The process of 2021Q2 financial reporting season has been significantly accelerated. Last week, the financial reports of banking stocks generally exceeded expectations, but the market was cold. Investors' expectations were too high, and the decline in trading income was the potential reason.

Among the more than 40 companies (accounting for 8% of S&P 500 companies) that have announced their results so far, 85% of them are expected to beat earnings, which is the second highest in history since the financial crisis, while the earnings forecast of US stocks in this quarter remains around 70% year-on-year. (Mainly contributed by industries that recovered after the epidemic, such as energy, materials, finance and optional consumption)

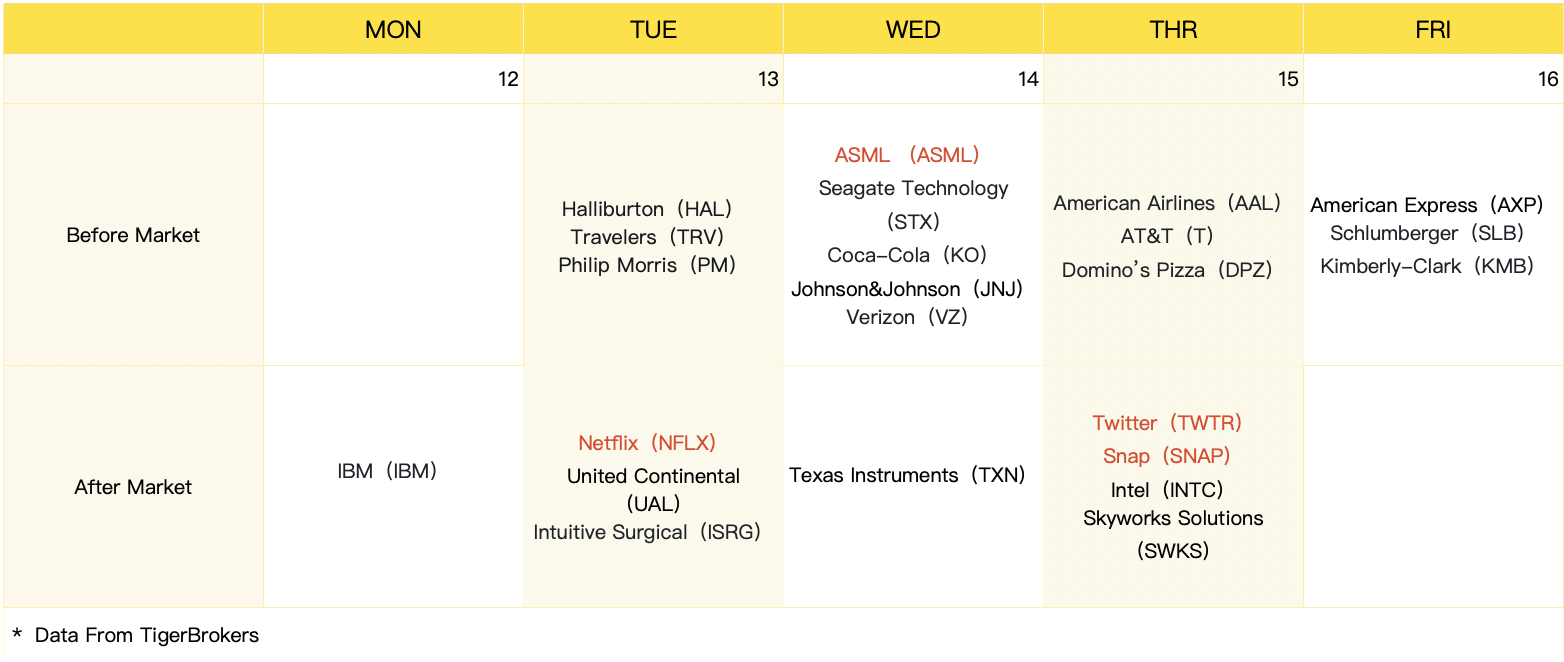

More than 250 companies will report results this week, including 73 S&P 500 companies. During the week, we will see more industry leaders' performance surface, such as $Netflix, Inc.(NFLX)$ , $ASML Holding NV(ASML)$ , $Coca-Cola(KO)$ , $Twitter(TWTR)$ , $Snap Inc(SNAP)$ .

Tuesday Netflix-$(NFLX) $

Netflix will release its financial results for the second quarter of 2021 after July 20, EST. The high base driven by the epidemic dividend in the first half of last year will put pressure on Netflix's results this quarter.

Netflix expects revenue of $7.3 billion and earnings per share of $3.16, according to Q2 performance guidelines provided by Netflix. Due to the outbreak of the epidemic last year, users were overdrawn ahead of schedule, and the content decreased in the first half of 2021, which may lead to the slowdown of membership growth in the second quarter. The company expects to add 1 million new users worldwide in the second quarter, far lower than the 10 million new users in the same period last year, and the 1 million new users are the lowest quarterly growth since the fourth quarter of last year.

Price increases are expected to add uncertainty to the third quarter results due to pent-up demand for outdoor entertainment.

However, the return of several blockbusters (Wizard, Cobra Road Hall, You and Paper House) will obviously be the catalyst for the normalization of user growth from the fourth quarter to 2022. On the positive side, although Netflix still has some problems in user growth recently, the company has successfully shifted from paying close attention to user growth to stable ARPU and free cash flow growth, and it is estimated that the operating profit rate in the second quarter will reach 25.5%.

Wednesday $ASML Holding NV(ASML)$

ASML will announce its second-quarter results on July 21st. As a chip equipment supplier with absolute monopoly position in the upstream of the industrial chain, ASML Holding NV ushered in a period of accelerated growth in performance.

Bloomberg unanimously expects that ASML Holding NV's net profit will increase by 35% year-on-year to 1.027 billion euros and its revenue will increase by 22.5% to 4.092 billion euros, which is at the high end of the company's guidance range of 4-4.1 billion euros. Driven by the increase of DUV (Deep Ultraviolet Lithography) production capacity with high profit margin in the second half of the year, ASML Holding NV is expected to increase its guidance for this fiscal year by 30%.

According to the current market demand, the growth of revenue and profit margin in 2021 mainly comes from non-EUV tools, and the management will also increase the production capacity of DUV in the second half of the year, which will continue until 2022, and the customer demand for EUV tools will remain strong throughout the year. Therefore, in the current environment, ASML Holding NV's further growth is limited by production capacity rather than demand.

Wednesday $Coca-Cola(KO)$

Coca-Cola will announce its second-quarter results before Wednesday's session. It is widely expected that Coca-Cola's net income and earnings per share in the second quarter will increase by about 30% year-on-year, which is mainly boosted by the decline in effective tax rate.

Revenue growth is due to a strong rebound in concentrated beverage sales, which is expected to increase by 26% this quarter, but decreased by 22% last year, which is mainly due to the sharp rebound in beverage consumption in restaurants and other business premises as consumers travel more.

Although Coca-Cola implemented a comprehensive restructuring at the beginning of the year, aiming at simplifying the organizational structure and reducing costs, it should be reflected in the third quarter at the earliest, and its operating profit will still be under pressure in the short term.

Thursday $Intel(INTC)$

Intel continued to benefit from the improvement of PC and server shipments, while cloud computing demand and enterprise IT expenditure remained high in the post-epidemic period.

Management is directing quarterly revenue of $18.9 billion and earnings per share to rise to $1.05. Competitor AMD and Cynthia's revenue consensus in the past six months has been revised up by 22-26%, while Intel's revenue consensus is only 3%. The expected difference also reflects that Intel's growth momentum rate is obviously insufficient.

In the long run, the long-term issues surrounding Intel's chip roadmap, especially the data center business, remain the biggest concern of investors.

Thursday $Twitter(TWTR)$

Bloomberg analysts unanimously expected Twitter's second-quarter revenue to be $1.058 billion, and the adjusted EBITDA was $204 million, which was basically consistent with management expectations.

Twitter, as a traditional social media platform, has the biggest challenge of peaking user growth on a month-on-month basis, but mDAU still has a 20% year-on-year growth, slightly inferior to other peers.

Last year, the epidemic greatly improved user activity, but Twitter will face difficult comparisons from the second quarter. It is expected that the growth rate of mDAU in the second quarter, the third quarter and the fourth quarter will still show low double-digit growth, and the growth low point may appear in the second quarter. Bloomberg predicts that mDAU will increase by 11% year-on-year to 204.5 million in the second quarter.

Compared with Facebook, Snap, Pinterest and other peers, the gap between Twitter users will only get bigger and bigger. The company can only hope for the recovery of popular sports events and product improvement to improve user participation. Long-term investors want to see the company's new successful monetization methods and efforts.

Just recently, Twitter launched two major subscription services: Early June: Twitter launched "Twitter Blue", which is a subscription service for content creators. Subscribers will be allowed to withdraw tweets, and can set a customizable timer of up to 30 seconds to withdraw tweets in time when they need to be modified. In mid-June, Twitter launched the long-rumored "Super Concern" function, which adopts paid subscription, and paid users can view the exclusive tweets of stars who have opened "Super Concern".

In addition, India's restrictions on Twitter and Nigeria's ban have added some uncertainty to international users. After all, India is one of its top five markets, and Nigeria has about 40 million Twitter accounts, but this is unlikely to have a substantial impact on the future direction of the company. Looking forward to the second half of the year, Twitter is a typical event-driven media platform. With the gradual recovery of large-scale sports events, such as the European Cup, the Olympic Games and the 2022 World Cup, it will support the activity of users to some extent. After the epidemic, it is a rare "honeymoon period" for Twitter. In addition, in the first quarter, the change of advertising identifier (DFA) on Apple iOS platform did not bring pressure to the advertising of this platform, and the impact will gradually appear in the second quarter.

Thursday $Snap Inc(SNAP)$

Snap is undoubtedly the leader of social platforms, and its revenue has maintained a high growth rate of more than 60% for two consecutive quarters, which greatly exceeded analysts' expectations. The growth rate of revenue and daily active users in the last quarter reached a new high in three years. Bloomberg unanimously expects Snap's second-quarter revenue to be 844.9 million US dollars, a year-on-year increase of 30%; Under Non-GAAP, EBITDA was US $1.8 million, which turned positive for the first time.

The advantage of Snap lies in its attraction to the younger generation of users. "Millennials" and "Generation Z" are the core user groups of Snap, and the high stickiness of young groups promotes the DAU to increase by 22% year-on-year to 280 million in the first quarter. In the second quarter, due to the high base last year, the growth rate of users declined. Bloomberg expects DAU to increase by 14% year-on-year to 290.6 million in the second quarter.

In terms of regions, Snap users have expanded faster in other parts of the world except the United States. Now, the number of Snap users in other parts of the world has exceeded the number of users in the United States, which has become the main contributor to the growth of users. Whether the growth of international users can continue is also a major attraction in the second quarter.

It is worth noting that the average revenue per user (ARPU) of Snap in other parts of the world is only 16% of that of ARPU in the United States, which has great room for improvement, reflecting the potential of Snap monetization overseas. In terms of valuation, the market selling rate of Snap is 25 times. Compared with Pinterest, which is 16 times, the price of Snap is definitely not cheap. Despite the increasingly fierce competition from peers for user time and advertising, Snap, with its loyal user base and continuous product innovation, will promote the expansion of profit margin in the global monetization process, and finally achieve long-term profit.

Comments