as Micron remains highly exposed to regulatory shifts that could curtail sales to Chinese OEMs.

- DRAM Pricing Resistance: Recent analyst commentary suggests that consumer electronics manufacturers in the PC and smartphone sectors are resisting further price increases for DRAM, potentially leading to a plateau in average selling prices (ASPs) and squeezing Micron’s anticipated margin expansion.

- Production Yield Challenges: Operational concerns regarding the ramp-up of ultra-advanced nodes, such as the 1-beta DRAM process, present a significant execution risk where any failure to achieve target yields could result in supply shortfalls and increased per-unit manufacturing costs.

Find out more

Comments